Last week (May 25th-29th), stainless steel spot prices in the Wuxi market were mixed. Prices for the 300 series were mostly under pressure; as previously allocated resources from steel mills arrived intensively at warehouses, spot inventory pressure increased. The 200 and 400 series operated stably with a strong bias, though transactions slowed down within the week after prices were adjusted upward. As of May 29, the price of the main stainless steel contract rose by US$18.6/MT from the previous week to US$2345/MT, an increase of 0.85%.

Market Performance by Series

Stainless steel 300 Series: Price Declines Slow Down, Spot Inventory Surges

Last week, cold-rolled and hot-rolled stainless steel 304 spot prices continued their downward trend, but the overall decline slowed down.

As of Friday, the mainstream base price for 4-foot cold-rolled stainless steel 304 in the Wuxi area was quoted at US$2315/MT, down US$7 from the previous week; the private hot-rolled price was quoted at US$2290/MT, flat compared to the previous week.

Early in the week, Tsingshan Steel Mill opened allocations for June, keeping stainless steel 304 plate prices flat while lowering stainless steel 316L plate prices by US$104/MT, which dragged spot prices down by US$7/MT. For the remaining trading days, prices fluctuated within a narrow range with no effective intraday rebound.

As the market entered the year-end closing phase for the month, trading activity became even quieter. Merchants increasingly offered hidden price cuts to ship goods, focusing primarily on completing their monthly agreement volumes.

Stainless steel 200 Series: Prices Continue to Strengthen, Transaction Pace Slows Down at High Levels

Last week, the futures market fluctuated, and stainless steel 201 prices mainly grew stronger. Steel mills raising their June plate prices boosted market confidence, keeping agent quotations firm at high levels.

Currently, agents for Desheng and Beigang quote BN1D4 and J5 at a basis of US$1275/MT, while Tsingshan cold-rolled stainless steel 201J2 is quoted at a base of US$1280/MT.

Approaching the end of the month, downstream purchasing shifted to a wait-and-see stance. Some traders exchanged price for volume, slightly adjusting shipping prices downward. Within the week, there were ample circulable resources of Hongwang cold-rolled steel, leading to a slight accumulation of market inventory.

