Stainless Insights in China from February 10th to February 14th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,035 | 0 | 0.00% |

| Foshan | 2,075 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,930 | -10 | -0.56% | |

| Foshan | 1,950 | -13 | -0.68% | ||

| 304/NO.1 | ESS | Wuxi | 1,860 | -4 | -0.22% |

| Foshan | 1,880 | -7 | -0.39% | ||

| 316L/2B | TISCO | Wuxi | 3,475 | 3 | 0.10% |

| Foshan | 3,540 | 4 | 0.12% | ||

| 316L/NO.1 | ESS | Wuxi | 3,365 | 9 | 0.28% |

| Foshan | 3,335 | 14 | 0.44% | ||

| 201J1/2B | Hongwang | Wuxi | 1,230 | 10 | 0.88% |

| Foshan | 1,215 | -2 | -0.22% | ||

| J5/2B | Hongwang | Wuxi | 1,125 | -3 | -0.27% |

| Foshan | 1,120 | -2 | -0.24% | ||

| 430/2B | TISCO | Wuxi | 1,145 | 9 | 0.92% |

| Foshan | 1,145 | 2 | 0.17% |

TREND || Rising Raw Material Costs Amid Slow Post-Holiday Demand Recovery.

Last week, stainless steel spot prices in Wuxi followed a volatile pattern, initially rising before retreating. Macro headwinds, including Trump’s tariff announcements, Fed Chair Powell’s hawkish remarks, and weakened rate-cut expectations, intensified price fluctuations. Spot demand recovered slowly, while arrivals increased, driving inventory accumulation. By Friday, the main stainless steel futures contract fell US$14.5/MT to US$1940/MT, down 2.31% week-on-week, with a weekly low of US$1930/MT. Spot prices declined by US$7-US$14/MT. Post-holiday demand recovery lagged, with tepid trading activity and low-price transactions dominating the off-season market.

300 Series: Inventory Accumulation Persists, Prices Retreat After Rally.

304 spot prices dipped slightly. As of Friday, the mainstream base price for 304 cold-rolled stainless steel (4ft, private mills) in Wuxi dropped US$14/MT to US$1880/MT, while hot-rolled prices fell US$7/MT to US$1860/MT. Early-week price hikes by mills like Tsingshan briefly boosted sentiment, but futures pullbacks later prompted cautious trading. Inventory continued to accumulate amid sluggish demand, with buyers prioritizing rigid needs.

200 Series: Prices Stabilize Amid Expanded Discounts.

201 series prices fluctuated. 201J2 cold-rolled prices settled at US$1095/MT(gross basis), while 201J1 cold-rolled and hot-rolled prices closed at US$1200/MT and US$1180/MT, respectively. After a US$21/MT increase on Monday, 201J1 cold-rolled prices fell US$7/MT on Tuesday, followed by a US$7 drop for 201J2 on Thursday. Traders offered discounts to stimulate sales, but downstream buyers remained hesitant, leading to mild inventory growth.

400 Series: Cost Support Stabilizes Prices.

430 prices diverged. State-owned 430 cold-rolled prices in Wuxi rose US$4.1/MT to US$1150/MT-US$1150/MT, while hot-rolled prices held steady at US$1075/MT. High-chromium raw material prices stabilized, supporting 400 series costs. Post-holiday arrivals were limited, driving inventory declines. With downstream demand gradually recovering, 430 prices are expected to remain firm.

