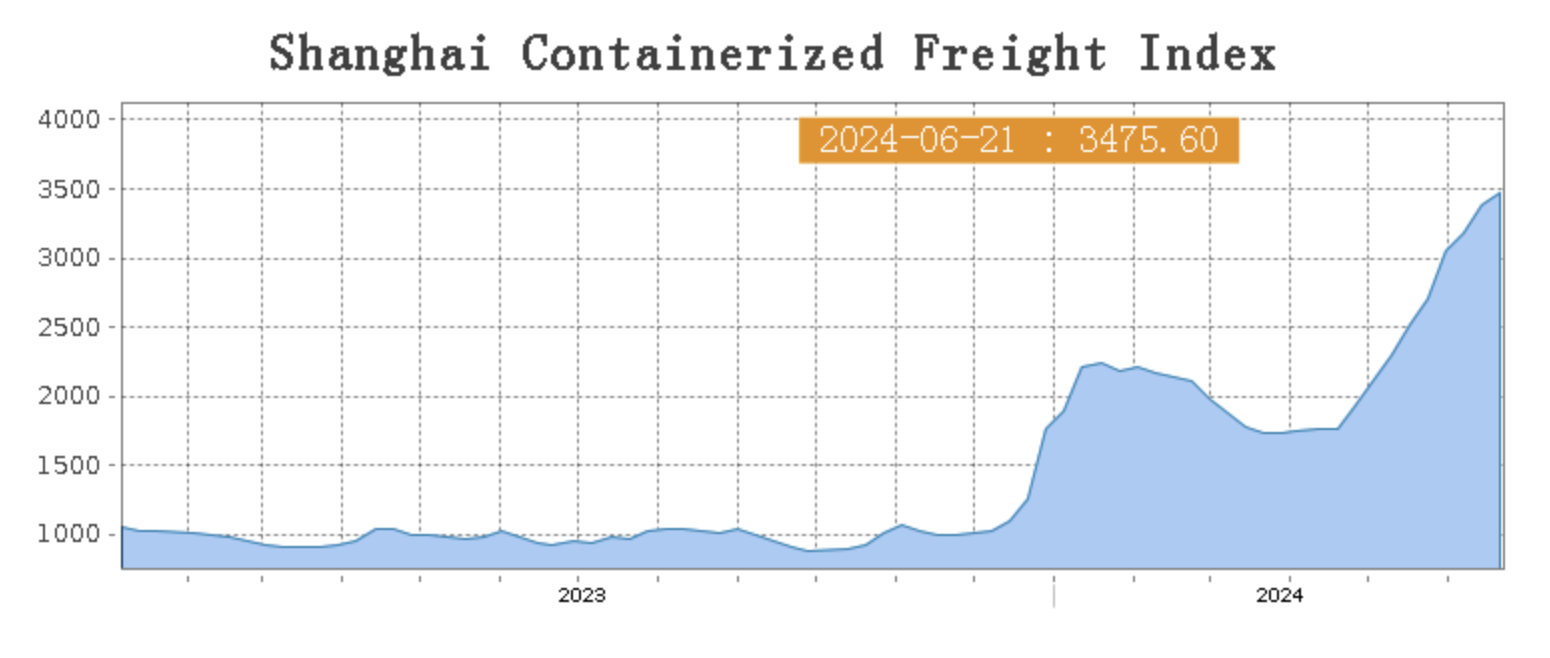

Turkey was the biggest buyer of Chinese stainless steel material in May. Last week, stainless steel prices declined because of the weak demand persisted. When the good news such as Beijing's economic stimulus and increasing LME nickel price gradually faded, the stainless steel prices lost a force to increase. Plus the Chinese domestic market, it is now in the slack season. In May, China's apparent consumption of stainless steel was reduced by 198,800 tons from last month. Whereas, the export volume, 457,700 tons, MoM increased by 65, 100 tons (17%) and YoY rose by 105,600 (30%). Inventory is close to the ceiling level, because of the previous large production by steel mills and the low force in purchase. In the short term, the stainless steel inventory might have to stock up. As for the sea freight, it is increasing but shows a flatter tendency. Last week, the Shanghai Containerized Freight Index rose by 2.9% to 3475.60. If you want to go deeper into the data and news, please keep reading our Stainless Steel Market Summary In China.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,140 | -16 | -0.77% |

