Stainless Insights in China from March 10th to March 16th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,085 | 32 | 1.66% |

| Foshan | 2,125 | 32 | 1.63% | ||

| Hongwang | Wuxi | 1,995 | 39 | 2.13% | |

| Foshan | 2,010 | 29 | 1.58% | ||

| 304/NO.1 | ESS | Wuxi | 1,930 | 38 | 2.13% |

| Foshan | 1,935 | 28 | 1.56% | ||

| 316L/2B | TISCO | Wuxi | 3,515 | 22 | 0.67% |

| Foshan | 3,590 | 14 | 0.41% | ||

| 316L/NO.1 | ESS | Wuxi | 3,390 | 21 | 0.65% |

| Foshan | 3,375 | 6 | 0.17% | ||

| 201J1/2B | Hongwang | Wuxi | 1,255 | 13 | 1.12% |

| Foshan | 1,260 | 15 | 1.36% | ||

| J5/2B | Hongwang | Wuxi | 1,155 | 14 | 1.36% |

| Foshan | 1,160 | 15 | 1.49% | ||

| 430/2B | TISCO | Wuxi | 1,155 | 0 | 0.00% |

| Foshan | 1,145 | 4 | 0.41% |

TREND || Stainless Steel Prices Keep Rising, with Downstream Market Mainly in Wait-and-See Mode

Last week, the spot prices of stainless steel in the Wuxi market continued to rise following the market trend, reaching a maximum of US$2,035/MT, with a high degree of speculation. On the cost side, as raw material prices increased, the cost logic provided support for price increases. The arrival of goods in the market decreased, procurement improved, and inventory was reduced. As of Friday, the price of the main stainless steel contract rose to a maximum of US$2,035/MT, an increase of US$32/MT compared to last week, and closed at US$2,025/MT.

300 Series: Consecutive Price Increases, First Inventory Decline Boosts Consumption Sentiment

The spot market prices of 304 stainless steel continued to rise last week. As of last Friday, the mainstream base price of 304 private cold-rolled four-foot steel in the Wuxi area was reported at US$1,970/MT, an increase of US$42/MT compared to the quotation previous week; the price of private hot-rolled steel was reported at US$1,945 /MT, an increase of US$28/MT compared to last Friday's price. The futures market moved steadily upward, the nickel price continued to increase, and with strong cost support and the release of peak-season demand, the market mostly maintained a price-stabilizing attitude. The spot price rose continuously during the week. The market sentiment improved in the later period, and terminal purchases increased. The inventory changed from an increase to a decrease during the week.

200 Series: Active Market Transactions

Last week, the price of 201 stainless steel maintained a strong and stable operation trend. The 201J2 cold-rolled steel was reported at US$1,135/MT gross basis; the 201J1 cold-rolled steel was reported at US$1,230/MT gross basis, and the 201J1 hot-rolled steel was quoted at US$1,195 /MT.

On Tuesday, the prices of 201J1 and 201J2 cold-rolled steels were increased by US$7/MT. On Wednesday, the price of 201J1 hot-rolled steel was increased by US$7/MT. On last Friday, the prices of 201J1 and 201J2 cold-rolled steels were increased by US$7/MT again. Downstream customers actively purchased, the market transaction atmosphere was active, shortages of some specifications occurred, and the cold-rolled and hot-rolled inventories both decreased slightly during the week.

400 Series: Stable Raw Material Prices, Slight Increase in Finished Product Prices

Last week, the quotation of 430 cold-rolled steel in the Wuxi market continued to be stable at US$1060/MT; the mainstream quotation of 430/NO.1 remained at US$1,075/MT, and the transactions were acceptable. During last week, the change in the spot inventory of the 400 series market was small. The arrival of goods from steel mills was scarce, and price support still existed.

