Stainless Insights in China from March 3rd to March 7th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,045 | 10 | 0.51% |

| Foshan | 2,085 | 10 | 0.50% | ||

| Hongwang | Wuxi | 1,945 | 18 | 1.00% | |

| Foshan | 1,975 | 18 | 0.99% | ||

| 304/NO.1 | ESS | Wuxi | 1,855 | 18 | 1.44% |

| Foshan | 1,900 | 25 | 1.11% | ||

| 316L/2B | TISCO | Wuxi | 3,480 | 19 | 0.59% |

| Foshan | 3,565 | 19 | 0.57% | ||

| 316L/NO.1 | ESS | Wuxi | 3,355 | 19 | 0.61% |

| Foshan | 3,355 | 22 | 0.70% | ||

| 201J1/2B | Hongwang | Wuxi | 1,235 | 7 | 0.62% |

| Foshan | 1,240 | 11 | 1.00% | ||

| J5/2B | Hongwang | Wuxi | 1,135 | 10 | 0.96% |

| Foshan | 1,140 | 13 | 1.23% | ||

| 430/2B | TISCO | Wuxi | 1,150 | 0 | 0.00% |

| Foshan | 1,135 | 0 | 0.00% |

TREND || Policy Expectations Drive Price Increases.

The opening of China's "Two Sessions" on Wednesday significantly boosted stainless steel market sentiment. By Friday's close, the main stainless steel futures contract 2505 closed at US$1985/MT, with a weekly increase of 1.17%. The weekly high reached US$2000/MT, and the low was US$1950/MT. Stainless steel market prices rose across the board last week. Specifically, the 304 variety saw a wave of price increases, with gains ranging from US$14-US$42/MT. The 316L variety also increased by US$21-US$42/MT. The 201 variety also showed an upward trend, with an increase of US$7-US$21/MT. In contrast, the 400 series varieties saw partial downward adjustments, with declines ranging from US$7-US$28/MT.

300 Series: Cost Increases & Positive Factors Boost, Weekly Turnover Improves.

Last week, 304 spot market prices slightly increased. As of Friday, the mainstream base price for 304 private cold-rolled four-foot in Wuxi was reported at US$1920/MT, an increase of US$28/MT from last week; the price of private hot-rolled was reported at US$1910/MT, an increase of US$42/MT from last week. Weekly futures prices fluctuated upwards, and ferronickel quotations were strong, with merchants holding firm on prices. With the release of positive signals from the "Two Sessions" and the sharp rise in Tshingshan's opening, market sentiment warmed up, spot quotations mostly increased, and the market saw a wave of procurement, with weekly turnover improving.

200 Series: Spot Prices Continue to Rise, Market Confidence Increases.

Last week, 201 prices mainly ran strongly and steadily, with 201J2 cold-rolled reported at US$1115/MT; 201J1 cold-rolled reported at US$1215/MT, and 201J1 hot-rolled quoted at US$1180/MT. On Monday, Tshingshan Steel Plant opened, raising the cold-rolled prices of 201J1 and 201J2 by US$7/MT, and on Tuesday, raising the hot-rolled price of 201J2 by US$7/MT. Market sentiment is optimistic, traders have followed suit with price increases, and inquiries and purchases from the consumer side are relatively active, with a slight destocking of cold and hot-rolled inventory within the week.

400 Series: Raw Material Prices Remain Stable, Finished Product Prices Slightly Increase.

Last week, 430 cold-rolled quotations in the Wuxi market remained at US$1155/MT; 430/NO.1 mainstream quotations remained stable at US$1075/MT, running smoothly. In terms of the spot market, last week, steel plant arrivals were fewer, inventory destocking accelerated, and 400 series market spot inventory saw a significant decline, with 400 series stainless steel price support still acceptable.

