Stainless Insights in China from March 17th to March 23rd.

WEEKLY AVERAGE PRICES

| Grade | Origin | Market | Average Price (US$/MT) | Price Difference (US$/MT) | Percentage (%) |

| 304/2B | ZPSS | Wuxi | 2,105 | 28 | 1.42% |

| Foshan | 2,145 | 28 | 1.39% | ||

| Hongwang | Wuxi | 2,005 | 17 | 0.89% | |

| Foshan | 2,020 | 15 | 0.81% | ||

| 304/NO.1 | ESS | Wuxi | 1,935 | 13 | 0.69% |

| Foshan | 1,950 | 21 | 1.15% | ||

| 316L/2B | TISCO | Wuxi | 3,500 | 0 | 0.00% |

| Foshan | 3,570 | -6 | -0.16% | ||

| 316L/NO.1 | ESS | Wuxi | 3,375 | 0 | 0.00% |

| Foshan | 3,360 | 0 | 0.00% | ||

| 201J1/2B | Hongwang | Wuxi | 1,265 | 15 | 1.35% |

| Foshan | 1,275 | 21 | 1.83% | ||

| J5/2B | Hongwang | Wuxi | 1,165 | 15 | 1.48% |

| Foshan | 1,175 | 21 | 2.00% | ||

| 430/2B | TISCO | Wuxi | 1,155 | 6 | 0.54% |

| Foshan | 1,145 | 6 | 0.54% |

TREND || Nickel Price Decline Drags Down Stainless Steel Prices

Stainless steel futures experienced a weak trend last week, with active market trading. The sharp decline in nickel prices led to a pullback in stainless steel futures on Tuesday, accompanied by increased trading volume and a significant drop in open interest, marking the end of the recent upward trend. Although the accumulation of warehouse receipts slowed, the overall volume remained at a high level, exerting pressure on the market. The main stainless steel futures contract closed at US$1980/MT, down 1.95% for the week, with a weekly high of US$1975/MT.

300 Series: Strong Price Support from Mills, Lower-Priced Resources Depleted

The spot market for 304 stainless steel saw a slight price drop last week. As of last Friday, the mainstream base price for private cold-rolled four-foot 304 stainless steel in the Wuxi region was reported at US$1950/MT, down US$14/MT from last week. The private hot-rolled price stood at US$1930/MT, down US$7/MT week-on-week.

At the beginning of last week, Tsingshan’s opening price surge and Delong's price cap policy boosted market sentiment, leading to consecutive price hikes and increased downstream inquiries and purchases. However, in the latter half of the week, as futures prices plunged, downstream buyers adopted a cautious and wait-and-see approach, primarily purchasing lower-priced resources based on immediate needs. Rising raw material prices provided cost support for stainless steel, and despite cost pressures, steel mills continued to hold firm on pricing. Downstream buyers took advantage of dips, resulting in decent transaction volumes throughout the week.

200 Series: Persistent Shortage, Inventory Slightly Decreases

Prices for 201 stainless steel continued to rise last week. The reported base price for 201J2 cold-rolled stainless steel reached US$1145/MT, while 201J1 cold-rolled was at US$1240/MT, and 201J1 hot-rolled was at US$1205/MT.

On Monday, the prices of 201J1 and 201J2 cold-rolled stainless steel increased by US$7/MT, followed by a US$7/MT increase across 201J1 cold-rolled, 201J2 cold-rolled, and 201J1 hot-rolled on Friday. The continuous price hikes, combined with a persistent shortage of thin-gauge Hongwang 201J2 cold-rolled resources, created a bullish sentiment in the market. Later in the week, Tsingshan shipments, further strengthening market optimism, making lower-priced resources harder to find. Both cold-rolled and hot-rolled inventories saw a slight reduction.

400 Series: Agents Slightly Increase Prices, Inventory Declines Significantly

Last week, prices for 430 cold-rolled stainless steel in the Wuxi market edged up to US$1165/MT, an increase of US$7/MT from last weekend. The mainstream price for 430/NO.1 remained at US$1075/MT, unchanged from the previous week. Meanwhile, the guidance prices for 430/2B stainless steel from TISCO and JISCO remained steady at US$1485/MT.

A notable reduction in 400 series stainless steel spot inventories was observed in Wuxi last week, bringing total stock down to around 139,500 tons, with cold-rolled inventory decreasing by 4,000 tons and hot-rolled inventory by 1,500 tons. Reduced sales pressure provided stronger price support.

INVENTORY || Maintenance and Production Cuts at Three Major Mills Impact March 200-Series Stainless Steel Supply

March 20 – According to market sources, Beigang New Materials has shut down one of its blast furnaces for maintenance, a rotational repair process expected to last three months, reducing 200 series production by approximately 300,000 tons. Additionally, Tsingshan has decreased 200 series production this month while increasing 300 series output, affecting 200 series supply by around 30,000 tons. Moreover, due to steelmaking equipment failures, Baosteel Desheng's 200 series production for March is expected to drop by 20,000 tons, with notable shortages of cold-rolled and hot-rolled materials.