| Foshan | 2,180 | -16 | -0.75% | ||

| Hongwang | Wuxi | 2,040 | -17 | -0.90% | |

| Foshan | 2,055 | -11 | -0.59% | ||

| 304/NO.1 | ESS | Wuxi | 1,975 | -14 | -0.73% |

| Foshan | 1,975 | -15 | -0.82% | ||

| 316L/2B | TISCO | Wuxi | 3,685 | 0 | 0.00% |

| Foshan | 3,740 | -10 | -0.29% | ||

| 316L/NO.1 | ESS | Wuxi | 3,545 | 5 | 0.13% |

| Foshan | 3,530 | -10 | -0.30% | ||

| 201J1/2B | Hongwang | Wuxi | 1,380 | -17 | -1.36% |

| Foshan | 1,380 | -14 | -1.09% | ||

| J5/2B | Hongwang | Wuxi | 1,280 | -19 | -1.58% |

| Foshan | 1,285 | -14 | -1.18% | ||

| 430/2B | TISCO | Wuxi | 1,230 | -3 | -0.22% |

| Foshan | 1,240 | 0 | 0.00% |

TREND || Weak Demand in the Off-Season, Futures and Spot Prices Struggle for Support.

Non-ferrous metals overseas maintained their strong performance and rebounded last week. In the spot market, stainless steel spot prices fell slightly last week. The current downstream consumption demand for stainless steel is still weak, and there is no further stimulus to boost prices. With the continuous arrival of steel mills, social inventory continues to increase. As of Friday of last week, the main stainless steel futures contract price has fallen by US$10.4/MT to US$2050/MT compared with last Friday, a decrease of 0.54%.

300 Series: Futures and Spot Prices Fluctuate.

The price of 304 in the market has been adjusted downward last week. As of Friday, the mainstream base price of 304 civil cold-rolled four-foot in Wuxi area has been adjusted to US$2000, down US$7/MT from last Friday; the price of civil hot-rolled has been adjusted to US$1980/MT, which is the same as last Friday. The price of stainless steel rebounded slightly last week, and the futures market fluctuated around US$2070/MT. Market inventory and warehouse pressure have accumulated to historical highs, and terminal procurement has not improved, and transactions are poor. The current off-season effect is prominent, and the arrival of the plum rain season has also affected the downstream procurement. The downstream procurement is cautious, and the transaction performance in the second half of the week is average. The transaction of low-priced resources is better.

200 Series: Low-Price Strategy, Improved Transactions.

The price of 201 fell mainly last week. The price of 201J2/2B 1.0 Hongwang four-foot coil is around US$1285/MT; the price of 201J1/2B 1.0 Hongwang four-foot coil is around US$1380/MT; the price of 201J1 five-foot hot-rolled is around US$1320/MT. In recent days, non-ferrous metals have fluctuated weakly, and the spot trading of stainless steel is light. Steel mills maintained stable prices and agents made concessions to promote transactions.

400 Series: Prices Can't Hold Anymore.

As of Friday of last week, the TISCO 430 cold-rolled guidance price is US$1475/MT, and the JISCO 430 cold-rolled guidance price is US$1605/MT, which is the same as last week. In the spot market of the tin market, the price of state-owned 430 cold-rolled is US$1230/MT-US$1235/MT, down US$4.1/MT from last week's quotation; the price of state-owned 430 hot-rolled is stable around US$1130/MT, which is the same as last week's quotation.

