Stainless Insights in China from January 6th to January 10th.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 1,995 | -19 | -1.00% |

| Foshan | 2,035 | -19 | -0.98% | ||

| Hongwang | Wuxi | 1,885 | -15 | -0.83% | |

| Foshan | 1,920 | -12 | -0.67% | ||

| 304/NO.1 | ESS | Wuxi | 1,830 | -4 | -0.22% |

| Foshan | 1,845 | -8 | -0.46% | ||

| 316L/2B | TISCO | Wuxi | 3,385 | -11 | -0.34% |

| Foshan | 3,450 | -17 | -0.50% | ||

| 316L/NO.1 | ESS | Wuxi | 3,240 | 11 | 0.36% |

| Foshan | 3,250 | -1 | -0.04% | ||

| 201J1/2B | Hongwang | Wuxi | 1,200 | -11 | -1.01% |

| Foshan | 1,185 | -4 | -0.38% | ||

| J5/2B | Hongwang | Wuxi | 1,085 | 0 | 0.00% |

| Foshan | 1,085 | -4 | -0.42% | ||

| 430/2B | TISCO | Wuxi | 1,125 | 0 | 0.00% |

| Foshan | 1,125 | 0 | 0.00% |

TREND || Strong Rebound in Stainless Steel Futures, Price at High Levels Shows Market Divergence.

Stainless steel prices increased this week. By midweek, the market transaction atmosphere warmed up, with low-priced goods performing well. Demand remains driven by just-in-time purchasing, and social inventories have decreased. Going forward, attention will focus on steel plant production schedules and demand performance, as well as the impact of domestic macroeconomic policies and their implementation. The market is expected to see fluctuating stainless steel prices in the future. This week, the main stainless steel futures contract closed at US$1,930/ton, up 3.22% from the previous week, with a peak price of US$1,945/ton.

300 Series: Price Rebounds from the Bottom, Increased Purchases to Reduce Inventory.

This week, the 304 spot market prices rebounded from the bottom. As of Friday, in Wuxi, the mainstream base price for 304 cold-rolled four-foot sheets was US$1,855/ton, unchanged from last Friday; the price for privately produced hot-rolled sheets was US$1,835/ton, up US$7/ton from last week. The People's Bank of China released a positive statement, but Trump's response to tariff policies remained in normal status, creating a mixed macro sentiment. The non-ferrous metal sector saw a counter-trend increase, and stainless steel prices rebounded from the bottom. Market end-user sentiment improved.

200 Series: Prices Show Mixed Movements.

This week, prices for the 201 series remained weak and stable. The price for 201J2 cold-rolled sheets was US$1,055/ton, while 201J1 cold-rolled sheets were priced at US$1,165/ton, and hot-rolled sheets at US$1,160/ton. At the beginning of the week, 201J1 cold-rolled prices were reduced by US$1,165/ton, while prices for 201J2 cold-rolled and 201J1 hot-rolled remained unchanged. As the week progressed and futures prices strengthened, market sentiment was boosted, leading some traders to increase the price of 201J2 cold-rolled sheets by US$3~5/ton. Overall, inquiries were active, and transaction volumes improved, with a reduction in inventory for the second consecutive month.

400 Series: Inventory Continues to Accumulate, Prices Under Pressure.

This week, the 430 series showed weak prices. As of Friday, the cold-rolled price for 430 in Wuxi was US$1,125-1,130/ton, and the state-owned hot-rolled price was around US$1,055/ton, both unchanged from last week.

