Stainless Insights in China from February 5th to February 7th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,020 | 0 | 0.00% |

| Foshan | 2,060 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,930 | 5 | 0.26% | |

| Foshan | 1,950 | 7 | 0.38% | ||

| 304/NO.1 | ESS | Wuxi | 1,850 | 5 | 0.27% |

| Foshan | 1,875 | 0 | 0.00% | ||

| 316L/2B | TISCO | Wuxi | 3,445 | 37 | 1.13% |

| Foshan | 3,505 | 14 | 0.41% | ||

| 316L/NO.1 | ESS | Wuxi | 3,335 | 9 | 0.29% |

| Foshan | 3,290 | 9 | 0.29% | ||

| 201J1/2B | Hongwang | Wuxi | 1,210 | 0 | 0.00% |

| Foshan | 1,210 | 5 | 0.42% | ||

| J5/2B | Hongwang | Wuxi | 1,120 | 14 | 1.39% |

| Foshan | 1,110 | 5 | 0.46% | ||

| 430/2B | TISCO | Wuxi | 1,125 | 0 | 0.00% |

| Foshan | 1,135 | 5 | 0.45% |

TREND || Post-Holiday Recovery, Spot Prices Edge Up.

Stainless steel futures prices fluctuated strongly last week. During the first week after the Lunar New Year, market activity improved, with futures extending their upward momentum from the last trading day before the holiday. However, trading volumes remained relatively low, while open interest rebounded noticeably. Market sentiment diverged during the price recovery from recent lows. The main stainless steel futures contract closed at US$1970/MT last week, up 0.53% week-on-week, with a weekly high of US$1980/MT.

300 Series: Narrower Year-on-Year Inventory Growth, Futures and Spot Prices Rise.

304 spot prices stabilized with a slight upward trend. As of Friday, the mainstream base price for 304 cold-rolled stainless steel (4ft, private mills) in Wuxi stood at US$1890/MT, while hot-rolled prices rose to US$1855/MT, both up US$7/MT from pre-holiday levels. Post-holiday futures maintained an upward trajectory, driving spot prices higher. Most traders resumed operations last week, but downstream procurement remained cautious, with limited high-price transactions. During the holiday, shipments stalled, leading to a surge in arrivals. However, pre-holiday price cuts by traders and production cuts by mills resulted in lower post-holiday inventory accumulation compared to previous years, boosting market sentiment and supporting a mild rebound in spot and futures prices.

200 Series: Stabilizing Confidence, Prices Firm Up.

201 series prices strengthened last week. 201J2 cold-rolled prices rose to US$1095/MT (gross basis), while 201J1 cold-rolled and hot-rolled prices held firm at US$1185/MT and US$1170/MT, respectively. On Wednesday, 201J2 cold-rolled prices increased by US$14/MT, supported by consecutive gains in futures. Traders raised offers, but downstream demand remained tepid as some clients had yet to resume operations. Mills maintained production during the holiday, leading to inventory accumulation amid stagnant transactions.

400 Series: Holiday Stagnation Drives Inventory Surge.

430 prices trended upward. By Saturday, 430 cold-rolled prices in Wuxi ranged between US$1130 and US$1140/MT, while state-owned hot-rolled prices stood at US$1065/MT, both up US$7/MT from pre-holiday levels.

