Demand weakened and inventory rebounded before the Easter and Chinese’s Tomb-Sweeping Day holidays, with the stainless steel market fluctuating downward amid cost support and supply-demand pressure.

I. Market Overview

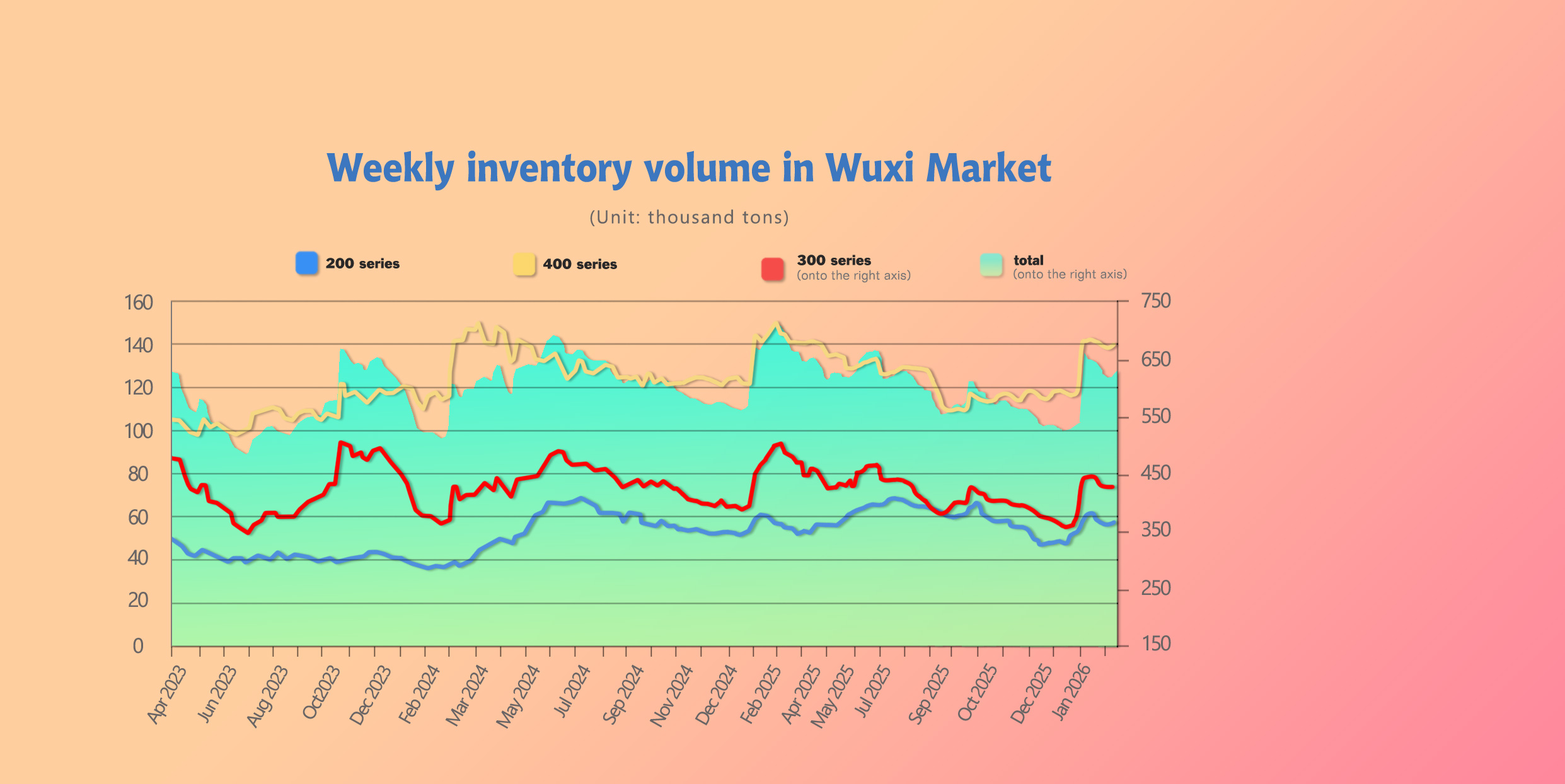

From March 30 to April 5, 2026, stainless steel prices in the Wuxi market generally showed a weak downward trend last week. During the week, South China steel mills opened allocations for cold-rolled stainless steel 304 resources, while previously centrally dispatched hot-rolled resources arrived successively, causing the market's spot inventory to shift from a destocking state to a slight accumulation. Approaching the Tomb-Sweeping Day holiday, the procurement pace of downstream terminals slowed down significantly, market wait-and-see sentiment rose, and the overall atmosphere in the futures and spot markets trended toward caution.