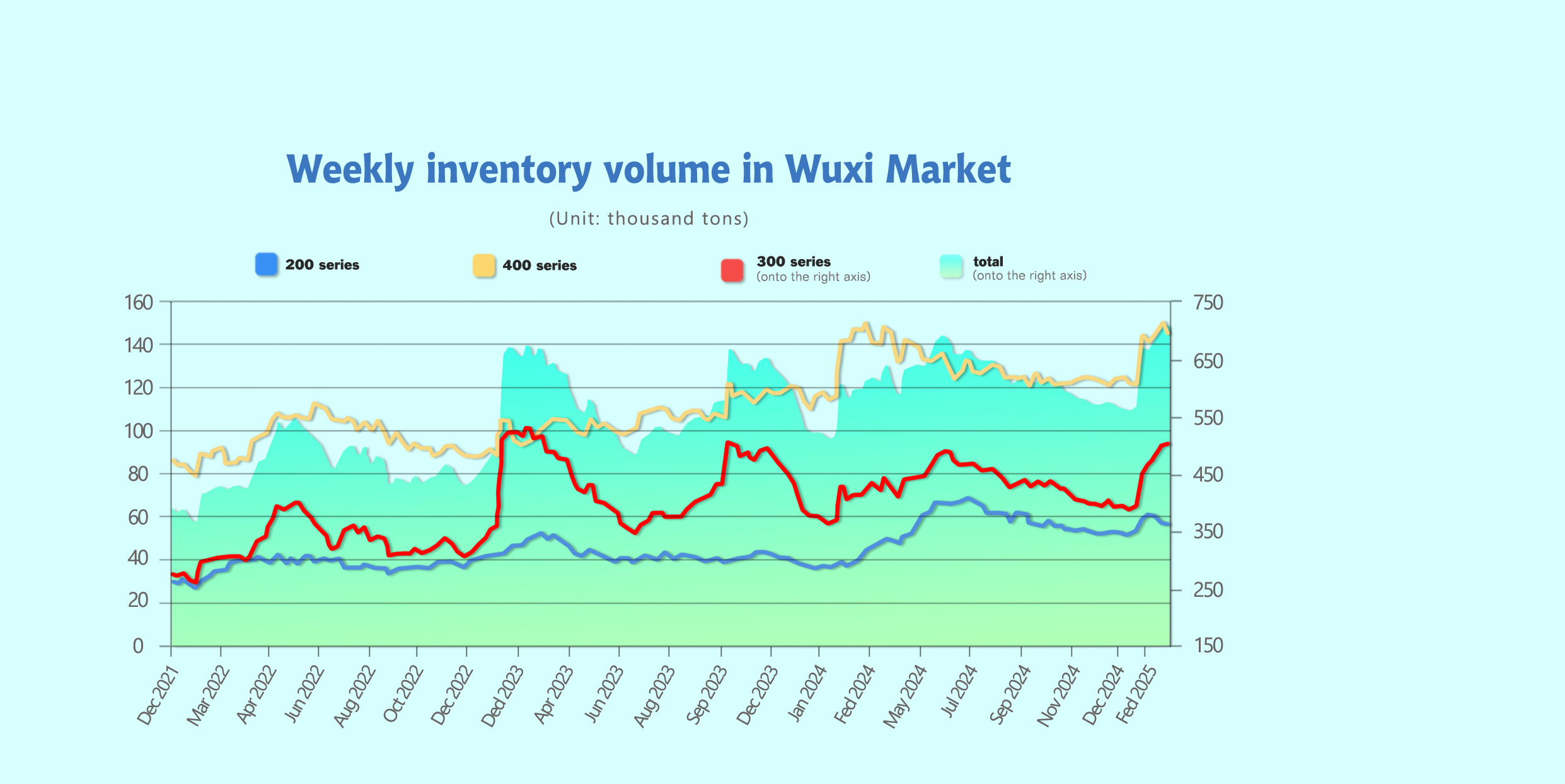

INVENTORY || First Inventory Reduction After the Spring Festival.

As of March 6th, total inventory in Wuxi sample warehouses decreased by 1,999 tons to 701,244 tons. Breakdown:

200 Series: 1,688 tons down to 56,244 tons.

300 Series: 4,287 tons up to 500,027 tons.

400 Series: 4,598 tons down to 144,973 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Feb 27th | 57,932 | 495,740 | 149,571 | 703,243 |

| Mar 6th | 56,244 | 500,027 | 144,973 | 701,244 |

| Difference | -1,688 | 4,287 | -4,598 | -1,999 |

200 Series: Price Adjustments and Increased Turnover Accelerate Inventory Destocking.

In the short term, 201J2 prices may maintain a stable to strong run, and it is expected that inventory may continue to destock next week, with a focus on steel plant trends and market turnover.