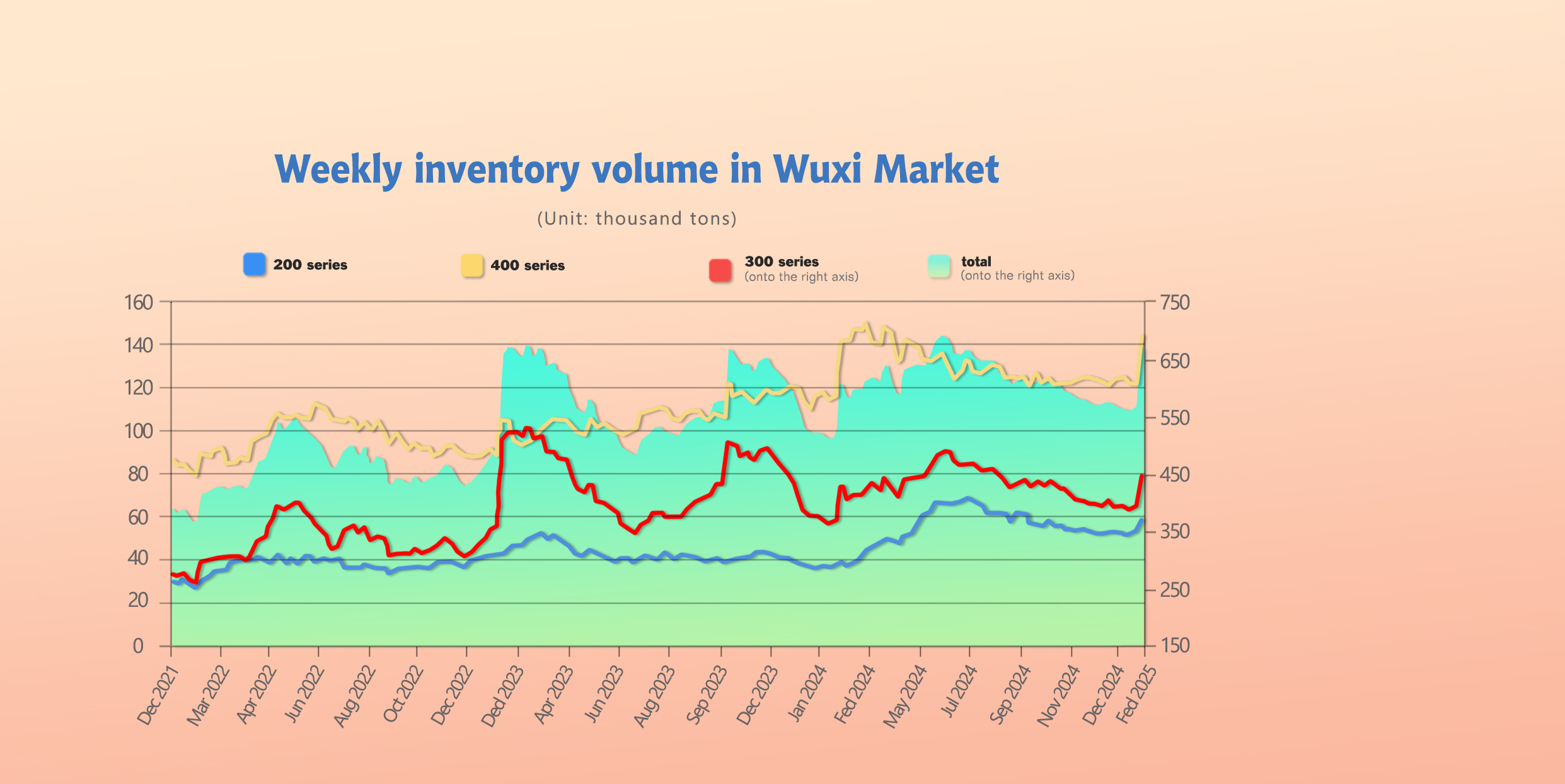

INVENTORY || Post-Holiday Inventory Accumulation Reaches 83,200 Tons.

As of February 6th, total inventory in Wuxi sample warehouses increased by 83,200 tons to 647,400 tons. Breakdown:

200 Series: 5,200 tons up to 57,900 tons.

300 Series: 54,300 tons up to 445,000 tons.

400 Series: 23,700 tons up to 144,500 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jan 22nd | 52,727 | 390,652 | 120,765 | 564,144 |

| Feb 6th | 57,912 | 444,975 | 144,489 | 647,376 |

| Difference | 5,185 | 54,323 | 23,724 | 83,232 |

300 Series: Transaction Halt Drives Inventory Surge.

Holiday-induced transaction halts and increased arrivals exacerbated supply-demand imbalances, resulting in seasonal inventory buildup.

200 Series: Arrivals Increase Amid Price Stability.

Shipments from mills like Beigang New Materials during the holiday drove inventory growth. Futures gains bolstered trader confidence, with offers remaining firm. Short-term 201J2 prices are expected to stabilize, with inventory likely to dip slightly next week.

400 Series: Pre-Holiday Mill Stockpiling.

Increased arrivals from mills like JISCO and TISCO during the holiday, combined with stagnant transactions, fueled inventory growth. Post-holiday futures supported firm offers, but downstream purchases remained need-based.

SUMMARY || Post-Holiday Recovery Tests Demand Amid Inventory Pressure.