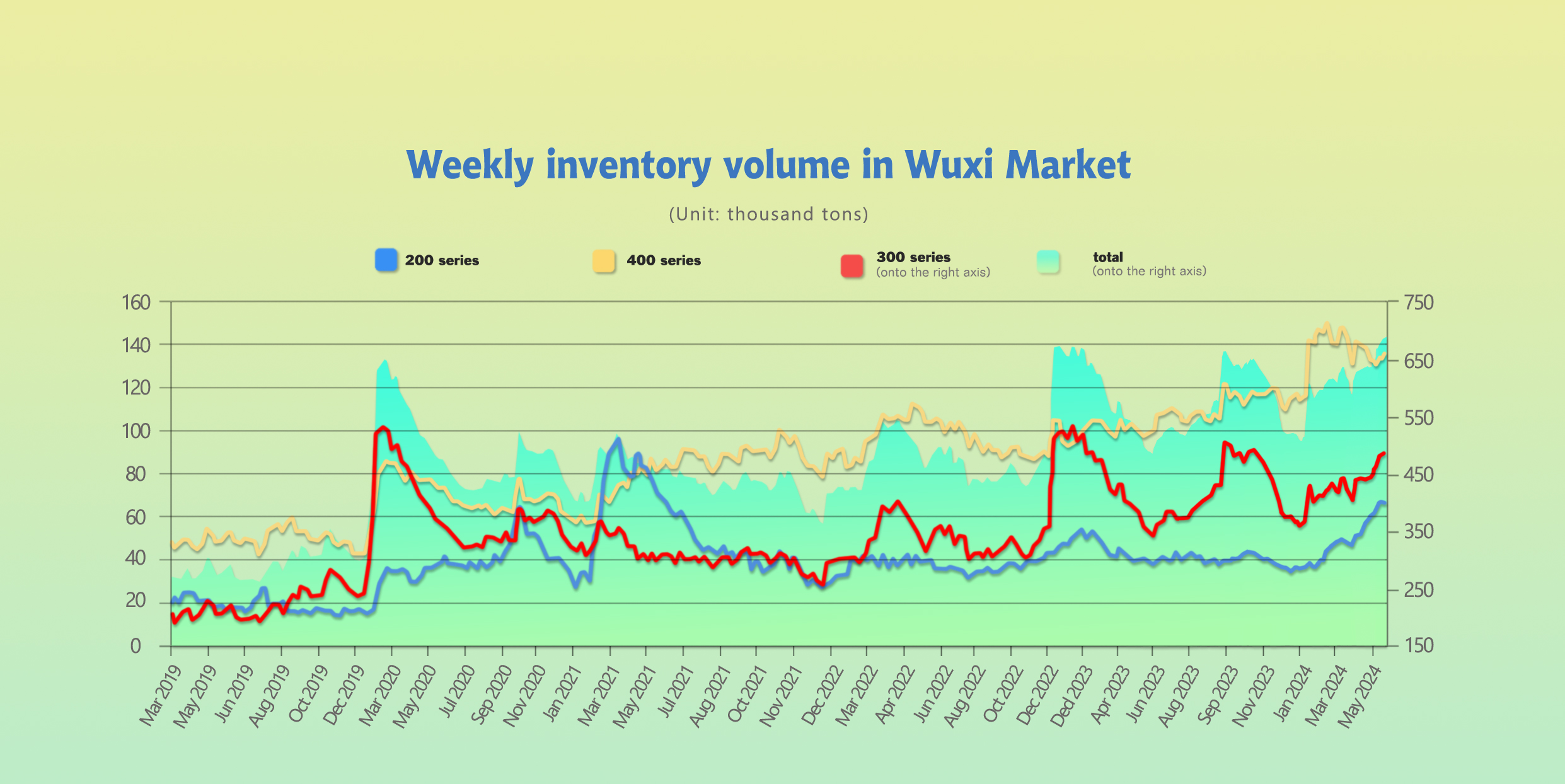

INVENTORY|| Inventory in Wuxi Market Increases by 0.94 Million Tons Last week.