As of Friday, the price of the main stainless steel contract fell by 25 USD/ton from the previous week to 2,215 USD/ton, a decrease of 1.15%. Overall, although the cost side still provides some support, the price center of gravity has shifted lower against the backdrop of no obvious improvement in demand.

II. Market Performance by Series

Stainless steel 300 Series: Cost Support Persists, Prices Fluctuate Downward

Last week, 304 cold-rolled and hot-rolled prices generally performed weakly. As of Friday, the mainstream basis price for 4-foot 304 private cold-rolled stainless steel in the Wuxi area was quoted at 2,175 USD/ton, down 15 USD/ton from the previous Friday; the private hot-rolled stainless steel price was quoted at 2,145 USD/ton, also down 15 USD/ton.

Looking at the pace of price movement, early in the week, influenced by news of Indonesia delaying the imposition of a windfall tax on nickel and coal on April 1, Shanghai nickel prices weakened, dragging down stainless steel futures and spot prices under pressure. Mid-week, Tsingshan Group opened prices again, raising the 304 cold-rolled quotation by about 30 USD/ton, which boosted market sentiment in the short term, but overall cold-rolled and hot-rolled stainless steel 316L prices remained stable. Influenced by the sentiment of "buying when prices rise, not when they fall," downstream procurement mainly adopted a wait-and-see approach, with some orders shifting to the futures market, resulting in limited support for spot transactions. At the end of the week, non-ferrous metals broadly operated under pressure, and lacking new driving factors in its fundamentals, the stainless steel price dropped again by about 5 USD/ton.

Overall, stainless steel 300 series exhibited some resilience against price drops supported by raw material costs, but lacking effective cooperation from the demand side, prices still mainly fluctuated with a weak bias.

Stainless steel 200 Series: Inventory Pressure Accumulates, Prices Pull Back Under Pressure

Last week, stainless steel 200 series prices generally showed a slight downward trend. Futures prices saw mixed gains and losses, while transactions in the spot market gradually weakened. On Wednesday, quotations from Desheng and Beigang were reduced by 5 USD/ton to a basis price of 1,215 USD/ton; on Thursday, the actual transaction price of 201J2 cold-rolled steel from Tsingshan agents floated further down, and low-priced resources in the market continued to increase.

From a transaction perspective, low-priced resources were shipped relatively smoothly early in the week, but as the holiday approached, downstream stocking intentions weakened, leading to a slight accumulation of both cold-rolled and hot-rolled stainless steel 200 series inventories in the Wuxi market.

In summary, under the dual impact of marginally weakening cost support and fading demand, stainless steel 200 series market operated under pressure, with inventory pressure gradually becoming apparent.

Stainless steel 400 Series: Cost Support Loosens, Supply-Demand Contradictions Intensify

Last week, stainless steel 400 series stainless steel prices generally operated weakly. Taking 430 as an example, as of Friday, the quotation for state-owned cold-rolled stainless steel 430 in the Wuxi spot market was 1,250–1,255 USD/ton, down 5 USD/ton from the previous week; the quotation for hot-rolled steel was 1,125 USD/ton, basically flat compared to last week.

During the week, traders generally adopted a strategy of yielding profits to accelerate inventory digestion, but as prices fell slightly, downstream procurement became more cautious. Due to the relatively slow pace of demand recovery, the inventory digestion speed lagged behind new supply, further increasing the market's inventory build-up pressure.

Against the backdrop of a slight pullback in high-carbon ferrochrome prices on the cost side, the support level for stainless steel 400 series weakened, and coupled with the continuous release of supply, prices generally operated under pressure.

III. Short-Term Market Outlook

Looking at individual varieties, against the backdrop of raw material prices remaining high, cost support for the stainless steel 300 series still exists. Meanwhile, stainless steel futures warehouse receipts are at a five-year low, dropping by approximately 75% year-on-year, meaning deliverable resources are limited, which provides certain support for prices. Considering changes in Indonesia's nickel ore policies and fluctuations in the overseas macroeconomic environment, market fluctuations will remain relatively obvious. If demand sees a phased release after the Tomb-Sweeping Day holiday, there is some room for price recovery.

For the 200 series, prices of copper and high-carbon ferrochrome on the raw material side have pulled back, while manganese prices remain stable, resulting in somewhat weakened overall cost support. At the same time, steel mills maintain high production scheduling expectations for April, which, combined with basically stagnant transactions during the holiday, may further reveal destocking pressure post-holiday. If subsequent transaction improvements drive inventory destocking, there may be a phased opportunity for price recovery.