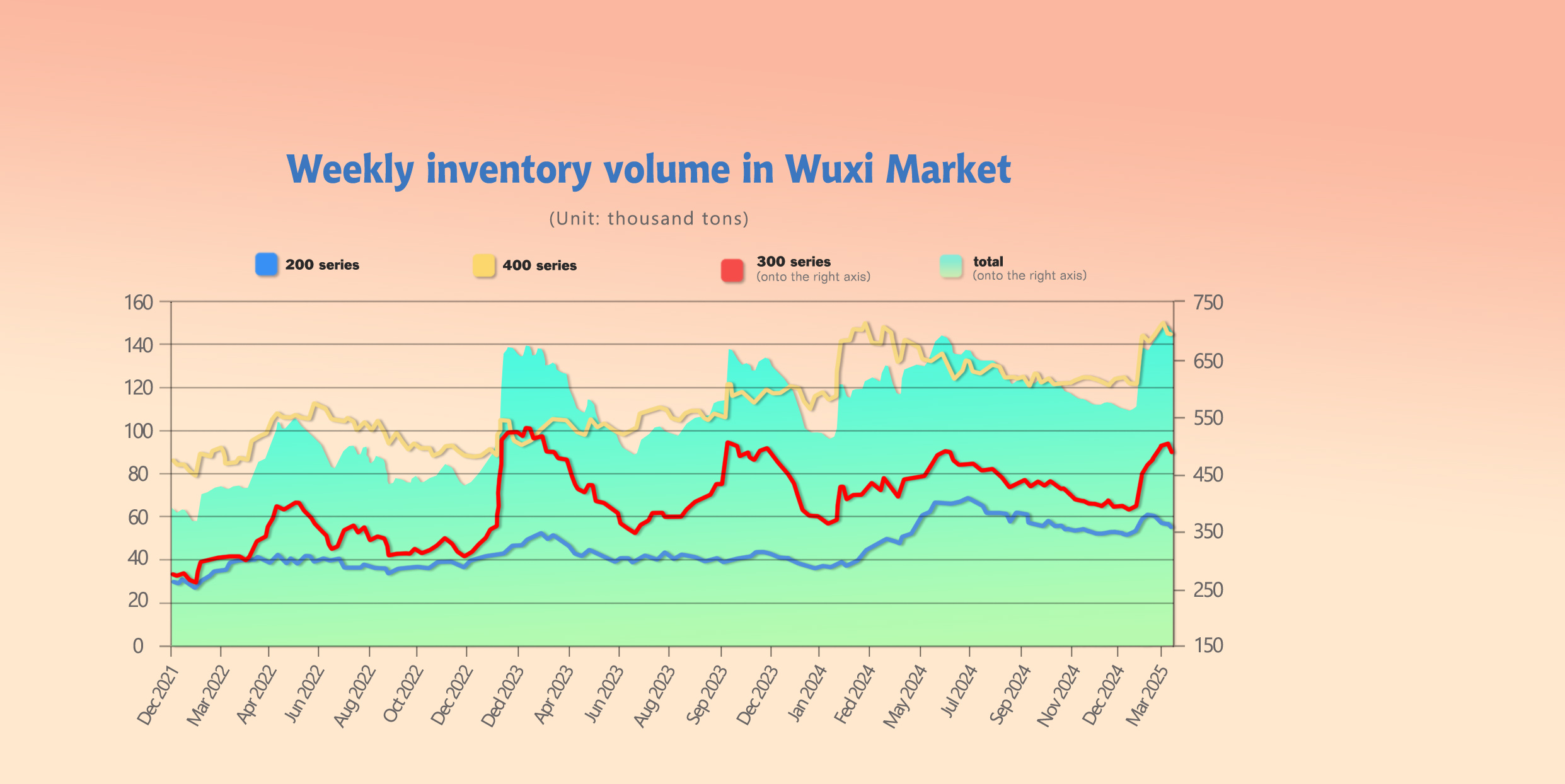

INVENTORY || Inventory Declines Again, Positive Expectations for Stainless Steel

As of March 13th, total inventory in Wuxi sample warehouses decreased by 15,268 tons to 685,976 tons. Breakdown:

200 Series: 1,223 tons down to 55,021 tons.

300 Series: 14,074 tons down to 485,953 tons.

400 Series: 29 tons up to 145,002 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Mar 6th | 56,244 | 500,027 | 144,973 | 701,244 |

| Mar 13th | 55,021 | 485,953 | 145,002 | 685,976 |

| Difference | -1,223 | -14,074 | 29 | -15,268 |

200 Series: Continued Shortages, Continuous Inventory Reduction

Last week, the price of 201 cold-rolled steel continued to increase, the procurement at the consumer end was relatively active, shortages of some specifications occurred, and there were more shortages of thin materials, resulting in a slight reduction in inventory. In the short term, the price of 201J2 may maintain a strong and stable operation trend. It is expected that the inventory may continue to decline next week.

