Stainless Insights in China from February 17th to February 21st.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,035 | 0 | 0.00% |

| Foshan | 2,075 | 0 | 0.00% | ||

| Hongwang | Wuxi | 1,925 | -6 | -0.31% | |

| Foshan | 1,945 | -4 | -0.23% | ||

| 304/NO.1 | ESS | Wuxi | 1,855 | -4 | -0.24% |

| Foshan | 1,875 | -4 | -0.24% | ||

| 316L/2B | TISCO | Wuxi | 3,475 | 0 | 0.00% |

| Foshan | 3,530 | -8 | -0.25% | ||

| 316L/NO.1 | ESS | Wuxi | 3,345 | -21 | -0.65% |

| Foshan | 3,335 | 0 | 0.00% | ||

| 201J1/2B | Hongwang | Wuxi | 1,225 | -3 | 0.88% |

| Foshan | 1,215 | 0 | 0.00% | ||

| J5/2B | Hongwang | Wuxi | 1,125 | -3 | -0.27% |

| Foshan | 1,120 | 0 | 0.00% | ||

| 430/2B | TISCO | Wuxi | 1,150 | 6 | 0.54% |

| Foshan | 1,135 | -7 | -0.68% |

TREND || Significant Inventory Reduction Supports Prices.

Stainless steel futures prices fluctuated strongly last week, bolstered by a sharp reduction in warehouse receipts on Thursday. Trading activity remained similar to last week, while open interest continued to rise. The main stainless steel futures contract closed at US$1960/MT, up 1.07% week-on-week, with a weekly high of US$1980/MT. Spot prices rose by US$7-21/MT. Post-holiday demand recovery remains gradual, with factories resuming operations and downstream buyers prioritizing rigid needs. Trading activity improved compared to last week.

300 Series: Prices Rise Amid Inventory Accumulation.

304 spot prices stabilized with a slight upward trend. As of Friday, the mainstream base price for 304 cold-rolled stainless steel (4ft, private mills) in Wuxi rose US$14/MT to US$1895/MT, while hot-rolled prices increased US$5/MT to US$1865/MT. Futures gains and speculative trading drove prices higher. Mills like Tsingshan raised offers, but downstream buyers hesitated to accept high prices. Increased arrivals and inventory growth capped price rebounds.

200 Series: Maintenance News Boosts Sentiment.

201 series prices firmed up. 201J2 cold-rolled prices settled at US$1100/MT (gross basis), while 201J1 cold-rolled and hot-rolled prices held at US$1200/MT and US$1180/MT, respectively.

On Friday, 201J2 cold-rolled prices rose US$7/MT. Early-week futures weakness prompted traders to offer discounts, but sentiment improved later in the week, lifting transaction activity.

400 Series: Stable Costs Support Mild Price Gains.

430 cold-rolled prices rose US$7/MT to US$1150-US$1155/MT, while 430/NO.1 hot-rolled prices remained flat at US$1075/MT.