Regarding the stainless steel 400 series, current cost support is marginally weakening, while the supply side maintains high-level operations, and demand recovery still appears insufficient. Given the weak performance during the traditional peak season, short-term prices are expected to remain under pressure, and going forward, close attention should be paid to the pace of downstream demand release and the arrival of steel mill resources.

IV. Q1 Market Review and Q2 Outlook

In the first quarter of 2026, the core driving force for the rise in stainless steel prices mainly came from the continuous strengthening of the raw material side.

In terms of nickel ore, Indonesia's 2026 RKAB approval quota was significantly tightened compared to the 2025 actual production target, with the market generally expecting a decrease of about 30%. This expectation drove a significant increase in Shanghai nickel futures in early January, and the ex-factory price of high-grade ferronickel rose from approximately 130 USD/nickel point in December 2025 to over 161 USD/nickel point in early March 2026, providing solid cost support for stainless steel 300 series.

Regarding ferrochrome, in late January, Tsingshan Group and TISCO announced the February bidding price for high-carbon ferrochrome, raising it to 1212 USD/50 reference tons. As outer market quotations for chrome ore continued to rise, ferrochrome prices cumulatively increased by about 45 USD/50 basis tons in January, reaching 1275 USD/50 reference tons by the end of March, an increase of about 7% from the beginning of the year.

Against the backdrop of a substantial rise in costs, the production cost of stainless steel increased significantly. According to estimates, the production cost of 304 cold-rolled steel rose from 1,970 USD/ton in December 2025 to 2,215 USD/ton at the end of January 2026. Driven by rapid follow-up increases in spot prices, industry profit margins briefly recovered to about 3.7%. However, entering February and March, affected by holidays and slow demand recovery, spot prices lacked upward momentum, profit margins were compressed again, and some processes returned to near the break-even point.