Stainless steel prices fluctuated strongly last week. Post-holiday trading rebounded, but holiday arrivals and sales stagnation caused significant inventory buildup. Ample spot supplies now test downstream demand. Domestic macroeconomic policies require reinforcement desperately. It is expected that the stainless steel market will have a roller coaster ride in the short term.

300 Series: Raw material costs edged up, supporting prices. Post-holiday inventory pressure persists despite lower accumulation than last year. 304 cold/hot-rolled prices likely to follow futures trends.

200 Series: Mixed futures, higher copper/manganese costs strengthened 201 price support. Post-price hikes, market focus shifts to mill pricing. 201J2 prices to stabilize.

400 Series: High chromium prices rebounded, stabilizing 400 series costs. Post-holiday inventory growth moderated. Traders and downstream buyers gradually resuming operations may drive demand. 430 prices to remain firm.

MACRO || U.S. Imposes 25% Tariffs on All Steel and Aluminum Imports.

On Sunday (February 9th), U.S President Trump announced a 25% tariff on all U.S. steel and aluminum imports. The latest news clarify that the tax will be effected on March 4th. Since taking office on January 20th, Trump’s policies have undergone multiple adjustments. Last Friday, he suspended tariffs on small Chinese parcels—originally set to take effect February 4th alongside an additional 10% tariff. The suspension will last until “an adequate system for rapid tariff collection is established.” The U.S. Postal Service (USPS) temporarily halted China-origin parcels but reversed the decision within a day.

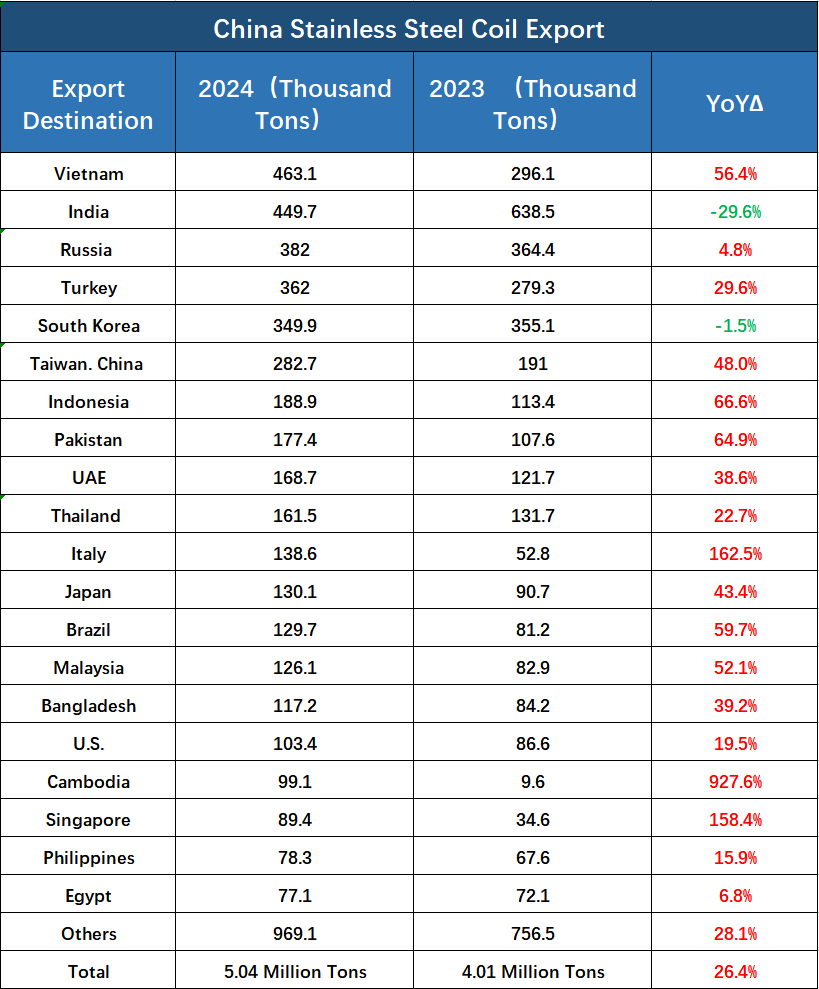

2024 Chinese Stainless Steel Exports Up 25.6% Year-on-Year.

In 2024, China’s stainless steel exports surged, with notable growth to Vietnam (+167,000 tons, up 56.4%).

