Impact of the Iran Situation on China’s Stainless Steel Industry

From Jinling Metals’ perspective, while geopolitical uncertainties surrounding the Strait of Hormuz may trigger short-term volatility in freight rates and export flows, the long-term impact will largely depend on the duration of disruptions and the adaptability of global supply chains. The Middle East remains a strategically important destination for Chinese stainless steel, particularly for flat products.

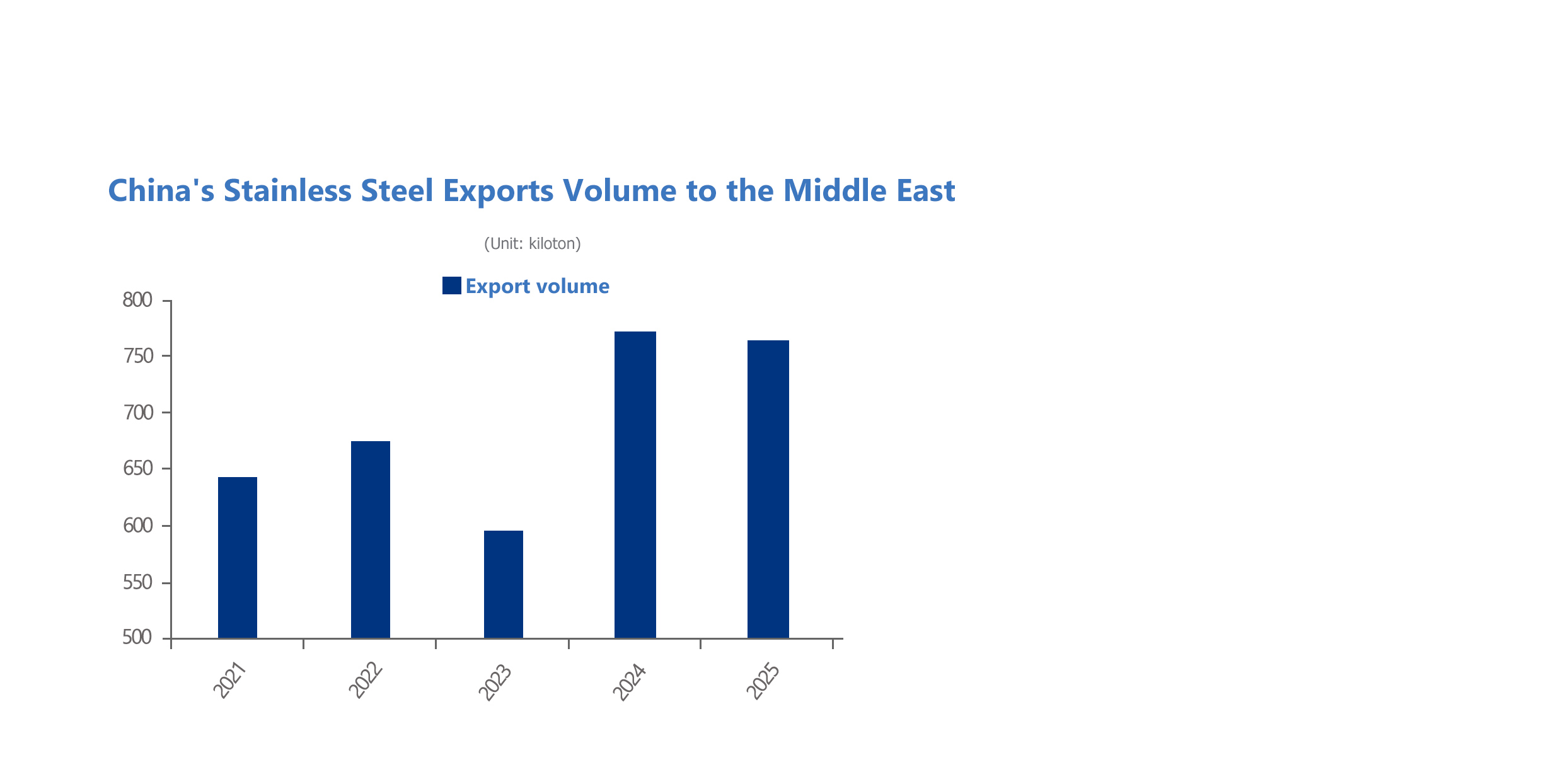

I. In 2025, the Middle East Accounts for 15.2% of China’s Stainless Steel Exports

In 2024, China exported approximately 772,800 tonnes of stainless steel to the Middle East, accounting for 15.4% of total exports, an increase of 176,700 tonnes year-on-year, up 29.7%.

In 2025, exports to the region totaled approximately 764,000 tonnes, representing 15.2% of China’s total stainless steel exports, down 8,500 tonnes year-on-year, a decline of 1.1%.