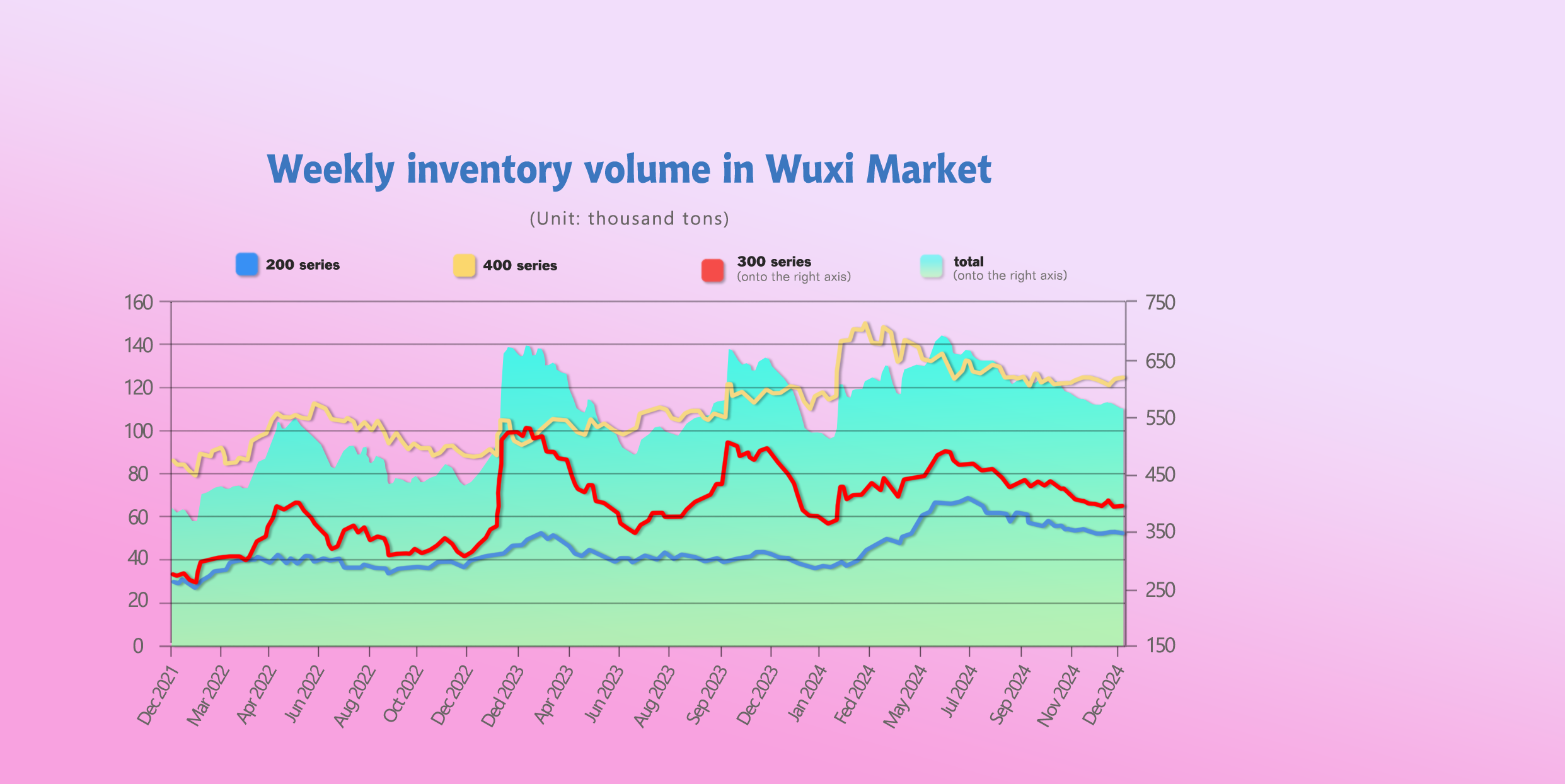

INVENTORY || Chinese New Year Approaches, Steel Mills Begin to Shut Down.

January 9 – According to statistics, the total inventory in Wuxi sample warehouses decreased by 0.16 million tons to 563,000 tons. Specifically:

•The 200 series saw a reduction of 0.13 million tons to 51,000 tons.

•The 300 series saw a reduction of 0.09 million tons to 387,800 tons.

•The 400 series saw an accumulation of 0.06 million tons to 124,200 tons.

| Inventory in Wuxi sample warehouse (Unit: tons) | 200 series | 300 series | 400 series | Total |

| Jan 3rd | 52,339 | 388,655 | 123,635 | 564,629 |

| Jan 9th | 51,000 | 387,800 | 124,200 | 563,000 |

| Difference | -1,339 | -855 | 565 | -1,629 |

200 Series: Steel Mill Maintenance Helps Accelerate Inventory Reduction.

For the 200 series, inventory reduced by 0.13 million tons to 51,000 tons (with cold-rolled reducing by 0.10 million tons and hot-rolled reducing by 0.03 million tons). From the inventory structure, several steel mills like Baosteel and Delong have begun to reduce production and maintenance, which reduced the arrival of cold-rolled resources. The strong futures market has boosted market sentiment, with the consumption side replenishing stock at lower prices. Short-term prices for 201J2 may remain stable.

300 Series: Increased Arrivals Slow Inventory Reduction.

This week, the 300 series inventory in Wuxi decreased by 0.09 million tons (cold-rolled down 0.19 million tons, hot-rolled up 0.11 million tons) to 387,800 tons. Futures prices rebounded from the bottom, and prices in the spot market remained low. Market sentiment improved, and downstream demand for inventory replenishment increased. With the approach of the Chinese New Year, downstream traders have become more cautious in purchasing, leading to short-term demand stagnation. Steel mills are gradually starting maintenance, which may ease supply pressure, and prices are rebounding.