RAW MATERIAL || Short-Term Strength in Ore Prices

Last week, high-nickel pig iron (NPI) prices continued their upward trend. Early in the week, an Indonesian plant's NPI transactions were recorded at US$144.8/nickel point. The prolonged rainy season in Sulawesi, Indonesia, disrupted mining and transportation, further tightening nickel ore supply, especially with the end-of-month Eid al-Fitr holiday approaching. Additionally, rising shipping costs from the Philippines to China pushed nickel ore prices at domestic ports up by $2–$3 per wet ton, with 1.5% grade nickel ore CIF prices reaching $59–$61 per wet ton. In the short term, NPI prices are expected to remain strong.

Meanwhile, high-carbon ferrochrome prices also strengthened, with domestic prices reaching around US$1093/MT. Increased inquiries in the chrome ore market reflected strong expectations for price increases. On Friday, a major South African chrome ore supplier raised its offer by $5/ton, while futures prices from other key suppliers increased by $5–$15/ton throughout the week. The cost support for ferrochrome remains strong, with high smelting costs limiting ferrochrome supply. From January to February, China’s total High-carbon ferrochrome imports stood at 550,800 tons, down 50,200 tons year-on-year, as both production and imports declined. On the demand side, rising stainless steel production is driving up ferrochrome demand, with some mills securing orders at high prices. High-carbon ferrochrome prices are expected to remain firm in the short term.

LME Fined $11.9 Million Over 2022 Nickel Crisis

March 21, 2025 – The UK Financial Conduct Authority (FCA) has fined the London Metal Exchange (LME) £9.2 million ($11.9 million) over its failure to effectively manage extreme nickel price volatility in 2022. This marks the first enforcement action against a UK-based exchange, stemming from LME's lack of control during the March 2022 nickel price surge.

The FCA's investigation revealed multiple failures at LME, the world's oldest and largest industrial metals exchange, in handling extreme market stress. On March 8, 2022, nickel prices doubled in just a few hours, surpassing $100,000 per ton. However, during the peak of the price surge, only junior staff were on duty, delaying crucial communication to senior management.

“This meant that when nickel contract prices experienced extreme volatility in the early hours of March 8, the issue was not promptly escalated to LME leadership,” the FCA stated. The LME was forced to cancel $12 billion worth of trades, leading to lawsuits from multiple financial institutions. Although the LME ultimately won these legal battles, court proceedings exposed critical risk management weaknesses.

Simon Morris, a financial services partner at CMS law firm, commented, "Policies for handling market stress were unclear, front-line staff weren't trained to know what to do or who to tell, and when senior management were briefed they were uncertain how to respond."

Steve Smart, joint executive director of FCA's Enforcement and Market Oversight, added, “LME should have been far better prepared for the risks associated with extreme volatility.”

SUMMARY || Futures Surge and Retrace, Spot Prices Follow Downward Trend

Last week, stainless steel spot prices weakened, as raw material prices remained firm, steel mills faced weak production margins, and market demand remained limited to essential purchases. Buyers were reluctant to accept high prices, adopting a wait-and-see approach. Meanwhile, market supply remained abundant, with social inventories staying high and warehouse receipts continuing to rise. Going forward, attention will be on inventory reduction speed, mill production plans, and raw material prices, with expectations for continued price volatility.

300 Series: Steel production is gradually recovering, increasing market circulation of available resources. Demand remains driven by essential needs, while speculative buying fluctuates with market sentiment. Inventory levels have started declining but remain high, with slow liquidation rates. Nickel pig iron (NPI) prices continue to rise due to supply constraints, supporting costs. Meanwhile, expanding overseas tariff policies and the resumption of trade tensions are pressuring the commodity market. Domestic macroeconomic expectations remain strong, with increased market speculation. In the short term, 304 cold-rolled and hot-rolled stainless steel prices are expected to follow futures market fluctuations.

200 Series: Beigang, Baosteel, and other mills have reduced production due to maintenance, while Qingshan has partially shifted from 200-series to 300-series production, tightening 200-series supply for March. Copper prices increased slightly last week, providing strong cost support. In the short term, 201 stainless steel is expected to remain stable and firm.

400 Series: High-carbon ferrochrome prices rose by US$28/50 reference ton, strengthening cost support for 400-series stainless steel. Market sentiment improved, while mills maintained limited deliveries, leading to a noticeable inventory reduction. With lower supply pressure, 430 stainless steel prices remained stable with a slight upward trend. Next week, restocking demand for 400-series stainless steel is expected to increase, with prices remaining steady overall.

