Stainless Insights in China from March 24th to March 30th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,105 | 0 | 0.00% |

| Foshan | 2,145 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,995 | -7 | -0.37% | |

| Foshan | 2,020 | 0 | 0.00% | ||

| 304/NO.1 | ESS | Wuxi | 1,930 | -3 | -0.15% |

| Foshan | 1,945 | -1 | -0.08% | ||

| 316L/2B | TISCO | Wuxi | 3,505 | 6 | 0.17% |

| Foshan | 3,570 | 0 | 0.00% | ||

| 316L/NO.1 | ESS | Wuxi | 3,375 | 0 | 0.00% |

| Foshan | 3,370 | 11 | 0.34% | ||

| 201J1/2B | Hongwang | Wuxi | 1,280 | 14 | 1.21% |

| Foshan | 1,290 | 15 | 1.32% | ||

| J5/2B | Hongwang | Wuxi | 1,185 | 18 | 1.72% |

| Foshan | 1,190 | 15 | 1.44% | ||

| 430/2B | TISCO | Wuxi | 1,160 | 4 | 0.40% |

| Foshan | 1,150 | 6 | 0.54% |

TREND || Rising Costs & Sustained Inventory Drawdown

Last week, stainless steel spot prices in the Wuxi market saw a slight rebound following futures movements, while costs edged up due to rising raw material prices. Improved market confidence and increased downstream purchases drove continued inventory depletion. As of Friday, the main stainless steel futures contract rose by US$26/ton week-over-week to US$2005/ton.

300 Series: Prices Rise, Inventories Dip

The 304 spot market prices stabilized with moderate gains. By Friday, the main base price for 304 cold-rolled sheets in Wuxi reached US$1955/ton, while hot-rolled prices stood at US$1935/ton, both up US$7/ton from the previous Friday. Futures fluctuated widely last week, supported by strong cost pressures. Spot prices firmed up, with chromium supply-side news briefly lifting futures mid-week, prompting some traders to raise quotes. However, terminal demand remains sluggish, and weekly transactions were muted.

200 Series: Prices Surge, High-Price Transactions Struggle

The 201 series maintained a strong upward trend. 201J2 cold-rolled sheets were quoted at US$1165/ton, while 201J1 cold-rolled and hot-rolled sheets traded at US$1255/ton and US$1225/ton, respectively. Prices for 201J1 and J2 cold- and hot-rolled products rose by US$7/ton on Monday, followed by another US$7/ton hike for 201J2 cold-rolled on Wednesday. On Thursday, 201J1 hot-rolled prices increased by US$7/ton, and all 201J1/J2 products rose another US$7/ton on Friday. Reduced market supply, linked to maintenance and production cuts at mills like Beigang Xincai and Baosteel Desheng, tightened availability. While transactions picked up post-price hikes, high-price deals faced resistance. Cold-rolled inventories saw minor accumulation, while hot-rolled stocks declined.

400 Series: Cost-Driven Price Support, Inventories Shrink

In Wuxi, 430/2B prices held steady at US$1155-US$1165/ton, and 430/NO.1 sheets remained flat at US$1075/ton, unchanged from the prior weekend. Rising costs and persistent inventory drawdowns strengthened price support for the 400 series.