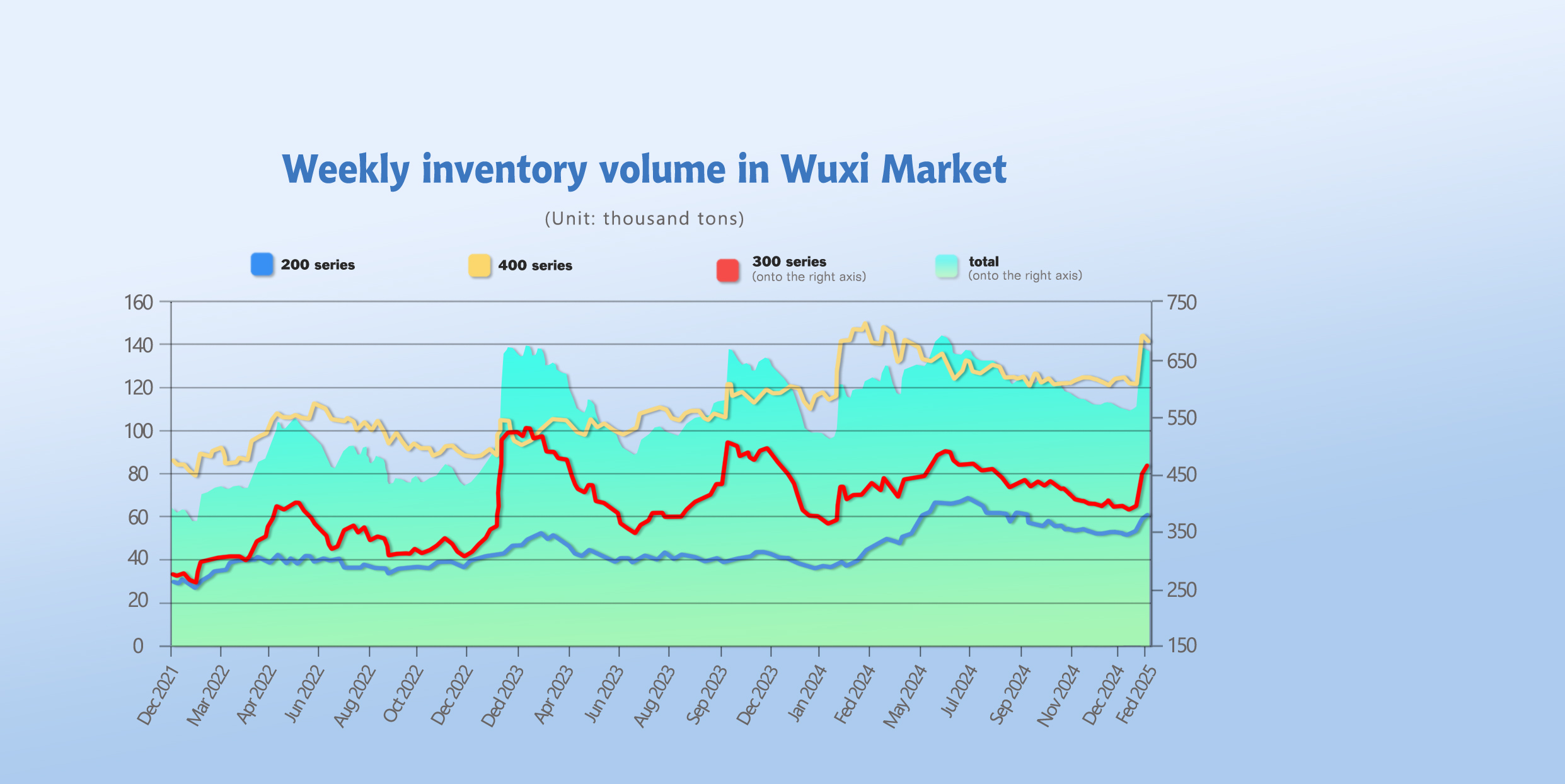

INVENTORY || Slow Demand Recovery Drives Further Inventory Growth.

As of February 13th, total inventory in Wuxi sample warehouses increased by 19,700 tons to 667,000 tons. Breakdown:

200 Series: 3,600 tons up to 61,600 tons.

300 Series: 20,900 tons up to 465,800 tons.

400 Series: 4,900 tons down to 139,600 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Feb 6th | 57,912 | 444,975 | 144,489 | 647,376 |

| Feb 13th | 61,558 | 465,846 | 139,634 | 667,038 |

| Difference | 3,646 | 20,871 | -4,855 | 19,662 |

300 Series: Persistent Oversupply Pressures Prices.

Mill restarts boosted supply, while demand recovery remained sluggish. Macro uncertainties, including Trump’s tariffs and weak rate-cut expectations, weighed on sentiment. Inventory is expected to keep rising, pending demand improvements.

200 Series: Increased Arrivals Drive Inventory Growth.

Higher arrivals from mills like Beigang intensified supply pressure. Traders offered discounts for 201J2 cold-rolled products, but downstream purchases stayed cautious.

400 Series: Inventory Declines on Tight Supply.

Reduced arrivals from mills like JISCO and TISCO tightened supply. Post-holiday demand recovery accelerated inventory drawdowns, with 430 prices expected to stabilize.