300 Series: Futures and Spot Prices Rise Together, Cold and Hot-Rolled Increase and Decrease Differently.

With the convening of the "Two Sessions," market expectations have risen, and the probability of policy issuance is expected to increase next week, with overall sentiment on the strong side. With the increase in spot prices, market purchases have improved, the supply and demand pattern has improved, and inventory is expected to decline next week, with a focus on steel plant trends and market turnover.

400 Series: Cost Increases, Reduced Arrivals, Inventory Turns from Increase to Decrease.

Last week, arrivals of both cold and hot-rolled were fewer. A small amount of Jiuquan cold-rolled resources arrived, and the inventory decline of Taiyuan Iron and Steel's cold and hot-rolled was significant, market supply pressure eased, and inventory destocking accelerated.

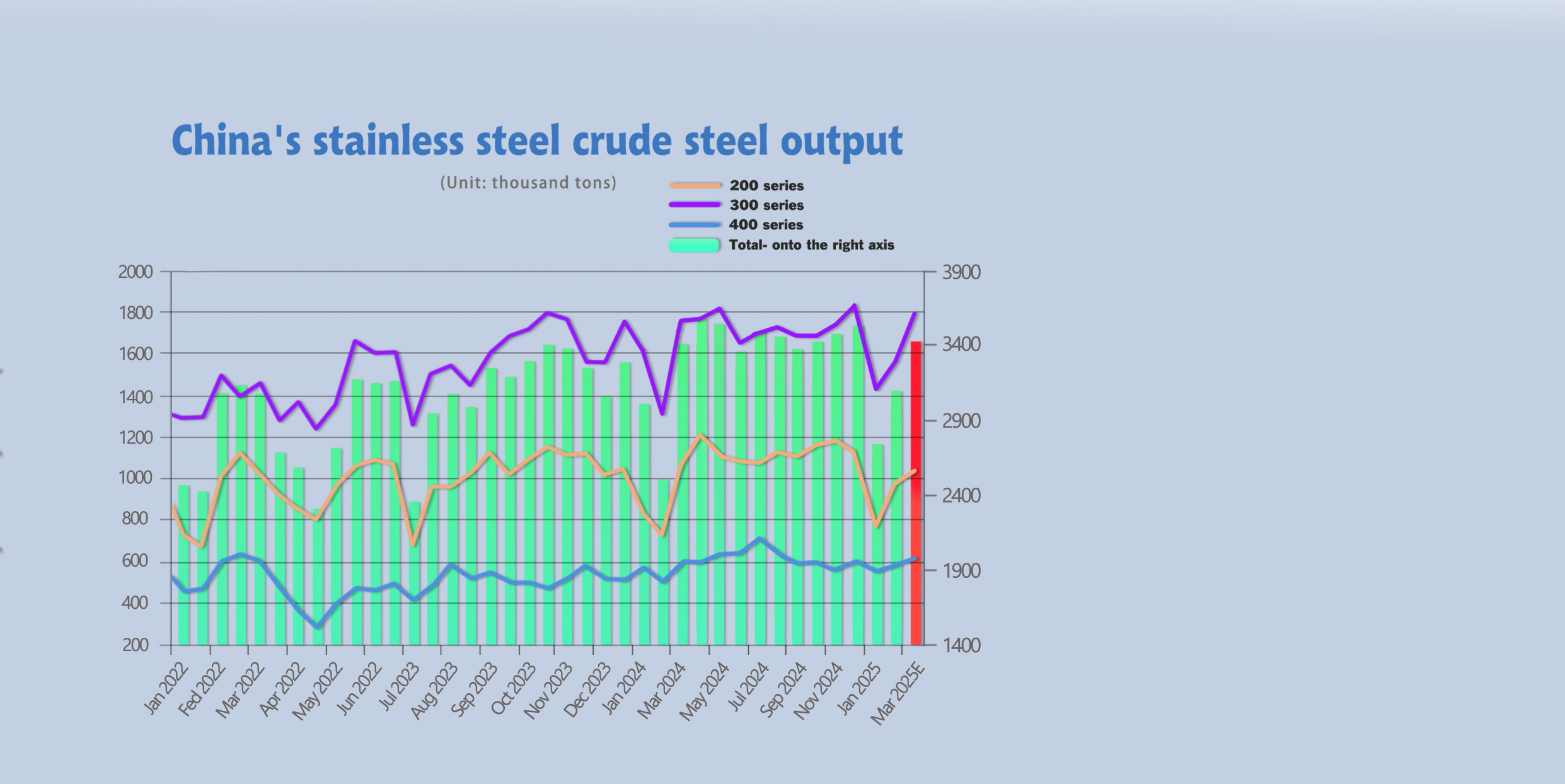

In February 2025, the domestic stainless steel crude steel output of enterprises above designated size was 3.1025 million tons, an increase of 357,300 tons from the previous month, an increase of 13.01%; an increase of 583,500 tons from the same period last year, an increase of 23.17%.