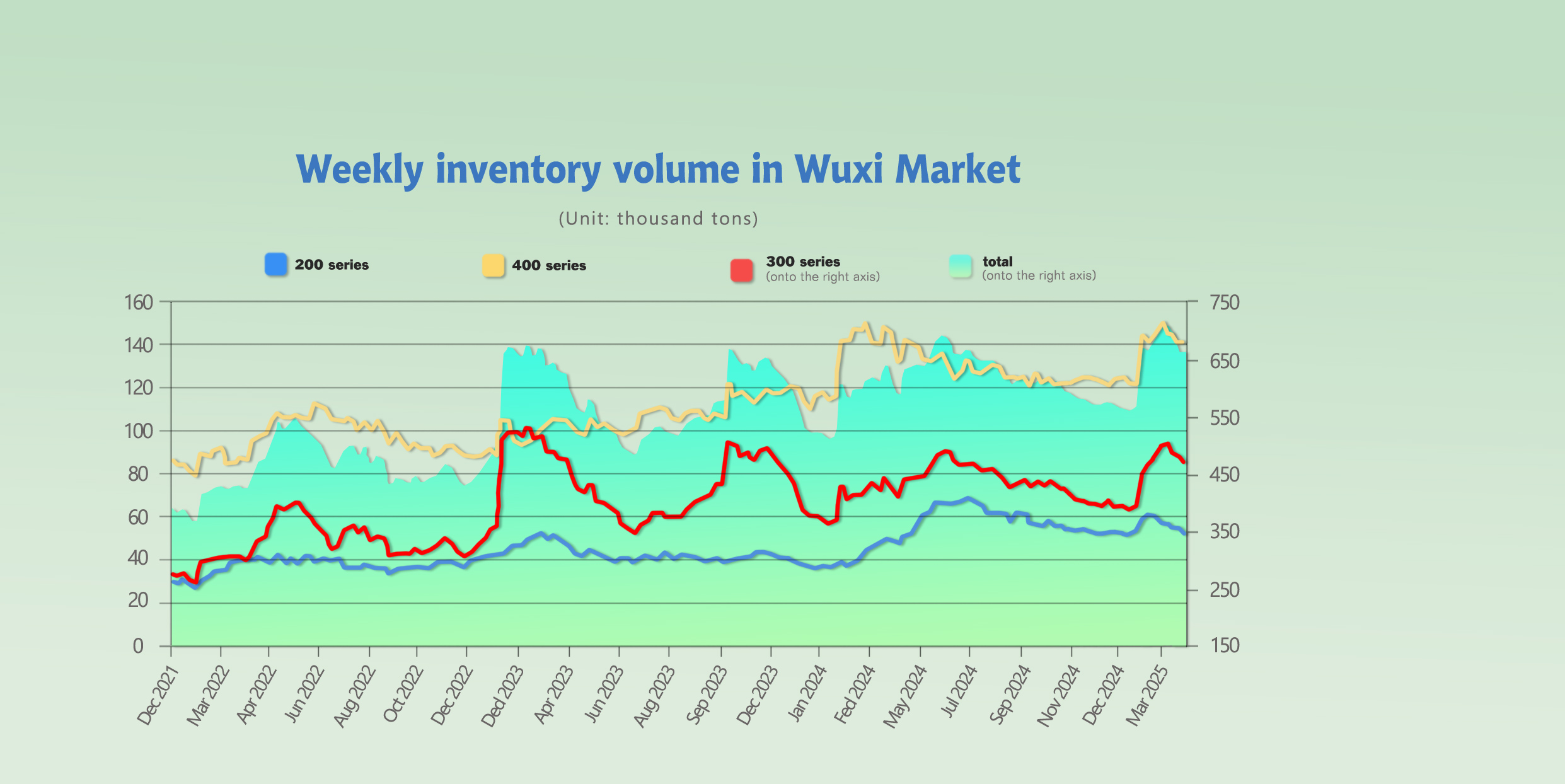

INVENTORY || Continued Drawdown, Weekly Decrease of 5,400 Tons

As of March 27th, total inventory in Wuxi sample warehouses decreased by 5,422 tons to 655,877. Breakdown:

200 Series: 179 tons down to 52,286 tons.

300 Series: 4,726 tons down to 464,570 tons.

400 Series: 517 tons up to 139,021 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Mar 20th | 52,465 | 469,296 | 139,538 | 661,299 |

| Mar 27th | 52,286 | 464,570 | 139,021 | 655,877 |

| Difference | -179 | -4,726 | -517 | -5,422 |

200 Series: Persistent Shortages, Rotating Maintenance Accelerates Inventory Reduction

Last week, from a supply perspective, rotating maintenance at Beigang New Material and production cuts at Baosteel Desheng due to equipment failures reduced market arrivals. Shortages of thin-gauge materials persist. The 201J2 price is expected to remain firm in the short term, with inventories likely to see minor accumulation next week. Key focus areas: mill output and market transactions.