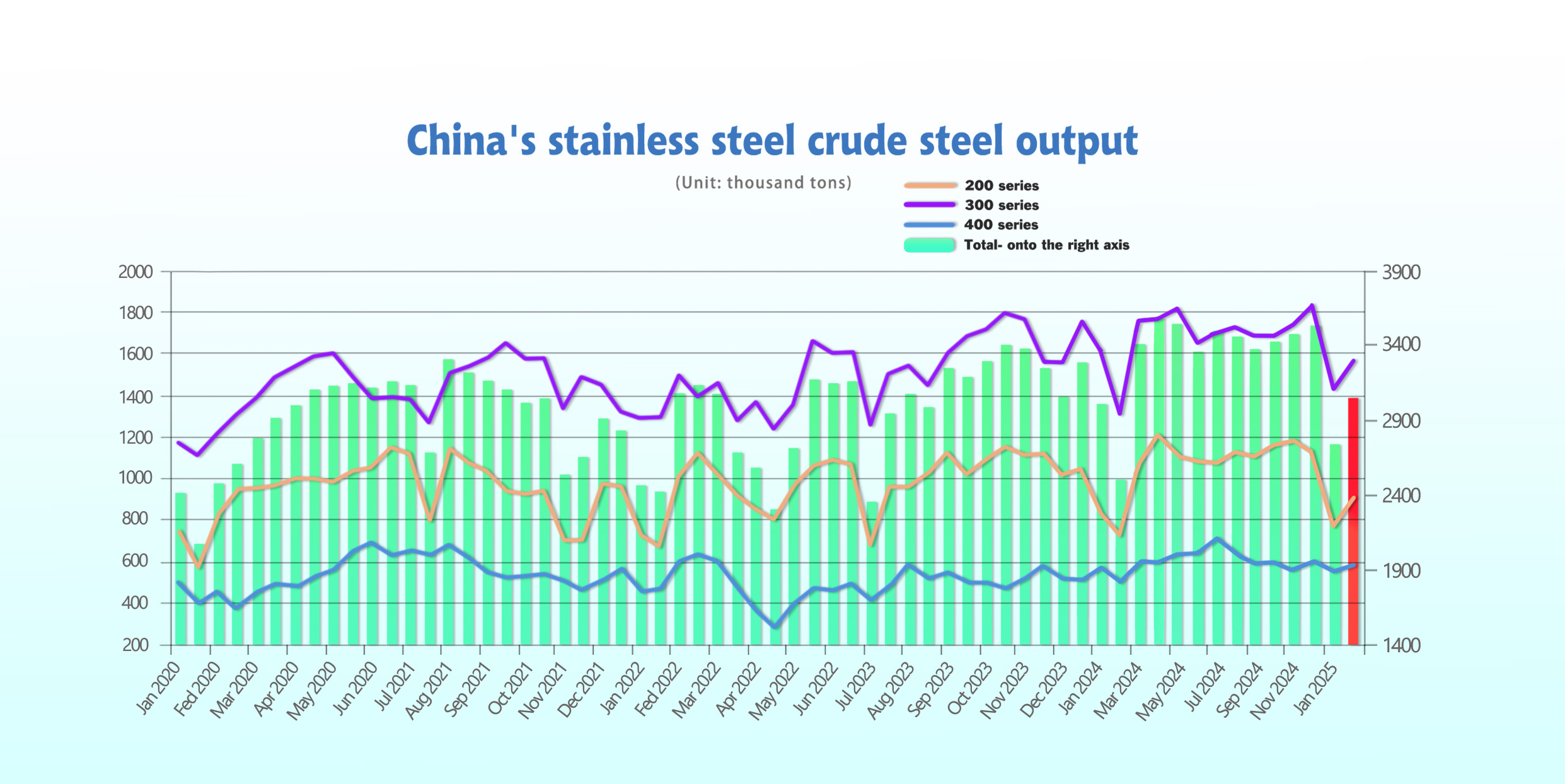

January Stainless Steel Crude Output Falls by 780,000 Tons Month-on-Month

In January, domestic stainless steel output contracted sharply due to low mill margins and holiday-related production cuts. Large-scale mills produced 2.7452 million tons of crude steel, down 781,800 tons (-22.17%) month-on-month and 276,000 tons (-9.13%) year-on-year.

200 Series: 762,700 tons (-31.69% MoM; -9.92% YoY).

300 Series: 1.4276 million tons (-21.45% MoM; -10.99% YoY).

400 Series: 554,900 tons (-6.41% MoM; -2.73% YoY).

February’s planned output is expected to rebound by 290,000 tons to ~3.04 million tons but remains below Q4 2024 averages. Post-holiday demand recovery and rising raw material costs will pressure prices, with mills likely to adjust production based on profitability.