The total inventory at the Wuxi sample warehouse lifted by 9,426 tons to 686,364 tons (as of 20th June).

the breakdown is as followed:

200 series: 621 tons down to 65,510 tons,

300 Series: 7,763 tons up to 485,507 tons,

400 series: 2,284 tons up to 135,347 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jun 13th | 66,131 | 477,744 | 133,063 | 676,938 |

| Jun 20th | 65,510 | 485,507 | 135,347 | 686,364 |

| Difference | -621 | 7,763 | 2,284 | 9,426 |

300 Series: Inventory Accumulates to a Historical High.

During last week, the main futures price rebounded from the bottom, the spot price fell, and the futures and spot prices diverged slightly. The arrival of goods in the market is normal last week, and the transaction is lukewarm. With the arrival of hot weather and the plum rain season, the market confidence has been frustrated. Therefore, the spot goods are mainly purchased on an as-needed basis, and the speculative sentiment is weak. The wait-and-see mood at the terminal has warmed up, and some orders in the early stage have been delayed in delivery, leading to a slight increase in social inventory, but the increase in inventory has narrowed compared with the previous month. The warehouse receipt is still on an upward trend year-on-year, the registered warehouse receipt resources have increased, and the spot supply pressure still exists. Based on the current raw material price, the steel mill is still in a loss state. The production of the steel mill in June is still high, the off-season demand is relatively weak, and the macro expectations are gradually cooling down. Under the double weak pattern, consumption is difficult to improve. It is expected that the inventory will continue to increase slightly next week.

200 Series: Inventory Remains High.

Last week, the Tsingshan Hongwang price remained the same, and the agent lowered the price for promotion. The transaction improved week-on-week. The production of 200 series steel mills in June has fallen slightly, but the output is still high compared with previous years. The off-season demand is weak, and the inventory may remain high. It is expected that the spot price of 201 will fluctuate in the short term, and the market transaction and the arrival of steel mills will be the focus in the future.

400 Series: Inventory Changes from Decrease to Increase.

The arrival of steel mill resources was normal last week, and the pressure of capital recovery at the end of the quarter has increased. Some traders have lowered prices to promote transactions, but the downstream still mainly purchases as needed, and the procurement is cautious. The spot inventory is digested slowly, leading to a slight increase in inventory. It is expected that the inventory will continue to increase slightly next week, and the subsequent inventory changes and market trading will be closely watched.