300 Series: Futures-Spot Price Tug-of-War, Concentrated Deliveries Drive Drawdown

Supply-side production rebounded, ensuring ample market availability. Demand remains rigid, with weak speculative interest. Prices are expected to stay range-bound with upward bias in the short term, supported by futures. Inventories may continue declining next week. Key focus: mill output and transaction volumes.

400 Series: Cost Support Strengthens, Inventories Decline

TISCO’s cold- and hot-rolled inventories saw significant reductions, while JISCO’s cold-rolled stocks also declined. Inventory drawdowns continued but slowed compared to last week.

430 cold-rolled prices stabilized last week, supported by steady downstream demand, ongoing inventory reductions, and firm cost pressures. Monitor the impact of April’s high-chromium steel tender prices on 430 pricing.

RAW MATERIALS || Ore Costs Continue Rising

Nickel: Cost Support Drives Ferronickel Price Strength

High-grade ferronickel prices strengthened last week, with Thursday’s ex-works quotes at US$142.7/nickel point, up 0.7/nickel point from previous Thursday.

An Indonesian ferronickel plant sold over 10,000 tons at US$144.1/nickel point (CIF, tax-inclusive). Tight pyrometallurgical nickel ore supply in Indonesia during March, coupled with ongoing government discussions to raise nickel ore and ferronickel taxes, could push nickel ore prices up by $3–4/wet ton if implemented. Domestic steel mills maintain high production levels, boosting raw material demand. Ferronickel prices are expected to remain firm.

Chrome: Major Producers Signal Output Cuts

On March 27, another large high-carbon ferrochrome producer in Inner Mongolia announced a 30% production cut for April due to power supply disruptions from thermal plant maintenance, suspending spot chromium ore purchases.

Downstream buyers remain cautious toward high-priced ore, while most ferrochrome plants operate at losses, dampening production enthusiasm. Multiple Inner Mongolia-based producers have signaled output reductions. In southern China, high costs have slowed post-holiday restarts. Chromium ore prices are expected to face upward resistance in the near term.