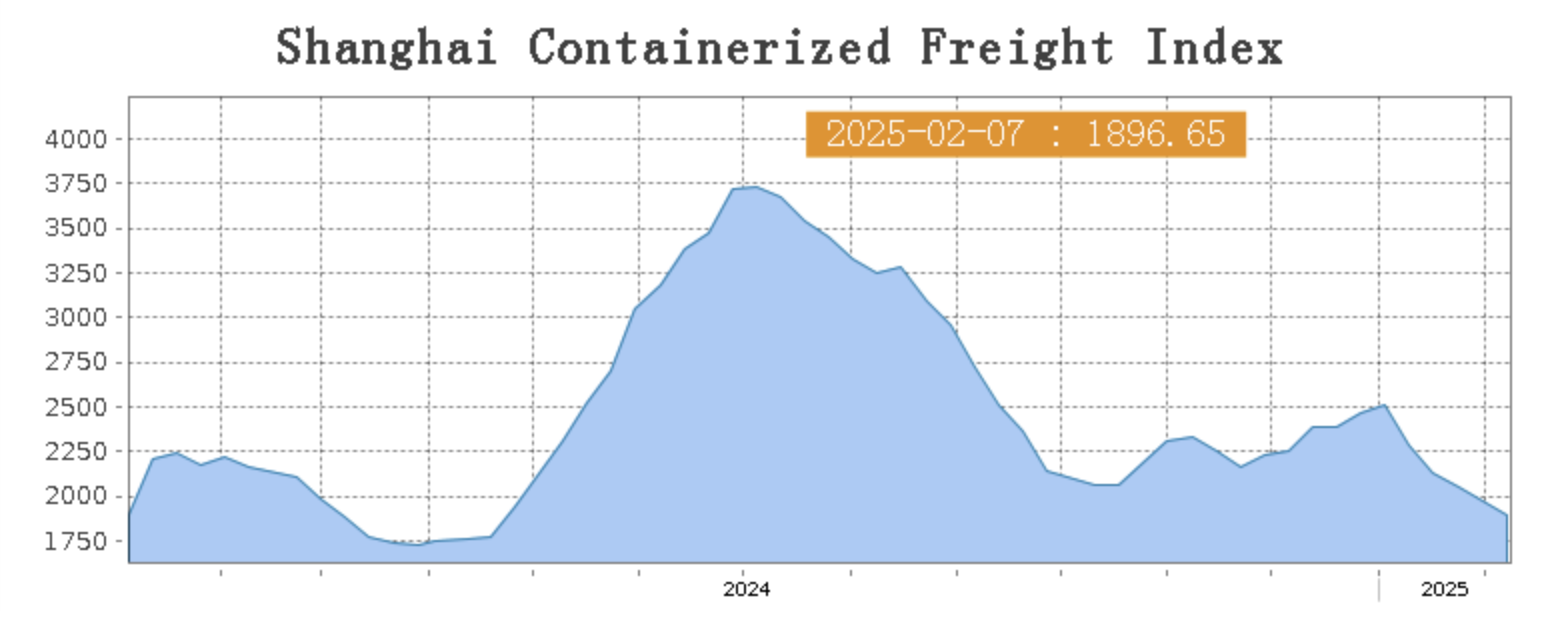

SEA FREIGHT || Slow Market Recovery, Freight Rates Decline.

Post-holiday recovery in China’s container shipping market remained sluggish. On February 7th, the Shanghai Containerized Freight Index (SCFI) fell 7.3% to 1,896.65 points.

Europe/ Mediterranean:

Last week, the shipping market was generally in a recovery phase. Shipping demand is flat, and shipping companies are mostly taking temporary shutdowns and combined shifts to balance supply and demand. Spot market booking prices continue to decline.

On 7th February, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1805/TEU, which fell by 15.9%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$3036/TEU, which dropped by 5.3%.

North America:

President Trump has begun to take measures to increase tariffs shortly after taking office, which will lead to greater uncertainty in the North American routes in the future. Last week, the shipping market performed weakly, transportation demand growth was sluggish, and market freight rates continued to show an adjustment trend.

On 7th February, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$3932/FEU and US$5490/FEU, reporting a 4.5% and 5.0% down accordingly.

The Persian Gulf and the Red Sea:

On 7th February, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf dipped 1.6% to $1,191/TEU.

Australia/ New Zealand:

On 7th February, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New plunged 20.7% to $1,085/TEU.

South America:

On 7th February, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 11.1% to $3,435/TEU.