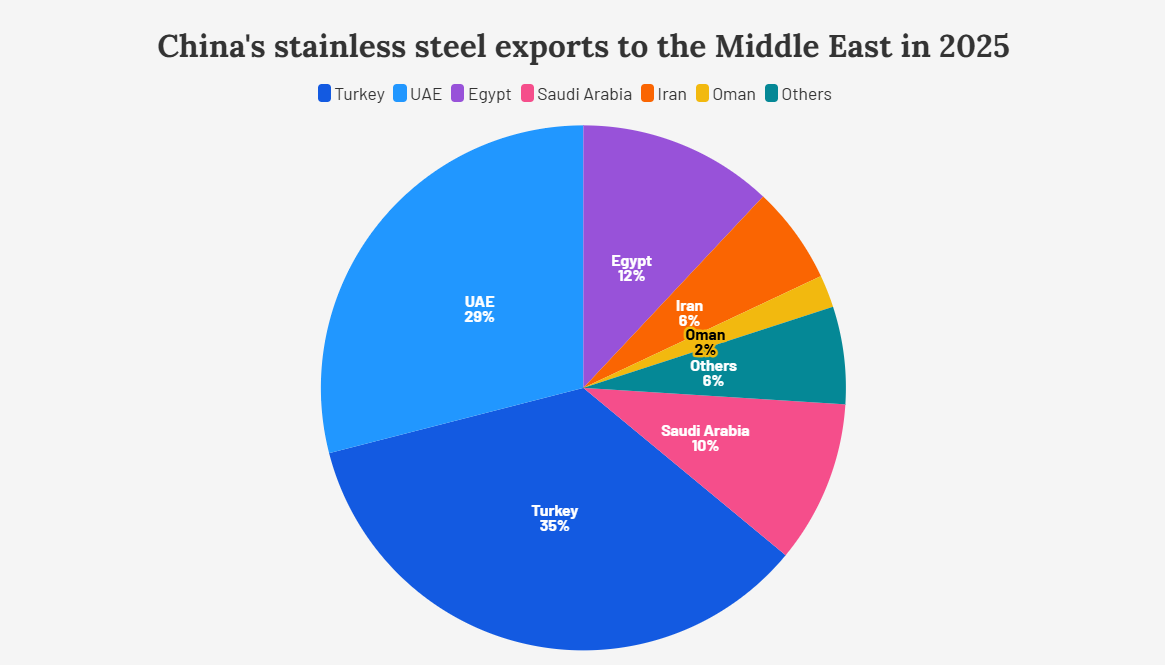

From a product perspective, flat products represent the primary category exported to Middle Eastern countries. Among them, the United Arab Emirates, Saudi Arabia, and Turkey exert the most significant influence. China’s flat product exports to these three countries account for approximately 4%–5% of total flat product exports. Exports to the seven major Persian Gulf countries combined account for 12.64% of China’s total flat product exports, while exports to the broader Middle East represent 21.82% of total flat product exports.

Angle sections and bars rank as the next most affected categories, while pipes and wire rods are relatively less impacted overall.

| China’s Steel Exports to the Gulf Region by Products (Unit: kilotons) | |||||||

| Product | UAE | Saudi Arabia | Iraq | Kuwait | Iran | Qatar | Bahrain |

| Flat | 3,680 | 4,050 | 900 | 210 | 200 | 200 | 10 |

| Bar | 120 | 320 | 10 | 0 | 0 | 40 | 0 |

| Angle | 1,390 | 850 | 370 | 610 | 40 | 130 | 40 |

| Tube | 190 | 270 | 30 | 20 | 10 | 30 | 10 |

| Wire | 80 | 80 | 20 | 10 | 10 | 10 | 0 |

The countries directly exposed are those that must rely on the Strait of Hormuz for maritime trade with China, including Saudi Arabia, the UAE, Iraq, Kuwait, Qatar, Iran, and Bahrain. In 2025, China’s steel exports to these seven countries accounted for 11.72% of total steel exports. Among them, the UAE, Saudi Arabia, and Iraq face the most significant indirect impact, representing 10.38% of total steel exports. Combined exports to these three countries reached 12.35 million tonnes in 2025.

The Strait of Hormuz serves as a critical shipping hub for China’s stainless steel exports to Saudi Arabia, the UAE, Iraq, Kuwait, and other Gulf countries. Any disruption to the Strait would directly affect shipping routes, potentially driving up freight rates and weakening export competitiveness.