300 Series: Price Increase, Inventory Changes from Increase to Decrease

During last week, the spot and futures prices rose in resonance. Low-price resources in the market were reluctant to sell. With the enhancement of expectations for domestic macro policies, market confidence improved, the willingness of downstream customers to purchase increased, and transactions were relatively good in some periods, resulting in a slight reduction in inventory.

The shortage of some hot-rolled specifications has not been resolved yet. The willingness of terminal customers to stock up and purchase has increased, and the hot-rolled inventory has decreased significantly. In the short term, the price of the 300 series may follow the market trend and maintain an upward trend. The market purchase willingness has increased. It is expected that the inventory may continue to decline next week.

400 Series: Stable Inventory Operation

Last week, the spot inventory of JISCO cold-rolled steel decreased significantly, and the spot inventories of TISCO's cold-rolled and hot-rolled steels both decreased slightly. The overall inventory fluctuated slightly compared to last week.

In March, the mainstream steel procurement price of high-chromium was flat, lower than the market's expected price increase. The expectation of strengthened cost support for stainless steel failed, and downstream customers remained in a wait-and-see state. It is expected that the market spot inventory will maintain a slight downward trend next week.

RAW MATERIAL || Good Transactions in the Ferronickel Market, Continuous Price Increase

LME Closing Summary

The price of LME nickel increased by US$85 compared to the previous trading day and closed at US$16,550. The inventory increased by 606 tons to 200,580 tons. The opening price of LME nickel was US$16,275. During the session, it reached a maximum of US$16,485, a minimum of US$16,440, and finally closed at US$16,780, an increase of 0.52% compared to the previous trading day. Concerns about US tariffs and other factors suppressed buying, and most metals closed lower.

The ex-factory price of high-nickel ferronickel continued to rise. As of last Friday, it was reported at US$140/nickel point, an increase of US$2/nickel point compared to last Friday.

On March 10, a ferronickel plant in Indonesia sold nearly 10,000 tons of high-nickel ferronickel at US$139/nickel point (DDU including tax), with a delivery date in April.

On March 13, a ferronickel plant in Indonesia sold over 10,000 tons of high-nickel ferronickel at US$141/nickel point (DDU including tax), with a delivery date in mid-to-late April.

On March 13, a ferronickel plant in Indonesia sold tens of thousands of tons of high-nickel ferronickel at US$142/nickel point (DDU including tax), with a delivery date in late April.

The transaction price of ferronickel exceeded US$140/MT, which was affected by many factors. The production of the third phase of a ferronickel plant in Indonesia has not resumed yet, affecting the return of domestic ferronickel. The local nickel ore supply is limited, and the relevant regulations of the Indonesian Ministry of Energy and Mineral Resources on changing the mineral benchmark price have also been superimposed. Domestically, the ore price is firm. Although the price of ferronickel has increased, domestic factories are still operating at a loss. In the short term, the price of ferronickel will operate in a stable and slightly strong manner.

SUMMARY || Short-Term Stable Prices for 300 Series and 200 Series

Last week, the price of stainless steel operated in a strong manner. On the market demand side, procurement was mainly for rigid needs. Steel mills continued to deliver goods, the social inventory remained high, the number of warehouse receipts increased significantly, and the spot resources were sufficient. The market divergence gradually increased, and there may be significant fluctuations in the later market. Policies have boosted market prices. Pay attention to the release of vitality on the demand side during the peak season in the later market, as well as the production scheduling of steel mills and the reduction of social inventory. It is expected that the price of stainless steel will fluctuate widely in the later market.

300 Series: The strong increase in costs and the warming of future market expectations have provided strong cost support for stainless steel. The profits of steel mills are gradually being repaired, and they have a strong attitude of maintaining prices. The spot and futures prices have risen in resonance. The supply of steel mills continued to recover in March. With the positive impact of policies driving further release of downstream demand, there is still an expectation of inventory reduction. It is expected that the spot price of stainless steel will operate in a strong manner in the short term.