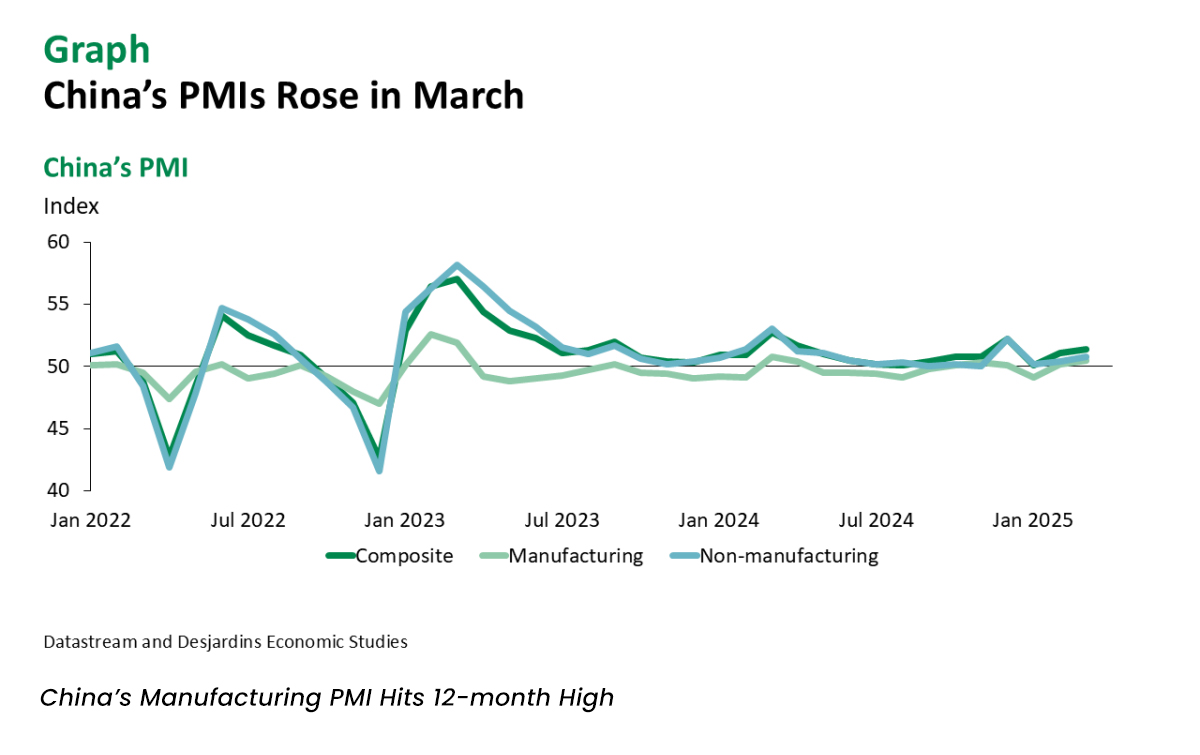

MACRO || China’s March Manufacturing PMI Rises to 50.5%, Tariff Impact Yet to Materialize

China’s manufacturing Purchasing Managers’ Index (PMI) climbed to 50.5% in March, up 0.3 percentage points from the previous month, marking a continued recovery in manufacturing activity.

This marks the highest manufacturing PMI in 12 months. The lack of visible tariff impacts on the PMI could stem from domestic supply chains having shifted to Southeast Asia over the past seven years, diluting tariff-related pressures.

The new export orders index rose by 0.4 percentage points to 49%, though it has remained below the expansion-contraction threshold for 11 consecutive months. A gradual improvement trend is emerging.

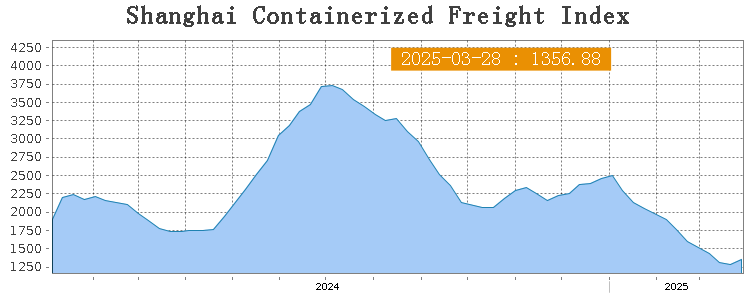

SEA FREIGHT || Freight Market Stabilizes, Rates Rebound on Most Routes

After consecutive adjustments, China’s export container shipping market showed signs of stabilization last week. Shipping demand held steady, with freight rates rebounding on most routes, lifting the composite index.

Last week, China’s export container shipping market continued its downward adjustment, with weaker transportation demand and declining freight rates across most routes, leading to a drop in the composite index. On March 28th, the Shanghai Containerized Freight Index (SCFI) rose 5% to 1356.88 points.

Europe/ Mediterranean:

Europe faces multiple risks, including geopolitical tensions and escalating trade conflicts, clouding its economic outlook. Last week, shipping demand remained stable, and rates steadied after prolonged declines.

On March 28th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was USUS$1318/TEU, which increased by 0.9%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was USUS$2076/TEU, which dropped by 5.4%.

North America:

The U.S. announced plans to impose additional tariffs on imported vehicles early next month, raising risks of intensified trade conflicts. North American routes are likely to face heightened volatility. With the contract renewal season approaching, shipping demand showed no significant growth, but freight rates edged up.

On March 28th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were USUS$2177/FEU and USUS$3194/FEU, reporting 16.3% and 11.4% surge accordingly.

The Persian Gulf and the Red Sea:

On March 28th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf rose 12.2% to US$1188/TEU.

Australia&New Zealand:

On March 28th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand rose 9.7% to US$828/TEU.

South America:

On March 28th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 0.7% to US$1669/TEU.

Japan:

On March 28th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to Japan major ports was US$967.28/TEU.