400 Series: Downstream Just-in-Time Purchases, Inventory Slightly Increased.

This week, the 400 series in Wuxi saw a slight increase in inventory by 0.06 million tons to 124,200 tons, with cold-rolled increasing by 0.09 million tons and hot-rolled slightly decreasing by 0.03 million tons. The price of 430 cold-rolled sheets remained steady, and trade primarily relied on just-in-time purchases, which slowed down the consumption of stock. The futures market continued to strengthen, boosting market confidence, but hot-rolled prices slightly corrected, with the downstream replenishing at lower prices.

SUMMARY || Stainless Steel Prices Hit Bottom, Market Waits for Solid Rebound.

300 Series: Futures prices rebounded, boosting market sentiment. End-users increased stockpiling before the holiday, helping to reduce inventory. In December, production of 300 series stainless steel by steel mills hit a record high, and market arrivals may increase. As the New Year approaches, downstream businesses are starting to close, which will reduce demand. In the short term, 304 cold-rolled prices are expected to follow fluctuating trends.

200 Series: Steel mills' reduced production and inventory depletion have eased supply pressure. As the Chinese New Year approaches, some traders are optimistic about stockpiling demand. The consumption side is choosing to replenish at lower prices, increasing transaction volume. Short-term 201J2 prices may remain stable.

400 Series: With the drop in ferrochrome prices, the cost of 400 series stainless steel has decreased, and the market remains relatively stable. Due to inventory accumulation in the previous two weeks, the inventory for the 400 series has increased. However, as steel mills begin to reduce production, the supply pressure may ease, with prices expected to remain weak.