Output of all series rebounded in February. The output details of each series are as follows:

200 series: 973,200 tons, an increase of 210,500 tons (27.6%) from the previous month, and an increase of 252,600 tons (35.06%) from the same period last year.

300 series: 1,559,900 tons, an increase of 132,300 tons (9.27%) from the previous month, and an increase of 252,500 tons (19.31%) from the same period last year.

400 series: 569,300 tons, an increase of 14,400 tons (2.6%) from the previous month, and an increase of 78,400 tons (15.97%) from the same period last year.

Steel mills production scheduling for March continues to increase. According to preliminary statistics, the domestic stainless steel crude steel scheduled output in March 2025 will increase by 330,000 tons from the previous month to around 3.43 million tons, of which the scheduled output of the 300 series will increase by 240,000 tons from the previous month to 1.8 million tons, the scheduled output of the 200 series will increase by 60,000 tons from the previous month to 1.03 million tons, and the scheduled output of the 400 series will increase by 40,000 tons from the previous month to 610,000 tons.

RAW MATERIAL || Stainless Steel Scheduling Increases, Raw Material Costs Expected to Rise.

High-Nickel Iron

Last week, high-nickel iron prices went up. With multiple steel plants purchasing within the week, high-nickel iron prices rose. Tsingshan released the first round of bidding prices for high-nickel iron in March at US$136.5/nickel point (DDU including tax); the transaction price of high-nickel pig iron in a steel plant in Liyang Stainless steel was US$140/nickel point (EXW including tax).

According to data from China United Metals, the output of nickel iron in Indonesia in February was 147,603 tons (metal volume), a decrease of 4.79%. With stainless steel scheduling increasing to 3.4 million tons in March, supported by demand, high-nickel iron is expected to run strong in the short term.

High-Carbon Ferrochrome

Last week, high-carbon ferrochrome ran steadily, with domestic steel plant zero-order purchase prices around US$11072.4/MT. At the beginning of the week, Tshingshan announced the long-term purchase price of high-carbon ferrochrome in March at US$974.2/50 reference tons (cash including tax to the factory price); the price was the same as in February.

At present, the domestic production cost of high-carbon ferrochrome is around US$1083.5/50 reference tons, but domestic ferrochrome plant production is losing money, the resumption of production is disrupted, and under cost pressure, plant raw material procurement demand is weakened, and high-priced chrome ore is difficult onclude transactions at high prices for chrome ore. In March, the production scheduling of stainless steel increased significantly. Coupled with the fact that the production volume of ferrochromium remained at a low level, driven by rigid demand, the price of ferrochromium is expected to remain firm.

SUMMARY || Stainless Steel Prices Expected to Remain Stable and Rise in the Short Term.

The current stainless steel market is showing a complex situation driven by both rising costs and macro sentiment. On the cost side, the prices of raw materials such as high-nickel iron and high-carbon ferrochrome have risen, increasing the production cost of stainless steel. At the same time, positive factors at the macro level have stimulated market optimism, and manufacturers' willingness to hold prices is extremely strong, with product quotations being raised one after another. However, the slow release of downstream demand and high prices have made buyers cautious in purchasing, and the wait-and-see atmosphere has become increasingly strong, further weakening the trading atmosphere. At present, downstream users have low acceptance of high prices, and the contradiction between market supply and demand is prominent. In this situation, although stainless steel prices remain firm in the short term, the range of price fluctuations is limited due to the suppression of downstream demand.

300 Series: The strong operation of raw material quotations and the release of favorable domestic policies from the "Two Sessions" have boosted the rebound of the market. Market sentiment has warmed up, and market purchases have increased. With the gradual recovery of traditional peak season demand and the support of favorable policies, inventory pressure may be alleviated, and stainless steel spot prices are expected to run strongly in the short term.