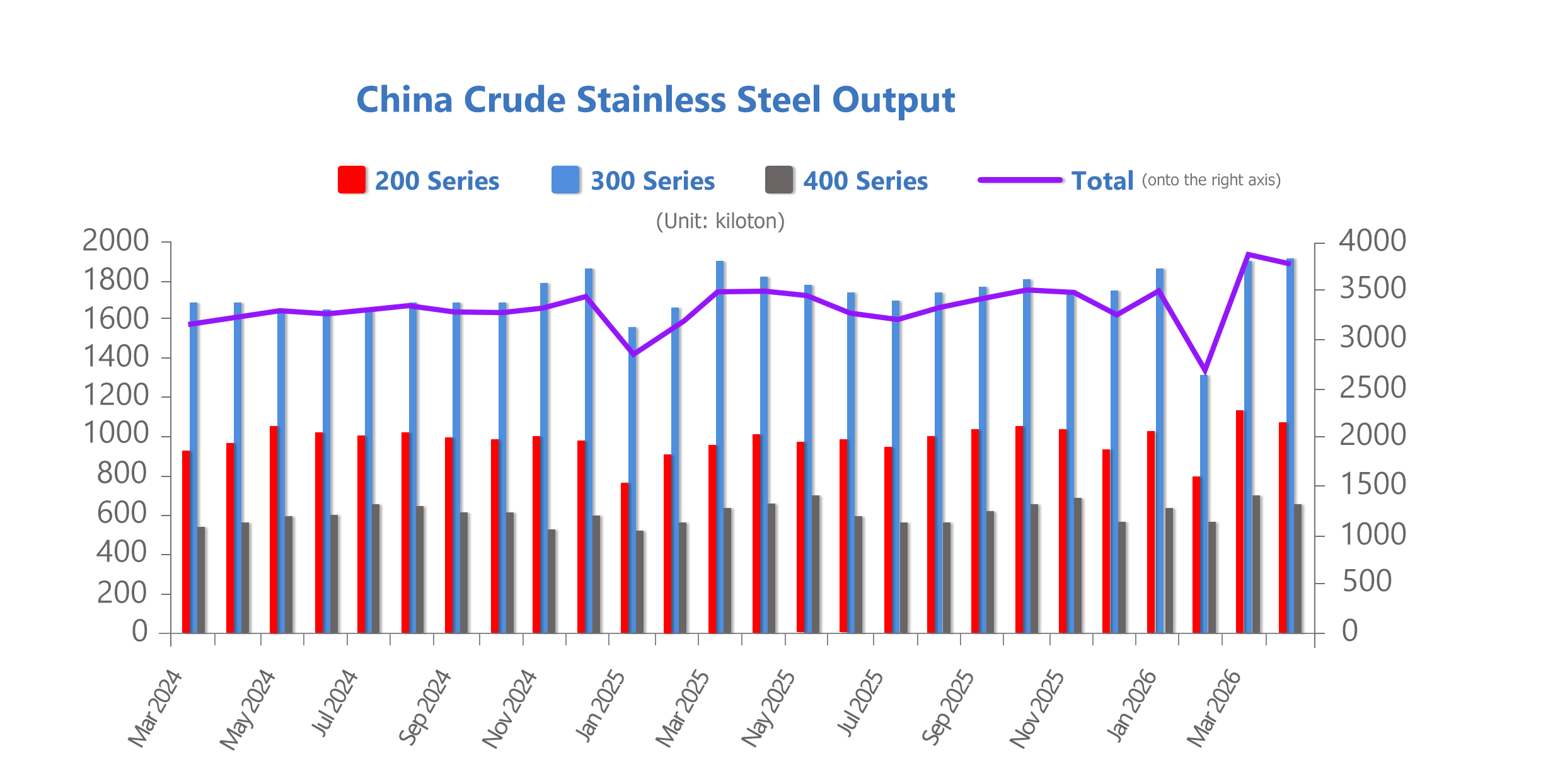

Production in June: Major Steel Mills Announce Maintenance; June Output Expected to Drop 4.4%

The Chinese stainless steel market entered a phase of planned production cuts and maintenance shutdowns in June, with the market expecting improvements in the supply-demand balance. Although seasonal demand remains weak during the traditional off-season, market participants expect the production cuts to help stabilize prices by reducing inventories and easing supply pressure.

Output Projections: China's crude stainless steel output in June is estimated to reach 3.58 million tons, down 4.4% month-on-month. The 200 series will see the most significant drop, with output expected to fall by 10.7% to approximately 940,000 tons. Output for the stainless steel 300 and stainless steel 400 series is projected to decrease by 1.6% and 2.9%, respectively. This reduction momentum is further supported by the Ministry of Industry and Information Technology's revised steel capacity replacement measures, which now bring stainless steel capacity under regulatory oversight.

Maintenance Plans: Several major stainless steel producers, including Baogang Desheng, Taigang Stainless Steel (TISCO), and Hualer Alloy, have announced June maintenance schedules. Total volume losses from these shutdowns are estimated to exceed 160,000 tons. A major producer in Jiangsu province expects to halt production for nearly 26 days starting June 6 for equipment maintenance, resulting in an output loss of about 65,000 tons. The impact is expected to be concentrated on stainless steel 200-series narrow strip products, potentially creating spillover effects on regional supply.

Market Response & Demand Constraints: Market participants expect these cutbacks to reduce the circulation of Stainless steel 200-series narrow strip materials and stainless steel 300-series cold-rolled stainless steel, helping to ease inventory pressures. However, given the sluggish downstream demand, it remains uncertain to what extent reduced supply will translate into price increases. June is traditionally a period of seasonal slowdown for Chinese stainless steel consumption, with weak demand in key terminal sectors like construction, kitchenware, home appliances, and industrial manufacturing. Pipe manufacturers report that order inflows and transaction volumes are lower than in previous years, prompting buyers to continue purchasing strictly on an as-needed basis. This cautious procurement strategy is expected to cap any substantial recovery in prices despite supply-side adjustments.

Export Pressures: The Chinese stainless steel export market remains under pressure. From January to April 2026, China's total stainless steel exports reached roughly 1.2 million tons, a year-on-year decline of 28.5%. Market sources attribute this to the implementation of export licensing requirements and rising trade protection measures in multiple overseas markets, which have reduced export competitiveness and shipping volumes.

Outlook for June

In May, the domestic stainless steel market was characterized by strong cost support, a weak recovery in demand, and high-level price fluctuations. Due to the interplay of multiple factors, the market rose before falling back, exhibiting highly distinct long-short crosscurrents.

Macro Environment: The new steel capacity replacement rules took effect this month, strictly controlling industry capacity expansion. The domestic economic recovery slowed down, the real estate market continued to weaken, and overseas manufacturing witnessed lackluster prosperity alongside increasing trade barriers, putting overall pressure on the market. In April, domestic stainless steel exports were 394,300 tons—up 27.12% month-on-month but down 11.93% year-on-year—indicating that the recovery in external demand lacks sustainability.