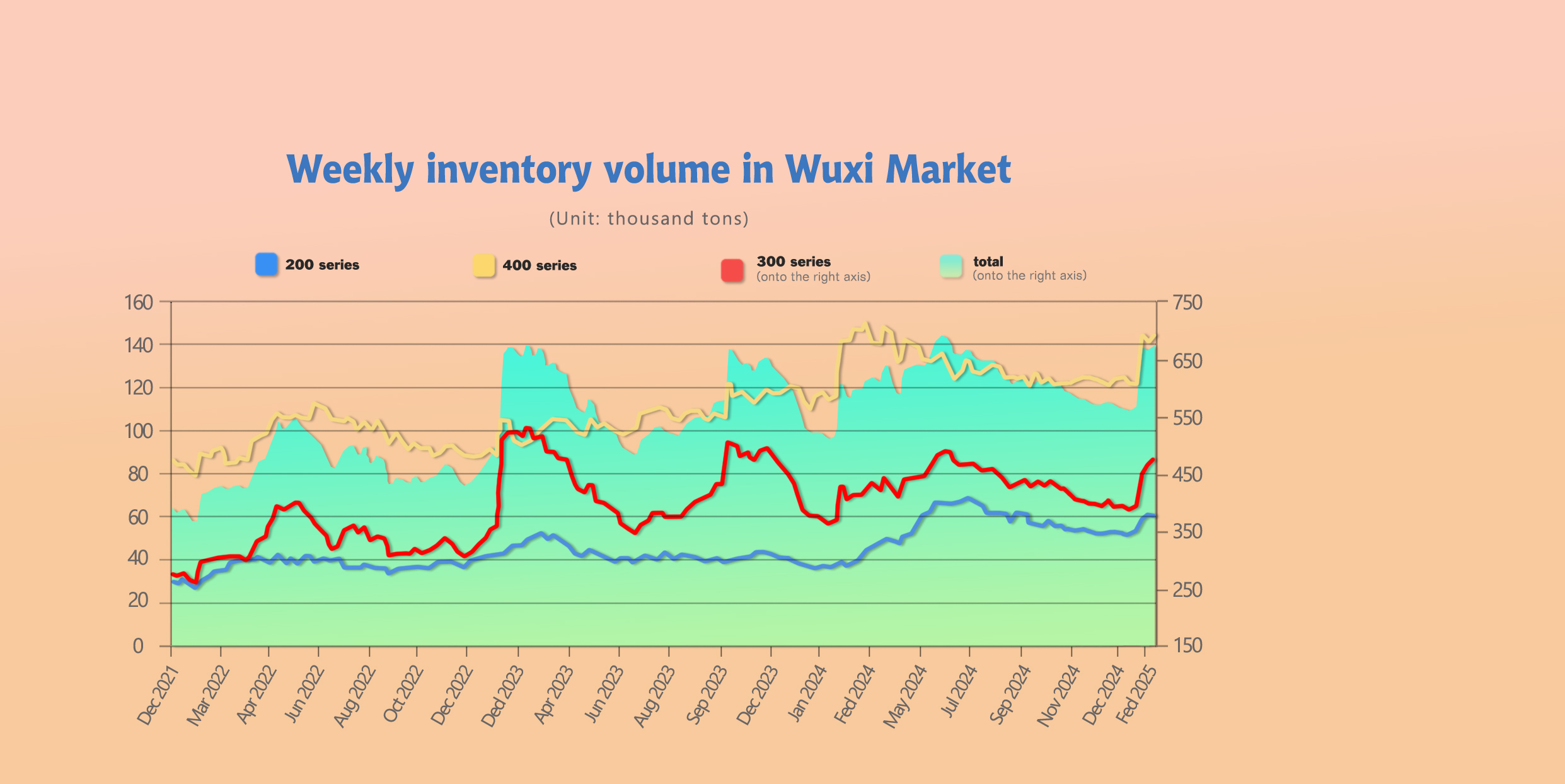

INVENTORY || Beigang New Materials’ Maintenance to Impact 200 Series Output.

On February 17th, Beigang New Materials announced a 3–6 month maintenance plan starting in March, expected to reduce 200 series output by approximately 300,000 tons.

As of February 20th, total inventory in Wuxi sample warehouses increased by 14,100 tons to 681,100 tons. Breakdown:

200 Series: 1,600 tons down to 60,000 tons.

300 Series: 10,500 tons up to 476,400 tons.

400 Series: 5,100 tons up to 144,700 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Feb 13th | 61,558 | 465,846 | 139,634 | 667,038 |

| Feb 20th | 59,995 | 476,383 | 144,720 | 681,098 |

| Difference | -1,563 | 10,537 | 5,086 | 14,060 |

300 Series: Mill Price Caps Slow Inventory Reduction.

Tsingshan’s price hikes limited trading, with downstream buyers staying cautious. Inventory accumulation persisted despite promotional discounts.

200 Series: Maintenance Plans Drive Inventory Decline.

200 series inventory dropped by 1,600 tons (cold-rolled dropped 1,400 tons; hot-rolled down 200 tons) to 60,000 tons. Beigang’s maintenance plan boosted market confidence, lifting transaction volumes.

400 Series: Arrivals Push Inventory Higher.

400 series inventory increased by 5,100 tons (cold-rolled +4,900 tons; hot-rolled +200 tons) to 144,700 tons. Significant arrivals of JISCO cold-rolled resources intensified supply pressure.

RAW MATERIAL || Indonesia Cuts Nickel Quotas.

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has decided to reduce nickel mining quotas in its 2025 Work Plan and Budget (RKAB) to balance supply and demand and stabilize global nickel prices.