200 Series: Recently, the price of raw material copper has maintained an upward trend, which provides strong cost support for 201 stainless steel. The output of 200 series crude steel by steel mills increased in March, and downstream demand improved. Macro policies have driven market sentiment, and with the continuous strengthening of the market trend, the price of 201J2 cold-rolled steel may operate in a strong and stable manner in the short term.

400 Series: The price of 430 stainless steel mainly remained stable. There was no significant breakthrough in downstream demand, the reduction of spot inventory slowed down, and the support from the high-chromium raw material side was less than expected. In the short term, the price of 430 stainless steel will mainly remain stable. Pay attention to the impact of the arrival of resources at steel mills and fluctuations in raw material prices on the price of 430 stainless steel in the near future.

At present, affected by the continuous increase of tariffs by the United States, the transportation market as a whole has weakened, transportation demand has remained at a low level, and the basic supply and demand situation lacks further support. The booking price in the spot market continues to decline significantly.

MARCO || "Super Central Bank Week" in Focus: Interest Rate Decisions and Market Expectations

This week, the global financial markets will witness the highly anticipated "Super Central Bank Week". According to the schedule, multiple central banks, including the Federal Reserve, the Bank of Japan, the Bank of England, the Swiss National Bank, and the Sveriges Riksbank, will announce their interest rate decisions.

The Federal Reserve will announce its interest rate decision in the early morning of March 20th, Beijing time. Fed Chair Jerome Powell will hold a monetary policy press conference shortly thereafter. Judging from market expectations, it is a foregone conclusion that the Federal Reserve will remain "on hold" at this meeting. The CME Group's "FedWatch" tool shows that the probability of the Federal Reserve maintaining the target range for the federal funds rate at 4.25% to 4.50% at this week's meeting is nearly 100%.

Fed officials generally expect two rate cuts this year. However, the current market pricing indicates a relatively high probability of three rate cuts by the Fed this year, and it is expected to resume rate cuts as early as June.

Behind this expectation lies the market's concern about the prospect of a slowdown in US economic growth.

Looking globally, the uncertainty brought about by US tariff policies is making the monetary policy paths of various countries more complex, and "caution" has become the main tone of global central banks' monetary policy adjustments.

In addition to the Federal Reserve, this week, multiple central banks such as the Bank of Japan, the Bank of England, the Bank of Indonesia, the Swiss National Bank, and the Sveriges Riksbank will also announce their interest rate decisions. Among them, the Bank of England is expected to remain "on hold" and adopt a wait - and - see attitude this week, and is highly likely to continue its policy tone of "gradual adjustment". Data released by the Office for National Statistics of the UK on March 14th showed that the UK's GDP declined by 0.1% month - on - month in January.

The Bank of Japan is also expected to keep interest rates unchanged this week. The meeting statement and press conference are expected to reveal the Bank of Japan's judgment on the prospects of interest rate hikes.

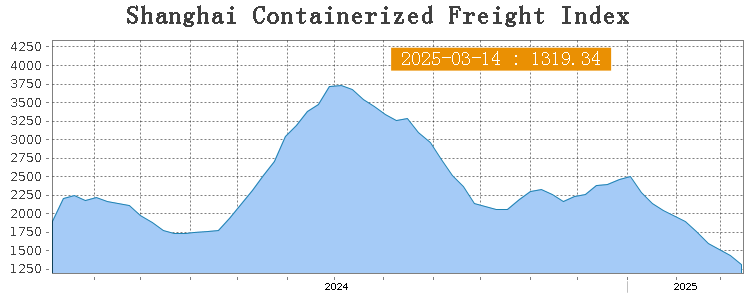

SEA FREIGHT || Weak Performance in the Transportation Market, Freight Rates of Most Routes Decline

Last week, the Chinese export container transportation market continued to show a relatively weak performance. The transportation demand lacked the momentum for further growth, and the freight rates of most route markets continued to decline, dragging down the composite index.

On March 14th, the Shanghai Containerized Freight Index (SCFI) fell 8.1% to 1319.34 points.