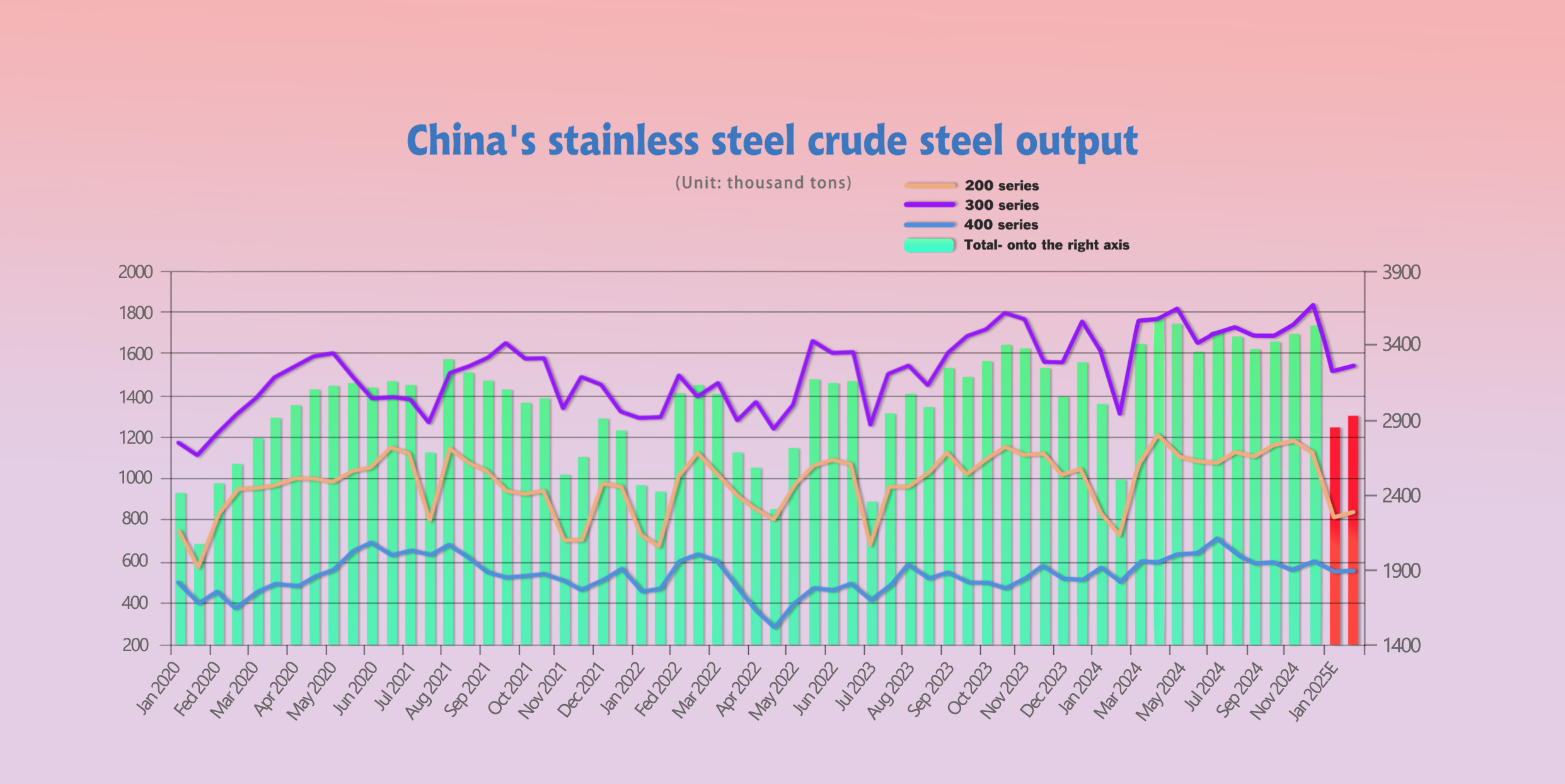

OUTPUT || 40.14 Million Tons, 2024 Stainless Steel Production Hits Record High.

Since December, steel mills have reduced prices to increase orders, with market traders lowering prices to clear inventory. With better export demand, market transactions have been active, and steel mills' production has remained high. According to statistics, in December, domestic stainless steel production reached 3.53 million tons. In 2024, stainless steel production at large-scale domestic enterprises surpassed 40 million tons, reaching 40.14 million tons.

In December, production figures for each series were as follows:

•200 Series: 1.1166 million tons, a decrease of 52,500 tons from the previous month (-4.49%), but an increase of 72,900 tons from the same month last year (+6.98%). In 2024, the 200 series production increased by 480,000 tons to 12.74 million tons (+4%).

•300 Series: 1.8175 million tons, an increase of 87,400 tons from the previous month (+5.05%), and an increase of 67,600 tons from last year (+3.86%). In 2024, the 300 series production increased by 1.07 million tons to 20.20 million tons (+6%).

•400 Series: 592,900 tons, an increase of 33,000 tons from the previous month (+5.89%), and an increase of 90,900 tons from last year (+18.11%). In 2024, the 400 series production increased by 1.11 million tons to 7.19 million tons (+18%).

300 Series: December saw wide fluctuations in spot prices, with nickel prices continuing to fall, and ferrochrome prices plunging. Steel mills' costs have been reduced, alleviating losses. Several mills maintained stable 300 series production, while production from Delong and Tsingshan Fujian increased, setting a record for 300 series output.

200 Series: December’s end-user demand for 200 series was lackluster. Inventory depletion was slow, and price reductions were triggered by both costs and market prices. Steel mills remained in a loss state. The output for 200 series declined to 1.12 million tons.

400 Series: With the drop in ferrochrome prices, the cost for the 400 series weakened. However, prices remained stable, and profits for 400 series steel mills slightly recovered. Production showed a minor rebound.

As we enter January, with the Chinese New Year approaching, downstream demand is expected to decrease. Many steel mills have started maintenance and reduced production. According to a survey, 12 steel mills plan to reduce production in January and February, which may affect production by around 830,000 tons.