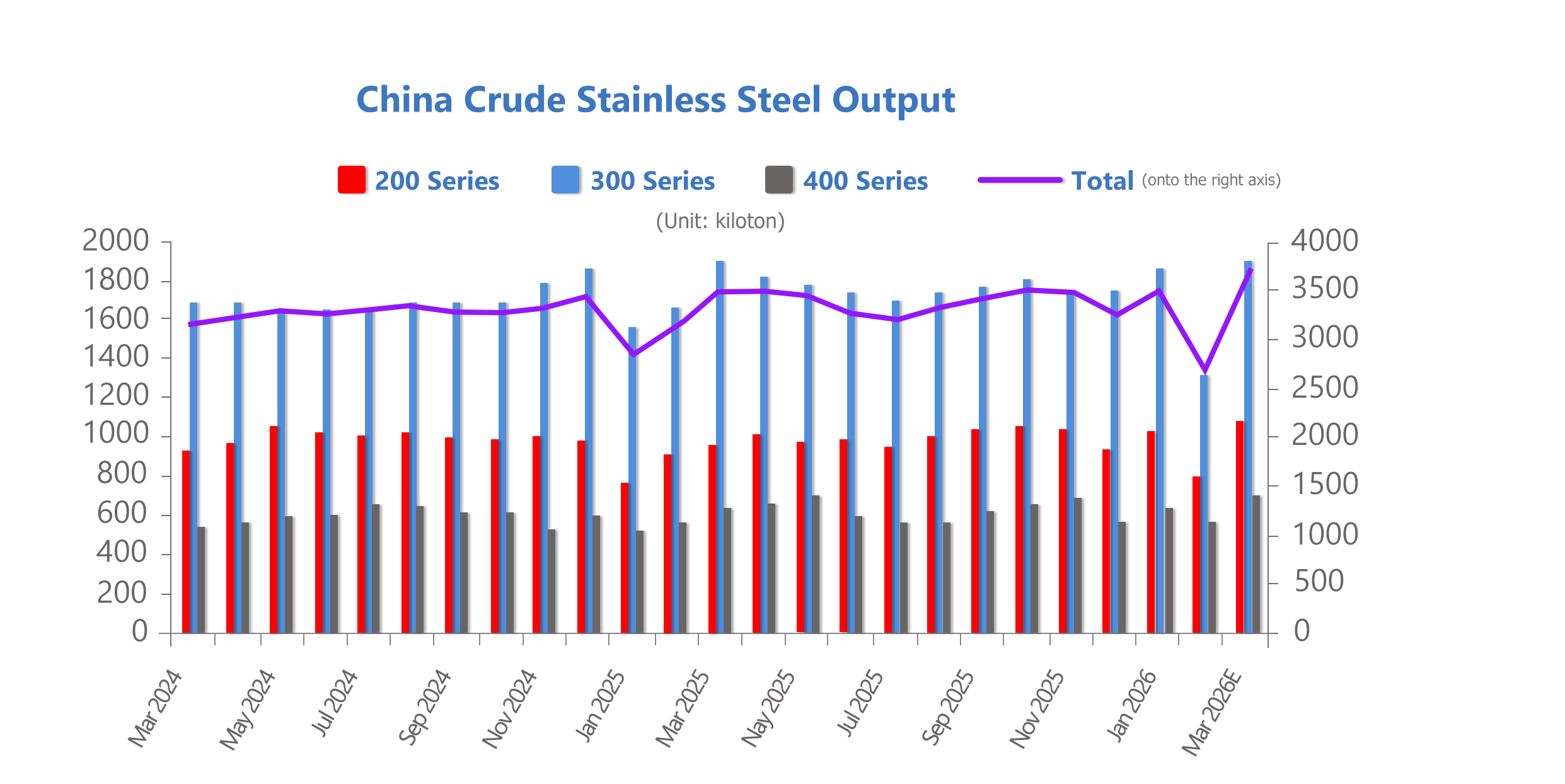

From a supply and demand perspective, the primary contradiction in the Q1 market lay in the mismatch between high elasticity on the supply side and a slower recovery on the demand side. In March, the crude steel production scheduling of 43 domestic stainless steel plants reached 3.6795 million tons, a month-on-month increase of 36.53% and a year-on-year increase of 4.77%, marking a significant elevation in overall supply levels. At the same time, downstream demand recovery fell short of expectations, with the market relying primarily on rigid demand procurement, and the transaction pace shifting along with price fluctuations.

Regarding inventory, the first quarter generally exhibited a trend of "falling first, then rising." In January, driven by rising costs and pre-holiday restocking, social inventories continued to be digested; during the Spring Festival, stagnant transactions combined with increased arrivals from steel mills led to post-holiday inventory accumulation. With terminals resuming work at the end of February, inventories briefly destocked, but entering March, demand failed to sustain its release, causing inventories to rebound again. Although current inventory levels have not reached historical extremes, they are already in a relatively high range.

Looking ahead to the second quarter, as the traditional off-season approaches, orders on the demand side may gradually weaken. With steel mills maintaining a relatively high level of production scheduling, the contradiction of oversupply may further intensify, there is still room for inventory pressure to rise, and prices may generally show a fluctuating, slightly weak operating trend.

V. Shipping Market Dynamics

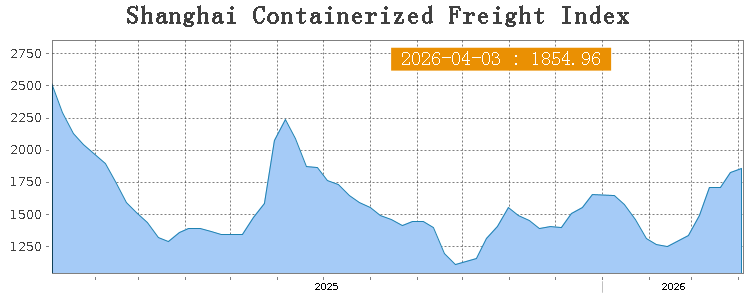

This week, the Chinese export container shipping market generally maintained a fluctuating operation against the backdrop of sustained geopolitical tensions, with freight rates for most ocean routes continuing to rise, driving the composite index up slightly. On April 3, the Shanghai Containerized Freight Index (SCFI) stood at 1854.96 points, up 1.5% from the previous period.

Looking at individual routes, influenced by rising energy prices and inflationary pressures, economic growth expectations for the European route weakened, while transportation demand remained fundamentally stable, with freight rates dropping slightly to $1,650/TEU, down 3.1% from the previous period; freight rates for the Mediterranean route were $2,684/TEU, down 2.9%. Demand for the North American routes performed stably, with freight rates rising to $2,359/FEU (US West Coast) and $3,354/FEU (US East Coast) respectively. Affected by the Middle East conflict, freight rates for the Persian Gulf route continued to rise to $3,977/TEU. Driven by recovering demand, freight rates for the Australia-New Zealand and South American routes rose to $794/TEU and $2,609/TEU, respectively.

Overall, geopolitical factors remain the primary driving force behind current freight rate fluctuations, but there is still some uncertainty regarding the global demand outlook.