Europe/ Mediterranean:

On March 14th, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was USUS$1342/TEU, which slid by 15.2%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was USUS$2295/TEU, which dropped by 8.8%

North America:

The United States has imposed additional tariffs on China, and trade conflicts have brought negative impacts to market transportation. Last week, market demand is generally recovering, shipping companies' load rates are generally average, and most have adopted price reduction strategies to attract order, and spot market booking prices have fallen.

On March 14th, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were USUS$1965/FEU and USUS$2977/FEU, reporting 14.2% and 10.6% plunge accordingly.

The Persian Gulf and the Red Sea:

On March 14th, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf rose 0.1% to US$976/TEU.

Australia&New Zealand:

On March 14th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New redounded 16.9% to US$735/TEU.

South America:

On March 14th, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 19.7% to US$1945/TEU.

The Current Plunge in International Freight Rates: Sea Freight Rates Are About to Bottom Out and Rebound

The Shanghai Containerized Freight Index (SCFI) plummeted from 2,505 points at the beginning of January to 1,436 points on March 7, a decrease of more than 42%. The freight rates of the West Coast and East Coast routes to the United States were halved, and the South American route even declined by 55%. There are already signs of the market bottoming out.

1. Shipping Companies' Suspension of Sailings and Reduction of Services to Alleviate Supply-Demand Contradictions and "Self-Saving" Price Increases

Maersk has announced a price increase for European routes in April (the price for a 40-foot container will increase to US$4,000), sending a "stop-falling" signal.

Seasonal Demand Recovery

Historical data shows that the global sea freight volume in the second quarter usually increases by 15%-20% month-on-month. Coupled with the accelerated resumption of work in the manufacturing industry, the freight rate is expected to enter a bottoming-out period.

Extreme Capacity Reduction

In the next five weeks, 47 sailings will be cancelled on major global routes (accounting for 6% of the total planned sailings), and the capacity of the trans-Pacific eastbound route will be reduced by 43%. The supply-demand contradiction is expected to be alleviated.

Christian, the CEO of German company AXS-Alphaliner, said that if shipping companies maintain the current suspension of sailings, the global capacity in April will be 81,000 TEUs less than that in February, and the supply-demand gap will narrow to less than 3%, significantly reducing the downward pressure on freight rates.

2. US Tariff Policies Spawn a "Rush Shipment Boom"

On March 4, the United States imposed a second round of 10% tariffs on Chinese goods (with a maximum comprehensive tax rate of 45%). Foreign trade enterprises in Zhejiang, Guangdong and other places accelerated the transfer of production capacity to Southeast Asia, but in the short term, they still need to transport raw materials and export finished products by sea.

If the United States further increases auto tariffs on April 2, it may trigger a new round of rush shipment demand, and the freight rate on the US routes may experience a retaliatory rebound.

Shipping Company Strategic Adjustment: From "Trading Price for Volume" to "Protecting Price and Controlling Space"

Capacity Optimization

Mediterranean Shipping Company (MSC) has cancelled the trans-Pacific Mustang route and transferred 24,000 TEU ultra-large ships to high-profit routes such as West Africa, reducing the deployment of inefficient capacity.

Dynamic Pricing

Shipping companies are piloting a floating freight rate mechanism. The spot price of the European route is already lower than the long-term agreement price, forcing enterprises to renegotiate contracts and leaving room for price increases.

3. Freight Rate Trend Forecast for the Next Three Months

Short Term (Late March): Freight Rates Continue to Bottom Out, but the Decline Narrow

The freight rate of the West Coast route to the United States may fall below the cost line of US$2,000/FEU. Shipping companies may attract shippers to lock in positions through "ultra-low special offers" to pave the way for price increases in April.

Medium Term (April - May): Seasonal Demand and Policy Stimulus Resonate

During the traditional peak season in the second quarter, coupled with rush shipments due to tariffs, the freight rate of the West Coast route to the United States may rebound to US$2,500/FEU, and the European route may recover to US$3,000/FEU.

Long Term (After June): Structural Supply-Demand Improvement

In 2025, the global delivery volume of new ships will decrease to 2.4 million TEUs (a year-on-year decrease of 18%). Coupled with the growth of regional trade under the RCEP, the pressure of overcapacity will be alleviated, and the freight rate will enter a stable upward channel.