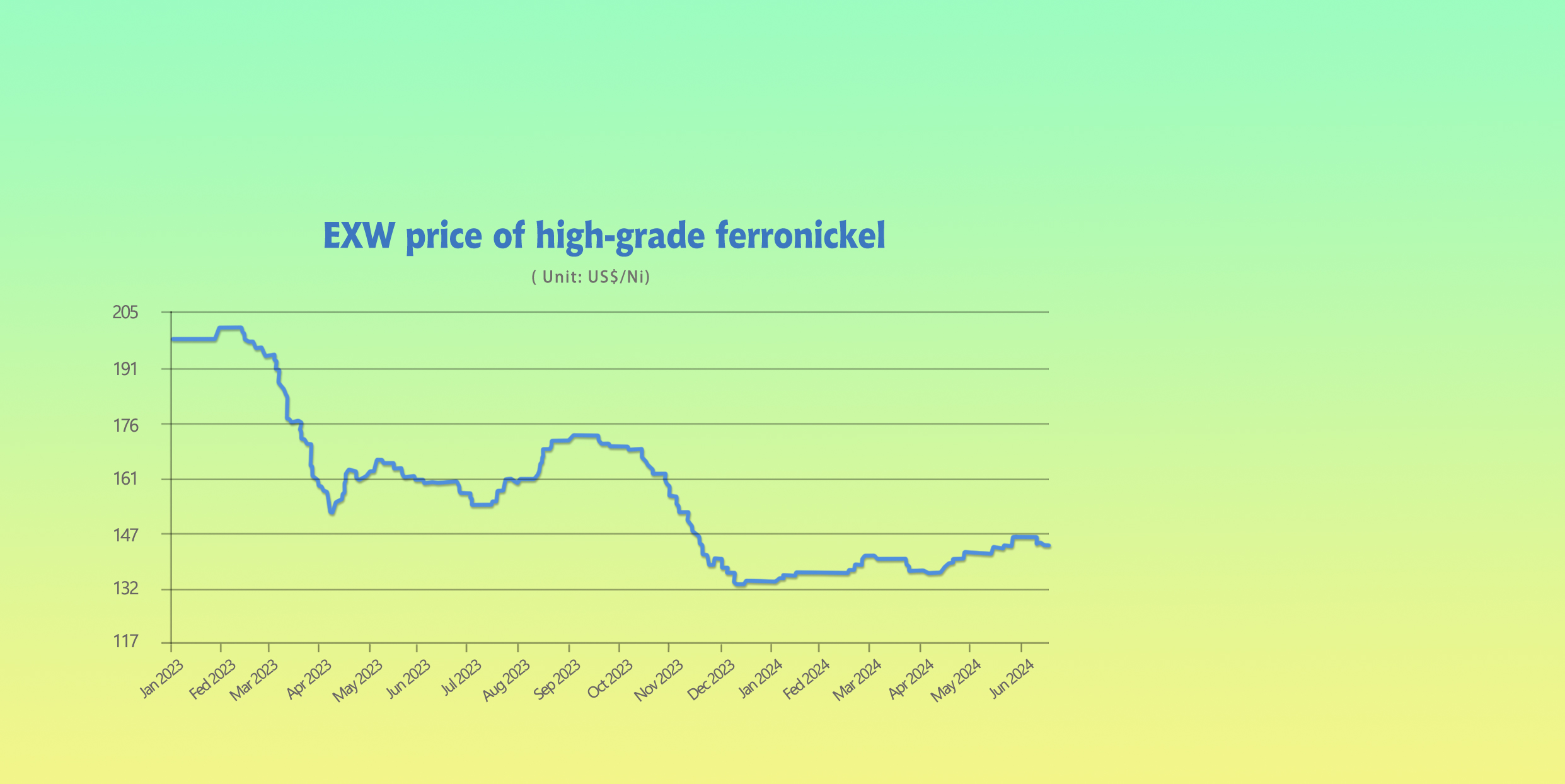

Raw Materials|| Steel mills are suffering losses, leading to a decline in nickel iron procurement prices.

The mainstream EXW price of high-chromium raw materials remains unchanged at US$1253- US$1267/50 reference ton compared to last week. Domestic production of high-chromium has continued to rise recently, while import volumes have decreased but remain higher than industry expectations.

SHFE nickel futures prices initially fell and then rebounded this week, reaching a low of US$18745/MT, the lowest in nearly ten weeks. As of Thursday's close, the main Shanghai nickel futures contract settled at US$19105/MT, down US$435/MT or 2.25% from last Thursday. Ex-factory prices of high-nickel iron are showing a weak trend, settling at US$137/nickel point as of last Thursday, down US$0.69/nickel point from last Thursday.

The Indonesian government has approved miners' work plans to produce an average of 240 million tons of ore annually for the next three years, basically meeting the current demand for nickel product production, and easing expectations for nickel ore supply. However, nickel ore resources in Indonesia remain tight, and ore prices are expected to remain high in the short term.

The sharp decline in stainless steel prices has intensified the cost inversion problem for domestic steel mills. Coupled with the decline in scrap prices, the use of nickel iron has become more economical. Steel mills have reduced their procurement of nickel iron recently, and nickel iron prices are expected to remain stable and weak in the short term.

Stainless Steel Trading Remains Weak, Social Inventory Pressure Persists.

Stainless steel prices have been trending weakly this week, with trading activity being relatively subdued. Downstream demand remains weak, social inventories continue to accumulate, and raw material prices are under pressure and declining, providing some support for stainless steel prices. Steel mill profits are marginal, and production remains high. The focus in the coming period will be on the pace of steel mill production and arrivals, as well as the strength of domestic macroeconomic policy stimulus. Stainless steel prices are expected to continue to fluctuate weakly in the later market.