Raw Materials: Cost support from raw materials continued to strengthen due to Indonesia's suspension of 34 nickel ore mining projects and rising expectations of ferronickel production cuts. At the end of the month, nickel plate prices rose to US$21671/MT, a monthly gain of about 5%, while ferronickel quotes stood firm at high levels between US$172/nickel point. High-carbon ferrochrome quotes stabilized at US$1276/50 reference tons, whereas ferromolybdenum prices retraced from US$47164/MT at the beginning of the month to US$45820/ton. This dragged down the 316L market and caused a divergence in performance among different stainless steel grades.

Supply & Inventory Caps: Driven by raw materials, stainless steel prices peaked and then fell back this month. The base price for cold-rolled 4-foot rough edges stainless steel 304 was reported at US$2186/ton, down US$52 from the end of last month; medium bars were quoted at US$2270/MT, erasing an entire month of gains. The supply side remains generally sufficient, with April crude stainless steel output at 3.845 million tons. As of May 29, Wuxi inventory stood at 626,900 tons, and this high inventory level continues to suppress the upside potential for prices.

Supply-Side Mitigation: In May 2026, China's estimated crude stainless steel production scheduling was 3.7806 million tons, up 0.89% month-on-month and 9.17% year-on-year. Among this, the 300 series accounted for 2.0476 million tons, up 4.36% month-on-month, hitting a new high for the year as steel mill operating rates remained elevated due to repaired profit margins. Looking ahead to June, supply pressures are expected to ease marginally. On one hand, the industry is entering a capacity replacement cycle where certain inefficient, high-pollution capacities are gradually exiting, and new capacity rollouts are slowing down. On the other hand, following May's high production scheduling, some mills may conduct minor maintenance due to inventory pressures, causing supply growth to ease.

According to statistics, China’s 43 stainless steel producers churned out 3.7321 million tons of crude stainless steel in April 2026, down 1.68% month-on-month. Output of the 200-series stainless steel stood at 1.0935 million tons, slipping 6.63% month-on-month while rising 8.02% year-on-year, putting an end to two consecutive months of post-holiday production growth. Looking ahead to May, scheduled output of the 200-series is projected to fall further to 1.0325 million tons, a further month-on-month drop of 5.58%, which will continuously ease supply-side pressure.

Summary Prediction: Market sentiment for June remains cautiously balanced. Planned production cuts are expected to help draw down inventories and improve supply-demand fundamentals, potentially supporting a mild price recovery in the second half of the month. However, weak downstream demand, cautious buyer sentiment, and weakening nickel cost support may limit any significant upside. Consequently, the Chinese stainless steel market is expected to remain range-bound in the short term, and despite ongoing supply-side adjustments, June's average price may fall below May levels, with mainstream cold-rolled stainless steel 304 prices expected to run between US$2365/MT. Future focus should be placed on Indonesian nickel policies, inventory destocking speeds, and changes in terminal demand.

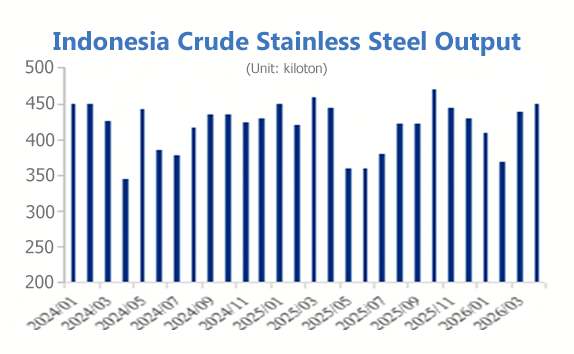

| 2026 Stainless Steel Production of China's 43 Major Steel Mills (Million Tons) | ||||||||

| Place of Production | Grade | March-2026 | April-2026 | May-2026 (Estimated) | April-2026 MoMΔ | April-2026 YoYΔ | May-2026 MoMΔ | May-2026 YoYΔ |

| China | 200 Series | 1.17 | 1.09 | 1.03 | -6.63% | 8.02% | -5.58% | 5.78% |

| 300 Series | 1.94 | 1.96 | 2.05 | 1.30% | 7.55% | 4.36% | 14.73% | |

| 400 Series | 0.688 | 0.677 | 0.676 | -1.66% | 1.59% | -0.15% | -3.79% | |

| Total | 3.8 | 3.73 | 3.76 | -1.68% | 6.56% | 0.63% | 8.45% | |

| Indonesia | 300 Series | 0.44 | 0.45 | 0.45 | 2.27% | 1.12% | - | 25.00% |

| China and Indonesia | Total | 4.24 | 4.18 | 4.21 | -1.27% | 5.94% | 0.56% | 10.01% |