| Status of China's Steel Exports to Other Middle Eastern Countries (Kilotons) | |||||||||||||||

| Item | Turkey | Egypt | Algeria | Israel | Jordan | Yemen | Morocco | Libya | Lebanon | Azerbaijan | Palestine | Syria | Cyprus | Georgia | Armenia |

| YoY Change | -6.5% | 5.7% | -5.8% | 30.5% | -11.2% | 37.0% | 102.6% | 8.1% | 19.8% | 3.1% | 285.8% | 376.4% | 272.6% | -1.9% | 23.1% |

| Net Change (25-24) | -267 | 84 | -72 | 223 | -53 | 78 | 200 | 12 | 25 | 3 | 1 | 94 | 23 | -2 | 1 |

| 2024 Exports | 4117 | 1476 | 1244 | 731 | 473 | 213 | 195 | 156 | 125 | 90 | 1 | 25 | 8 | 95 | 4 |

| 2025 Exports | 3850 | 1560 | 1172 | 954 | 420 | 291 | 395 | 168 | 150 | 93 | 2 | 119 | 31 | 93 | 5 |

| China’s Steel Exports to the Gulf Region by Country (2024 & 2025, Unit: kilotons) | |||||||||

| Year | Global | Iran | UAE | Saudi Arbia | Iraq | Kuwait | Qatar | Bahrain | Middle East Countries |

| 2024 | 111,060 | 400 | 5,500 | 4,770 | 1,440 | 530 | 340 | 50 | 23,150 |

| 2025 | 119,020 | 270 | 5,460 | 5,570 | 1,320 | 860 | 410 | 70 | 24,110 |

| Total | 7,960 | -140 | -40 | 790 | -110 | -110 | 70 | 10 | 970 |

| YoY (%) | 7.2% | -34% | -0.8% | 16.6% | -7.9% | -7.9% | 20.2% | 29.1% | 4.2% |

II. What If the Strait of Hormuz Remains Blocked?

A blockade of the Strait of Hormuz would first push up tanker freight rates. Once shipping through the Strait is suspended, major ports along the Persian Gulf coast would face paralysis or severe congestion.

If the Strait is blocked for one month:

New orders in March would likely be stalled, and steel export contracts scheduled for shipment from April onward would face widespread delays or potential defaults. If stranded vessels activate safe-port discharge clauses, large volumes of steel could be forced to unload midway in Oman, India, or other locations, leading to uncontrollable transshipment costs and delivery timelines. Traders would likely suspend quotations to the Middle East, and export volumes would decline sharply.

In this scenario, short-term shipment slowdowns combined with rising freight rates would passively lift FOB export prices. The estimated impact on China’s steel exports would be approximately 11.72%, equivalent to around 1.1624 million tonnes per month. Of this, flat products would account for about 770,000 tonnes per month, angle sections 280,000 tonnes, bars 40,000 tonnes, pipes 50,000 tonnes, and wire rods 20,000 tonnes.

If the disruption lasts two months:

The crisis would enter a mid-term stalemate phase. Charterers would face sustained demurrage charges, storage fees, and secondary transshipment costs, placing cash flow pressure on small and medium-sized traders. Shipping companies, due to prolonged route interruptions, may temporarily suspend or consolidate Gulf routes, further tightening vessel capacity. Middle Eastern buyers could shift from a wait-and-see approach to seeking alternative suppliers such as Turkey and India, potentially eroding China’s market share.

If the disruption lasts three months or longer:

Structural changes in the supply chain may occur. Some shipping lines could permanently adjust routes, and Gulf port functions may weaken. Steel products might need to transit through third countries (such as Oman or overland routes via Saudi Arabia) before entering Middle Eastern markets. Logistics costs would remain elevated for an extended period, pushing up local steel prices. More importantly, Middle Eastern buyers may accelerate diversification toward alternative suppliers such as Turkey, India, or Russia, posing a long-term risk of permanent market share loss for Chinese steel. The prolonged absence of war risk coverage could also shift trade models toward “self-risk assumption” or “advance payment + liability waiver” arrangements, further raising transaction barriers.

Estimated 32.7% Month-on-Month Increase in China’s Stainless Steel Crude Steel Output in March 2026

1. Estimated Crude Stainless Steel Output in February

According to statistics, the estimated crude stainless steel output of 43 domestic stainless steel mills in February 2026 was 2.7383 million tonnes, down 798,100 tonnes month-on-month (a decrease of 22.57%) and down 12.94% year-on-year.

Breakdown by series:

- Stainless Steel 200 series: 840,300 tonnes, down 192,800 tonnes MoM (–18.66%), down 8.54% YoY;

- Stainless Steel 300 series: 1.3228 million tonnes, down 535,300 tonnes MoM (–28.81%), down 20.04% YoY;

- Stainless Steel 400 series: 575,200 tonnes, down 70,000 tonnes MoM (–10.85%), up 0.52% YoY.

2. Production Schedule for March

Planned production for March is 3.6335 million tonnes, up 32.69% month-on-month and up 3.46% year-on-year.

Breakdown by series:

- Stainless Steel 200 series: 1.0771 million tonnes, up 28.18% MoM and up 11.63% YoY;

- Stainless Steel 300 series: 1.8948 million tonnes, up 43.24% MoM and down 0.37% YoY;

- Stainless Steel 400 series: 661,600 tonnes, up 15.02% MoM and up 2.51% YoY.