300 Series: The current off-season effect is evident, terminal procurement willingness is weak, spot market inventory and warehouse receipts continue to accumulate, and stainless steel prices are trending weakly. Under the reality of strong supply and weak demand, steel mills may start to reduce production to help reduce inventory levels. It is expected that the spot price of 304 cold-rolled will remain weak in the short term, and the pace of changes in steel mill production will be closely monitored in the future.

200 Series: The production of 200 series steel mills in June remains high, and supply pressure persists. Off-season demand remains weak. Although agents have lowered prices for promotion, transactions have been sluggish and inventory remains high. It is expected that the spot price of 201 will continue to fluctuate weakly in the short term.

400 Series: The current spot market inventory is still at a high level. Although the production of steel mills in June has fallen slightly, the overall output is still high, and the market supply pressure has not been alleviated. It is expected that the price of 430 will remain weak in the short term. Based on current raw material prices, the production cost of 430 cold-rolled steel is causing steel mills to lose even more money, with a per-ton loss of up to 308 yuan. Steel mills are facing serious cost inversion and have a strong willingness to hold prices.

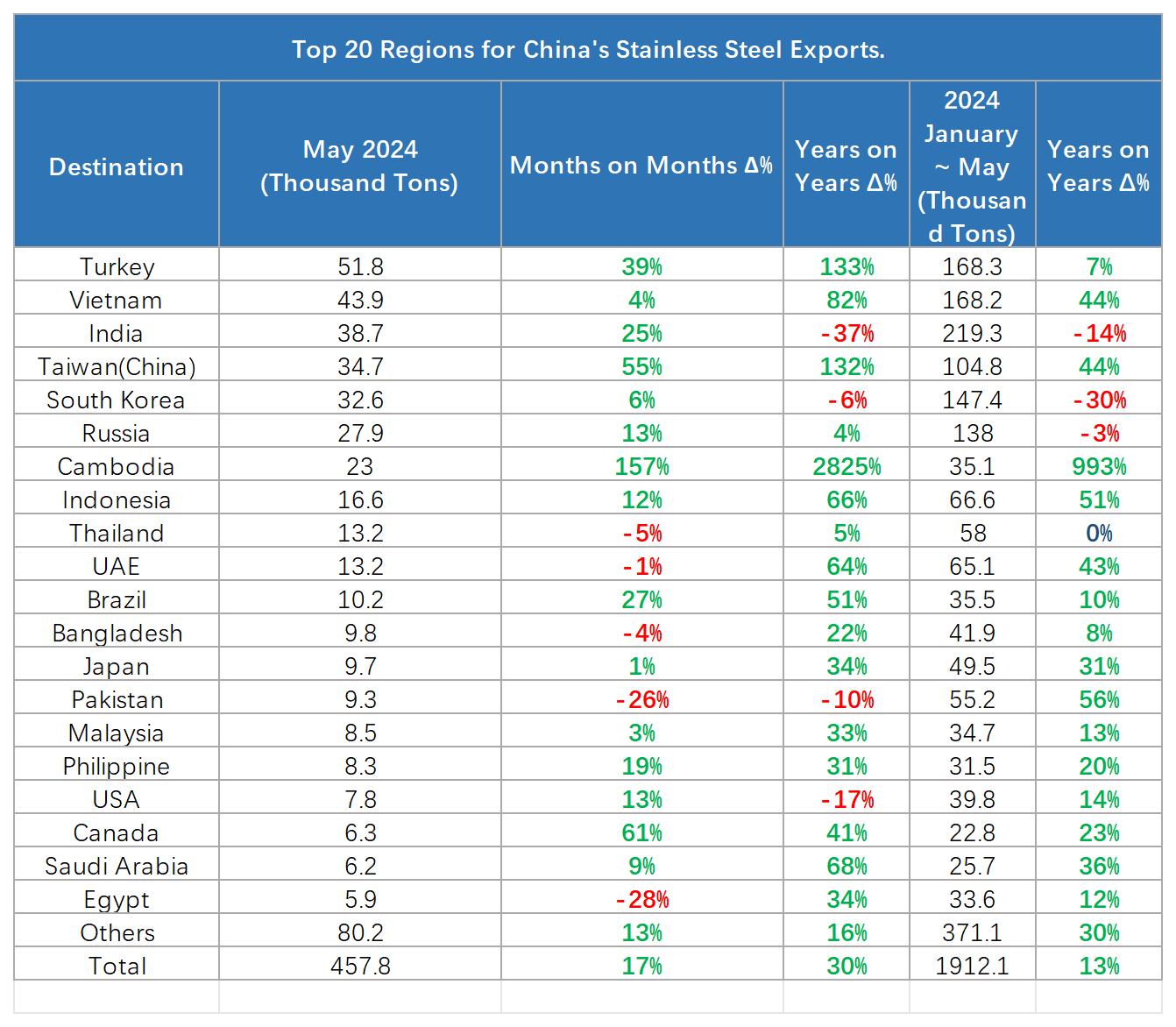

EXPORT & IMPORT||China's Stainless Steel Exports Surge by 30% in May.

China's stainless steel exports in May 2024 reached approximately 457,700 tons, an increase of 65,100 tons or 17% from the previous month. Compared to the same period in the previous year, exports increased by 105,600 tons or 30%. In the first five months of 2024, China's stainless steel exports to the top 20 regions totaled approximately 1.912 million tons, an increase of 216,500 tons or 13% year-on-year.

In May 2024, stainless steel exports from China increased to many regions. Exports to Turkey, Taiwan, and Cambodia increased significantly by 39%, 55%, and 157%, respectively, compared to the previous month. Exports from China to Thailand, the United Arab Emirates, and Bangladesh decreased slightly month-on-month.

The top 20 regions for China's stainless steel exports in May 2024 accounted for a total of approximately 377,500 tons, or 82.48% of total exports. In the first five months of 2024, the cumulative export volume from the top 20 regions was approximately 1.541 million tons, accounting for about 80.59% of total exports.