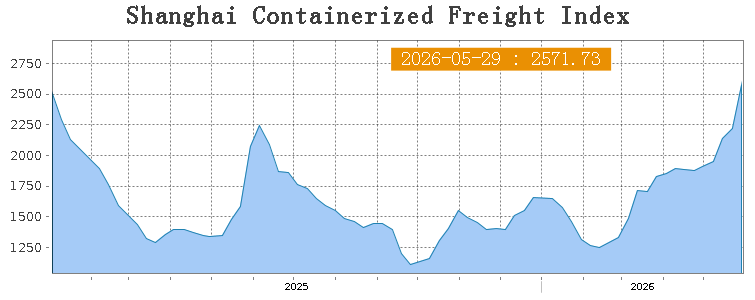

Sea Freight Keeps Climbing Up

Last week, the Chinese export container shipping market continued its positive trend, with freight rates on ocean routes maintaining an upward trajectory and the composite index climbing further. On May 29, the Shanghai Containerized Freight Index (SCFI) stood at 2571.73 points, up 15.9% from the previous period.

European Route

Shipping demand performed well, and supply-demand fundamentals were solid, driving market freight rates up sharply. On May 29, the market freight rate (ocean freight and ocean surcharges) from Shanghai Port to European base ports was $2,475/TEU, up 29.9% from the previous period.

Mediterranean Route

The market trend ran basically in step with the European route, with spot market booking prices continuing to rise. On May 29, the market freight rate from Shanghai Port to Mediterranean base ports was $3,750/TEU, up 16.9% from the previous period.

North American Route

Shipping demand maintained a steady growth trend, the supply-demand relationship was favorable, and the gains in spot market freight rates expanded. On May 29, freight rates from Shanghai Port to US West Coast and US East Coast base ports were $4,149/FEU and $5,333/FEU, up 31.5% and 23.6% respectively from the previous period.

Persian Gulf Route

Geopolitical conditions in the Middle East remained fundamentally stable, but the Strait of Hormuz is still a ways off from returning to normal shipping conditions. Freight rates ticked up slightly last week; on May 29, the rate from Shanghai Port to Persian Gulf base ports was $4,462/TEU, up 3.6% from the previous period.

Australia-New Zealand Route

Transportation demand grew steadily, pushing freight rates up further. On May 29, the rate from Shanghai Port to Australia-New Zealand base ports was $1,487/TEU, up 6.4% from the previous period.

South American Route

Shipping demand was stable with a positive outlook, and spot freight rates continued their upward climb. On May 29, the rate from Shanghai Port to South American base ports was $5,751/TEU, up 12.7% from the previous period.

The Driver Behind the Surcharge Surge: Cargo Front-Loading

June 1 marks the routine date for shipping lines to announce adjustments to the third-quarter Bunker Adjustment Factor (BAF). Different carriers use varying nomenclature; for example, Maersk refers to it as the FFF (Fossil Fuel Fee).

Analysts point out that the core driving force behind the recent surge in freight rates is that a large number of major European and American cargo owners (BCOs) front-loaded their shipments to beat the July 1 quarterly BAF hikes, causing booking demand to accelerate significantly. At that point, most large shippers will automatically face a new round of freight increases tied to quarterly BAF adjustments. Currently, what contract cargo owners are truly competing for is not a tariff window, but the last relatively low-fuel-cost window across all routes.

Entering June, these market expectations have further intensified. Conflicts have driven fuel prices up sharply, which in turn pushes up fuel surcharges. The impending effective date of the new quarterly fuel surcharges, combined with the continuous climb in freight rates, has further incentivized cargo owners to ship early to lock in prices. Meanwhile, shipping lines continue to tighten supply through slow steaming, blank sailings, and capacity adjustments. Demand is shifting forward, while supply is contracting.

Market sentiment is undergoing a transformation: moving from initial wait-and-see behavior, more and more cargo owners now worry that shipping will become costlier and harder to book later on, prompting them to push shipments forward. Since seasonal goods must be shipped regardless, the market has begun to display clear characteristics of panic shipping. War, fuel, peak season, slow steaming, congestion, container control, and market sentiment are forming a resonance as expected, reinforcing one another through layers of positive feedback. When expectations begin to dictate behavior, and behavior in turn solidifies expectations—such as cargo owners front-loading shipments out of fear of price hikes, which then drives rates even higher—the market ceases to operate on linear logic. At this stage, the market is driven not just by current realities, but heavily by expectations of the future.

The most critical variable remains the progress of negotiations between the US and Iran. If the two sides fail to reach even a first-stage framework agreement within the third quarter, the Strait of Hormuz risk premium will be hard to dissipate, keeping oil price baselines relatively high. Under these circumstances, fuel costs, BAF surcharges, and shipping market risk premiums will spill over into the fourth quarter to some extent, thereby raising the relative overall baseline for freight rates and costs in Q4.