Minister Bahlil Lahadalia emphasized that the quota adjustment aims to maintain price stability while ensuring domestic industrial needs and downstream growth. He stated, “We must maintain a balance. The quota should not be so high above industry demand that nickel prices become cheap, We are ensuring prices remain favorable yet sufficient for industry.”

He added, “This initiative has received positive responses from various stakeholders, with some circles viewing it as the right move to prevent price volatility from harming industrial sectors.”

This policy is part of broader efforts to optimize resource management and sustain Indonesia’s competitiveness in the global nickel market.

SUMMARY || Cost Support Underpins Stainless Prices.

Stainless steel spot prices fluctuated strongly last week. Stable raw material costs and thinning mill margins coincided with rising inventories and reduced warehouse receipts. Market focus remains on inventory trends, mill production adjustments, and raw material prices.

300 Series: Low mill output eases supply pressure, but weak demand sustains inventory challenges. Rising costs may curb future production. Prices expected to follow futures with mild strength.

200 Series: Beigang’s maintenance plan and firm copper/manganese costs bolster sentiment. Gradual demand recovery supports stable 201J2 prices.

400 Series: Stable production costs and moderate demand keep 430 prices steady. Inventory drawdowns remain slow.

MACRO || Chinese Stainless Prices Hit Six-Year Low.

As of February 21, 2025, prices for 304 cold/hot-rolled, 201 cold/hot-rolled, and 430 cold/hot-rolled in Wuxi are at their lowest levels in six years. In 2024, prices trended downward due to oversupply and weak raw material costs, with only a brief uptick in October.

In 2025, price volatility has narrowed. Post-holiday futures gains driven by raw materials failed to lift spot prices significantly due to weak demand. However, factors like maintenance plans and firm raw material costs are gradually supporting a price recovery.

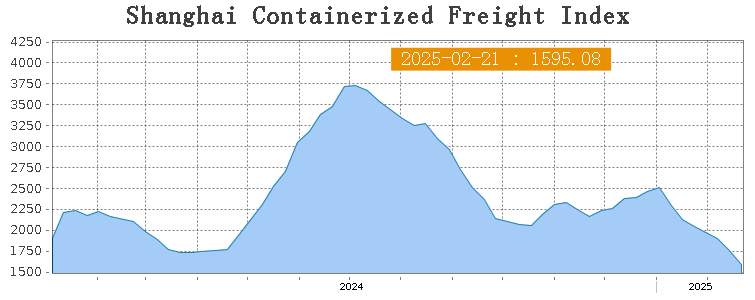

SEA FREIGHT || Freight Rates Continue Downward Trend.

Last week, China's export container shipping market showed a slightly weak performance. The market as a whole presented a slow recovery trend after the holidays. Freight rates on all ocean routes continued to decline, dragging down the comprehensive index.

On February 21st, the Shanghai Containerized Freight Index (SCFI) fell 9.3% to 1595.08 points.

Europe/ Mediterranean:

According to data released by the European Statistical Office, the initial value of the Eurozone consumer confidence index for February was -13.6. Although it was slightly better than the previous value, it continued to be in the negative range, indicating that consumer confidence is still in a pessimistic state. Recently, the situation of the Russia-Ukraine conflict has been volatile, leading to an increase in geopolitical risks in Europe. The future economic outlook for Europe faces many risks. Last week, transportation demand lacked further growth momentum, and the supply and demand fundamentals lacked further support. Market freight rates continued to decline.

On February 21st, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was US$1578/TEU, which fell by 1.9%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was US$2624/TEU, which dropped by 6.8%.

North America:

According to data released by the US Department of Commerce, US retail sales in January fell by -0.9% month-on-month, which was significantly lower than market expectations and the largest month-on-month decline since March 2023. The substantial slowdown in consumption will have an adverse impact on future US economic growth. Currently, US President Trump is continuing to expand measures to increase the scope of future tariffs, and trade conflicts face the risk of continuous expansion, which will have a greater impact on the North American route.

On February 21st, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were US$2907/FEU and US$3954/FEU, reporting 18% and 18.1% down accordingly.

The Persian Gulf and the Red Sea:

On February 21st, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf dipped 3.7% to $1102/TEU.

Australia/ New Zealand:

On February 21st, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New plunged 14.6% to $826/TEU.

South America:

On 21st February, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 12.3% to $2947/TEU.