RAW MATERIAL || The Philippines Plans Raw Nickel Export Ban from June 2025.

The Philippines is advancing a bill to ban raw nickel ore exports starting June 2025, aiming to boost domestic downstream industries. This policy risks disrupting Indonesia’s nickel supply chain, as Indonesia imported over 1 million tons of Philippine nickel ore (valued at $451.9 million) from January–November 2024. The ban may tighten global nickel supply and push prices higher.

The Philippines' nickel export ban will not only impact Indonesia's nickel industry, but also affect global nickel inventories, and may even drive up nickel prices. However, Indonesia's Ministry of Energy and Mineral Resources has not yet confirmed whether the country's nickel prices will rise as a result, pointing out that nickel prices are affected by multiple factors other than supply and demand.

The Philippines' export ban will have a profound impact on the global nickel market, especially the trend of nickel prices. Indonesia, as the world's second largest nickel producer, is expected to produce 220 million tons of nickel in 2025, which is close to the target of 240 million tons in 2024.

Last week, high-nickel pig iron (NPI) prices strengthened. Supply tightness in Indonesia due to weather and regulatory delays lifted NPI costs, with transactions reaching US$136/Nickle point. Rising freight costs from the Philippines further squeezed Chinese NPI producers’ margins. Despite weak stainless steel trends, NPI prices are expected to remain firm.

SUMMARY || Policy Support Needed Amid Macro Challenges.

Stainless steel prices weakened last week. Slow demand recovery, rising inventories, and elevated raw material costs pressured mill margins. Market focus remains on policy stimulus, mill production adjustments, and demand trends.

300 Series: Cost-driven price volatility to persist amid inventory pressure.

200 Series: Weak demand and inventory growth may keep 201J2 prices subdued.

400 Series: Tight supply and recovering demand to stabilize 430 prices.

MACRO || Global Demand Slump, Tariff Barriers Intensify.

Outokumpu Halts U.S. Expansion Plans

Finnish firm Outokumpu paused U.S. expansion and Finnish nuclear investments due to weak global stainless demand and import pressures. Despite favorable tariffs, market uncertainty forced delays. The company reported a Q4 operating loss of €3 million, better than expected, and forecasts 10–20% shipment growth in Q1 2025.

India Proposes 15–25% Safeguard Duty on Chinese Steel

India is investigating provisional tariffs (15–25%) on Chinese steel imports to counter "unfair competition." The move follows declining Indian steel exports amid weak global demand.

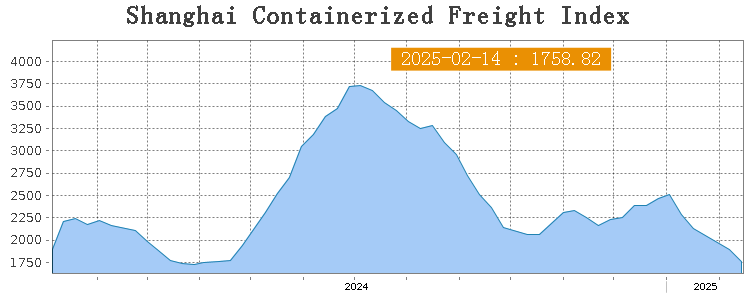

SEA FREIGHT || Freight Rates Continue Downward Trend.

Last week, freight rates on all ocean routes in China's export container shipping market continued to adjust, and the comprehensive index continued to decline. According to the latest released data, the Caixin China Composite PMI in January fell to 51.1, and both the manufacturing and service PMI slightly declined, but both continued to remain above the prosperity line. On February 14th, the Shanghai Containerized Freight Index (SCFI) fell 7.3% to 1,758.82 points.

Europe/ Mediterranean:

Last week, transportation demand was weak, the supply and demand balance was not ideal, and spot market booking prices continued to fall.

On 14th February, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1608/TEU, which fell by 10.9%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2815/TEU, which dropped by 7.3%。

North America:

The United States continues to introduce measures to impose additional tariffs, which will increase the risk of trade conflicts and cause greater uncertainty to the North American route.

On 14th February, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$3544/FEU and US$4825/FEU, reporting 9.9% and 12.1% down accordingly.

The Persian Gulf and the Red Sea:

On 14th February, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf dipped 3.9% to $1,144/TEU.

Australia/ New Zealand:

On 14th February, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New plunged 10.9% to $967/TEU.

South America:

On 14th February, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 2.2% to $3,359/TEU.