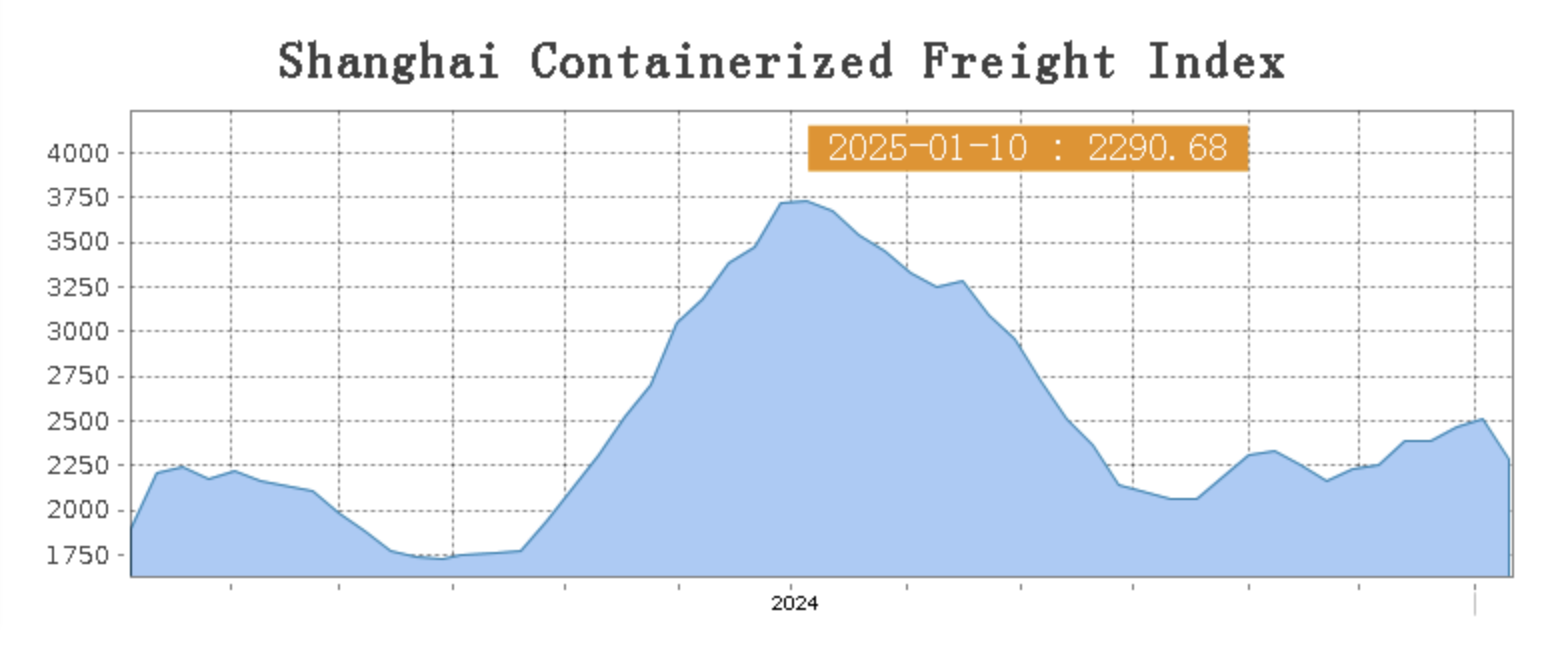

SEA FREIGHT || Long-distance route freight rates declining.

This week, the Chinese export container shipping market adjusted, with ocean freight rates on long-distance routes falling, pulling down the composite index. On January 10, the Shanghai Shipping Exchange's Shanghai Export Container Composite Freight Index stood at 2,290.68 points, down 8.6% from the previous period.

Europe/ Mediterranean:

Due to Ukraine's decision to stop providing natural gas transit services, energy prices have risen, which will increase inflationary pressures in Europe. Additionally, the future international trade relations face significant uncertainty, and the European economic outlook is facing many risks. This week, transportation demand lacks further growth momentum, and the supply-demand fundamentals have weakened, leading to a decline in spot market booking prices. On January 10, the market rate for exports from Shanghai Port to major European ports (including sea freight and sea freight surcharges) was $2,440/TEU, down 14.4% from the previous period. Mediterranean routes are following the same trend as European routes, with market prices continuing to fall. On January 10, the market rate for exports from Shanghai Port to Mediterranean ports (including sea freight and surcharges) was $3,477/TEU, down 7.2% from the previous period.

North America:

Currently, the East Coast ports in the U.S. have reached an agreement, and the strike risk has been mitigated, leading to a stabilization of market sentiment. This week, the transportation market lacks fundamental support, and after a continuous rise in prices, the market rates have started to adjust. On January 10, the market rates for exports from Shanghai Port to major U.S. West Coast and East Coast ports (including sea freight and surcharges) were $4,682/FEU and $6,229/FEU, respectively, down 6.3% and 2.9% from the previous period.

The Persian Gulf and the Red Sea:

Transportation demand growth has slowed, and the transportation market is weakening. This week, spot market booking prices have declined. On January 10, the market rate for exports from Shanghai Port to major Persian Gulf ports (including sea freight and surcharges) was $1,397/TEU, down 5.1% from the previous period.

Australia/ New Zealand:

The local demand for various materials remains generally stable, and market prices have fallen from their high levels. On January 10, the market rate for exports from Shanghai Port to major Australasian ports (including sea freight and surcharges) was $1,838/TEU, down 14.4% from the previous period.

South America:

Transportation demand growth is weak, and the supply-demand balance is not ideal. This week, market prices continue to decline. On January 10, the market rate for exports from Shanghai Port to major South American ports (including sea freight and surcharges) was $4,637/TEU, down 13.2% from the previous period.