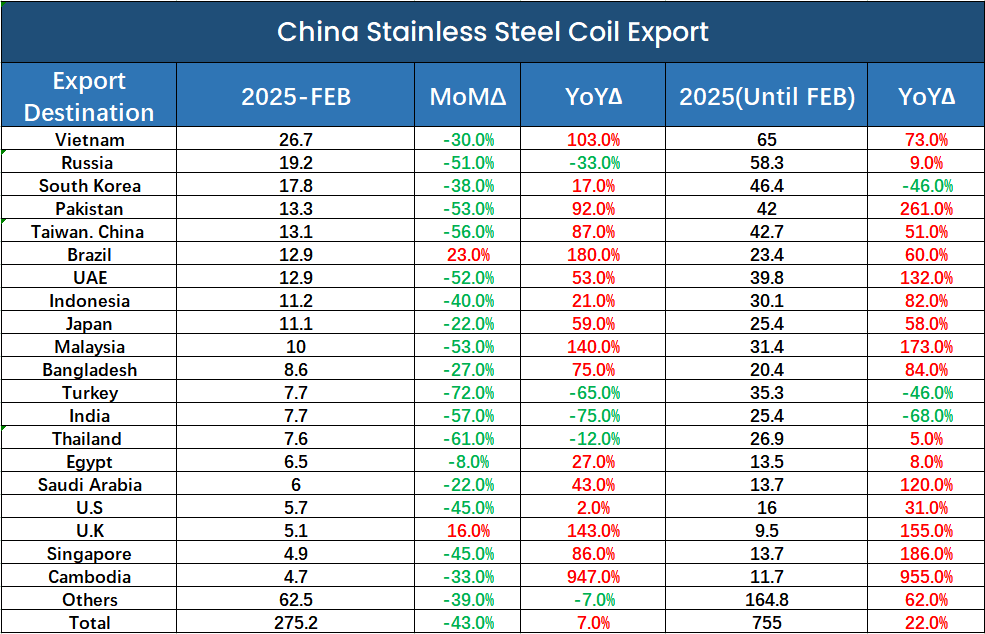

MACRO || China's Stainless Steel Exports Fell 43% in February

According to customs data, China's stainless steel exports totaled 275,200 tons in February, down 43% month-on-month, mainly due to the Chinese New Year holiday. Vietnam was China's largest stainless steel export destination in February, with January-February exports reaching 65,000 tons, marking a 73% year-on-year increase. Meanwhile, exports to Brazil and the UK showed month-on-month growth.

From January to February 2025, China's total stainless steel imports stood at 321,900 tons, down 29.31% year-on-year. Over the same period, exports totaled 755,300 tons, up 11.83%. The net export volume reached 433,400 tons, marking a 97% year-on-year increase.

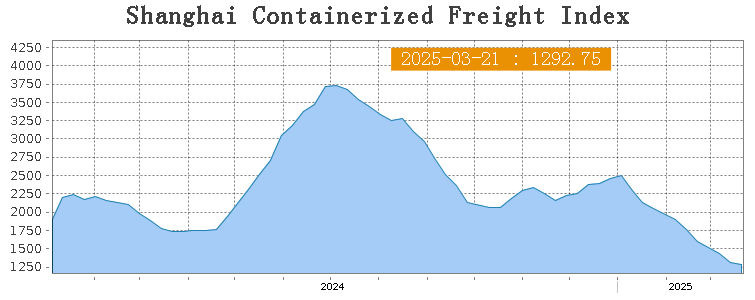

SEA FREIGHT || Market Continues to Adjust as Freight Rates Decline on Most Routes

Last week, China's export container shipping market continued its downward adjustment, with weaker transportation demand and declining freight rates across most routes, leading to a drop in the composite index. On March 21st, the Shanghai Containerized Freight Index (SCFI) fell 2% to 1292.75 points.

Europe/ Mediterranean:

On March 21st, the freight rate (maritime and marine surcharge) exported from Shanghai Port to the European major ports was USUS$1306/TEU, which slid by 2.7%. The freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the Mediterranean major ports market was USUS$2195/TEU, which dropped by 4.4%

North America:

Early next month, the U.S. is set to implement further “reciprocal tariffs”, which could have a significant impact on global trade. As a result, the North American shipping market is expected to face considerable pressure. This week, demand remained weak, supply-demand balance remained unfavorable, and market freight rates continued to decline.

On March 21st, the freight rates (shipping and shipping surcharges) for exports from Shanghai Port to the US West and US East major ports were USUS$1872/FEU and USUS$2866/FEU, reporting 4.7% and 3.7% decrease accordingly.

The Persian Gulf and the Red Sea:

On March 21st, the freight rate (maritime and marine surcharges) exported from Shanghai Port to the major ports of the Persian Gulf rose 8.5% to US$1059/TEU.

Australia&New Zealand:

On March 21st, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to the major ports of Australia and New Zealand rose 2.7% to US$755/TEU.

South America:

On March 21st, the freight rate (shipping and shipping surcharges) for exports from Shanghai Port to South American major ports dropped 13.6% to US$1680/TEU.