200 Series: The market continues to strengthen, and macro policy expectations have boosted market confidence. Beigang New Materials has a maintenance plan from March to June, the output of 200 series crude steel has decreased, and market supply pressure has weakened. In addition, raw material copper has rebounded from a low level, and the cost support has become stronger. Downstream demand is gradually recovering, and 201J2 cold-rolled prices are expected to maintain a stable to strong run in the short term.

400 Series: Overall, raw material cost support is relatively stable, but due to the lack of upward momentum in prices, production enterprises' losses are difficult to reverse. Last week, 400 series stainless steel spot supply has decreased, and inventory consumption has accelerated. It is expected that 430 prices will continue to run smoothly next week.

MACRO || China's Exports Show Seasonal Decline in the First Two Months of 2025.

In January-February 2025, exports in US dollar terms increased by 2.3% year-on-year (10.7% in December 2024), and imports decreased by 8.4% year-on-year (1.0% in December 2024), both lower than market expectations (Bloomberg's market expectations for exports and imports were 5.9% and 1.0%, respectively). The decline in export growth was mainly due to seasonal factors. The foreign demand side showed marginal improvement in manufacturing and marginal decline in services, which was not the main reason for the decline in export growth. The landing of tariffs may have a certain counteracting effect on the front-loading effect of exports. Imports were relatively weaker than seasonal factors.

The decline in export growth was mainly due to seasonal factors. From a month-on-month perspective, the average monthly export volume in January-February 2025 decreased by 65.7 billion US dollars from December 2024, between 2017 and 2022, which had similar Spring Festival dates (59.5 and 70.6 billion US dollars, respectively); the month-on-month change rate was -19.6%, higher than -28.5% in 2017 and -20.8% in 2022, which had similar Spring Festival dates. From a year-on-year perspective, the base has increased. The year-on-year growth rate of exports in January-February 2024 was 7.1%, higher than 2.1% in December 2023.

The foreign demand side showed marginal improvement in manufacturing and marginal decline in services. In January and February 2025, the manufacturing PMI of developed countries was 49.3% and 50.0%, respectively, an improvement from 48.2% in December 2024; while the service PMI was 52.2% and 50.9%, respectively, a decrease from 54.0% in December 2024. We believe that the overall foreign demand side is stable and is not the main reason for the decline in export growth.

The landing of tariffs may have a certain counteracting effect on the front-loading effect of exports. By destination, exports to the United States, the European Union, and ASEAN in January-February 2025 increased by 2.3%, 0.6%, and 5.7% year-on-year, respectively (15.6%, 8.8%, and 18.9% in December 2024), and the month-on-month comparison was between 2017 and 2022, which had similar seasonal patterns. For the United States, the average monthly export volume to the United States in January-February 2025 decreased by 23% from December 2024, while the same period in 2017 and 2022 was -25% and -19%, respectively. Although the 10% tariff imposed by the United States on China from February 4, 2025 [1] may have had a certain negative impact on China's exports to the United States, due to factors such as the performance of previously signed contracts, the impact may not have been fully reflected in the export data for January-February. In addition, if market players expect that tariffs may be further increased in the future, it may also accelerate the short-term front-loading effect of exports.

Regarding future exports, it is expected that the overall US economy may slow down in the first half of the year. Attention should be paid to the uncertainty of tariffs. On the one hand, it may have a certain negative impact on China's exports, but in the short term, there may be a certain front-loading effect of exports to counteract this, so that the negative impact may not be fully apparent in the short term. The pressure may be more concentrated in the second quarter, and the export growth rate in the first half of the year may slow down compared with 2024.