China's net stainless steel exports in May reached 283,300 tons, an increase of 84,700 tons or 43% from the previous month. Compared to the same period in the previous year, net exports increased by 72,900 tons or 35%. In the first five months of 2024, China's net stainless steel exports totaled approximately 935,400 tons, a decrease of 35,400 tons or 7% year-on-year.

Sea Freight|| Composite Index Continues to Rise.

The Chinese Export Container Shipping Market Continues to Show a Steady and Upward Trend, overall shipping demand remained stable this week, and freight rates on most sea routes increased, but the upward trend slowed down. The comprehensive index continued to rise. On 21st June, the Shanghai Containerized Freight Index rose by 2.9% to 3475.60.

Europe/ Mediterranean:

According to data released by the European Economic Research Institute (ZEW), the ZEW economic sentiment index for the eurozone in June was 51.3, which was better than market expectations and the previous value, and hit a new high since July 2021. The data shows that the European economy continues to maintain stable growth, which will help support shipping demand on European routes. At the same time, the Asia-Europe route also faces many risk factors, including the geopolitical tensions in the Red Sea region and the recent Sino-European trade disputes. The future Asia-Europe route shipping market will face great uncertainty.

On 21st June, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$4336/TEU, which rose by 3.8%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$4855/TEU, which jumped by 0.1%.

North America:

According to data released by the US Department of Commerce, US retail sales in May grew 0.1% month-on-month, below market expectations of 0.3%. The slowdown in retail data indicates that consumers are facing greater spending pressure. Continued inflation, a cooling labor market and rising debt costs could lead to continued weakness in the US retail situation in the future, increasing the risk of a stagnant economy.

On 21st June, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$7173/FEU and US$8277/FEU, reporting a 3.9% and 3.6% lift accordingly.

The Persian Gulf and the Red Sea:

On 21st June, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf dropped by 1.9% from last week's posted US$2893/TEU.

Australia/ New Zealand:

On 21st June, the freight rate (shipping and shipping surc-harges) for exports from Shanghai Port to the major ports of Australia and New Zealand was US$1406/TEU, a 1.7% growth from the previous week.

South America:

On 21st June, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports was US$8558/TEU, an 3.6% growth from the previous week.