| Export Category | 2025-Feb | 2024-Dec | 2024-Nov | 2024-Oct |

| Cotton Yarns and Products | -2 | 17.2 | 9.3 | 15.6 |

| Furniture and Parts | -15.5 | 3.1 | -2.7 | 2.5 |

| Steel Products | -3.9 | 11.8 | 2.6 | 24.4 |

| Auto Part and Accessory | 0.6 | 15.6 | 5.5 | 14.7 |

| Garments and Accessory | -6.9 | 6.2 | 3.8 | 6.8 |

| Plastic Products | -8.3 | 4.2 | 3.4 | 8.6 |

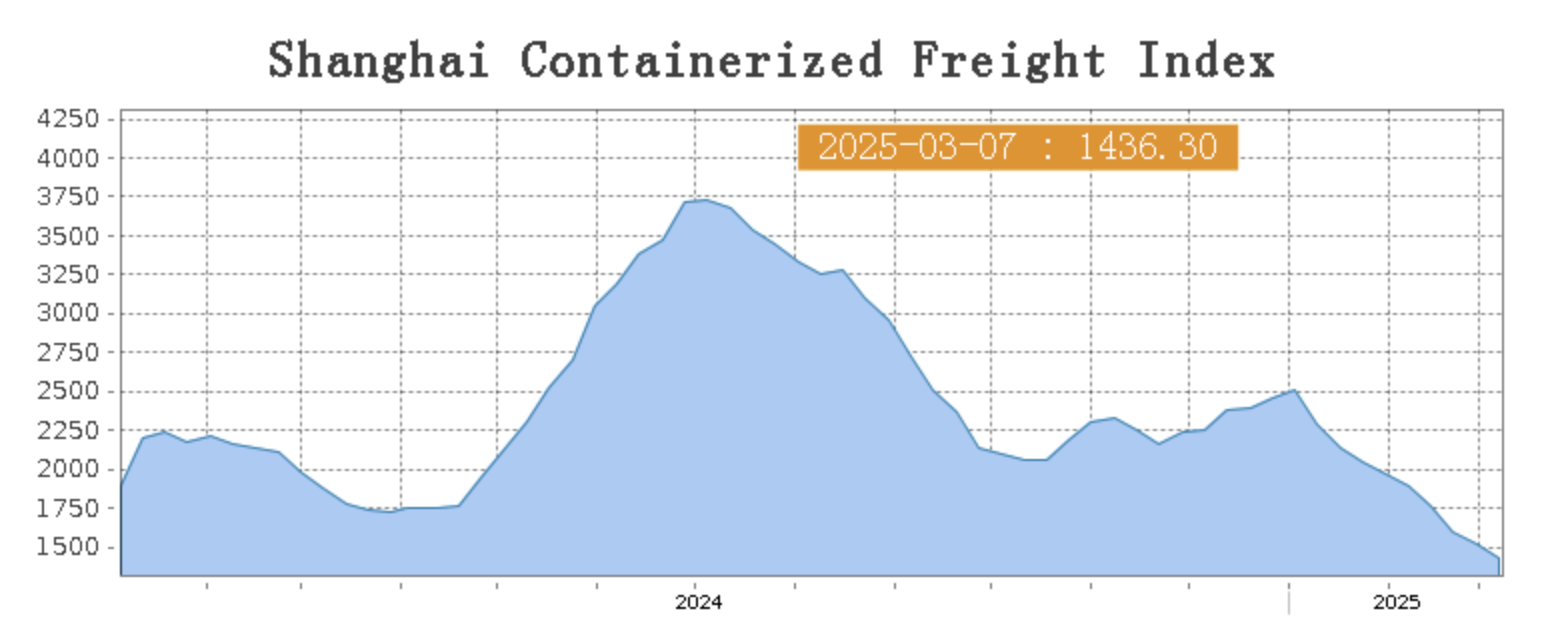

SEA FREIGHT || Demand Recovery is Slow, Freight Rates Continue to Decline.

Last week, China's export container transportation market is still in a slow recovery period. Although the overall market volume has increased, the recovery is less than expected, and ocean freight rates continue to decline, with the comprehensive index falling.

On March 7th, the Shanghai Containerized Freight Index (SCFI) fell 5.2% to 1436.29 points.

Europe/ Mediterranean:

According to recent PMI and other European economic data, the Eurozone's manufacturing sector has marginally improved. Last week, transportation demand has slowly recovered, but since the overall shipping capacity has returned to the pre-Spring Festival level, freight rates have continued to decline.

On March 7th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1582/TEU, which slid by 6.6%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2517/TEU, which dropped by 3%.

North America:

The United States has imposed additional tariffs on China, and trade conflicts have brought negative impacts to market transportation. Last week, market demand is generally recovering, shipping companies' load rates are generally average, and most have adopted price reduction strategies to attract order, and spot market booking prices have fallen.

On March 7th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2291/FEU and US$3329/FEU, reporting 7.7% and 5.1% down accordingly.

The Persian Gulf and the Red Sea:

On March 7th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf dipped 3.9% to $975/TEU.

Australia/ New Zealand:

On March 7th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New plunged 15.6% to $629/TEU.

South America:

On March 7th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 6.2% to $2422/TEU.